U.S. Overtakes Brazil as Top Crop Protection Market, but Not for Long

17 August 2016

17 August 2016 In nominal terms, the global market for crop protection chemicals declined to $54.6 billion in harvest year 2015 as measured at the ex-company level and using average year exchange rates throughout. Compared to record-high sales of $60.5 billion in 2014, this represents a decline of about 9.8%. It is also the first year the market has declined this decade and brings to an end a five-year period of growth.

Despite the global decline, developed economies tended to perform well as emerging economies struggle to rekindle the strong growth they experienced during the last 10 years. The United States, buoyed by a strong dollar, rising employment, and consumer confidence, once again overtook Brazil as the world’s No. 1 market in terms of sales.

Since 2011, Brazil had outstripped sales of the U.S. market by on average about $1 billion per year. This trend was reversed in 2015 when the U.S. once again gained top spot with sales approaching $8 billion when measured at ex-company level, with Brazil lagging behind by about $100 million.

While not an earth-shattering difference, it does highlight the different fortunes of the world’s two largest markets in 2015. Of course the “devil is in the details” (currency movement being the biggest devil here) and there are several ways to paint quite a different story. One such way is to look at the two markets in terms of area treated. If we add up the cumulative acres of product (Super Developed Area) used on the ground, Brazil is running within a whisper of 1 billion hectares as compared to not much over half-billion hectares SDA for the U.S.

The message is clear — the U.S. will not hold the position as the worlds’ No. 1 market for too long.

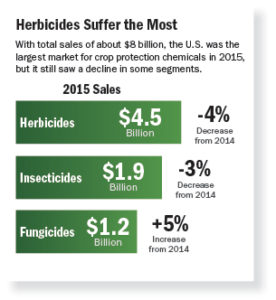

Putting a little more meat on the bones of the U.S. market, like just about everywhere else had a tough time in 2015 compared to 2014. Overall, the market fell in excess of $250 million to reach the $8 billion mark.

Herbicides

Herbicides suffered the greatest fall of 4% such that the sector stood at $4.5 billion or a little over 56% of the total market. Within the herbicide sector, maize saw the biggest fall in terms of sales whereas soybeans saw some improvement.

This divergence is in part due to crop area change, but increasingly to the greater product sophistication of the soybean co-formulations or pre-mixes compared to those for the maize crop.

While maize is the bigger crop in terms of herbicide sales, the gap is getting smaller. Glyphosate-based products still dominate, but the soybean “residual” pre-mixes based on sulfentrazone, chloransulam, and chlorimuron, to name but a few, are gaining a larger part of the cake.

Of course the big story in the herbicide market is the introduction of both the Enlist (2,4-D tolerant) and Xtend (dicamba tolerant) crops and the knock-on effect this might have on the fledging resurgence of the selective corn and soy herbicide markets.

Insecticides

Insecticides also saw a decline dropping 3% to $1.9 billion. Here the decline was felt across all crop groups but most acutely felt in the cotton sector. This in itself is due to declining cotton areas as well as the percentage of acreage that receives any insecticide foliar or soil treatment, now down to less than half the crop area planted. Although the newer active ingredients are gaining market share (again, for example, those based on either sulfoxaflor, flubendiamide, spiromesifen or indeed flupyradifurone) the market is still very dominated by older generic organophosphate and pyrethroid chemistries such as dicrotophos and bifenthrin as well as the now older neonicotinoids, namely imidacloprid and thiamethoxam.

Fungicides

Fungicides were the one shining star in the U.S. market in 2015. Overall the sector grew by just over 5% in value terms such that the market achieved sales of $1.2 billion in 2015.

The key crop groups behind the increase were cereals and soybeans. In both of these crop sectors it is, however, more of the same rather than any product or chemistry upgrade that is driving the market. The co-formulations and pre-mixes have yet to take off in a big way with the market dominated by single active ingredient-based products mainly based on triazoles or strobilurin chemistry. There is room for continual improvement, however, as the newer SDHI chemistry (in this case fluxapyroxad) gain momentum within the market. •

Kleffmann’s amis®AgriGlobe database of farmer surveys and product use information drives much of the company’s “top level” analysis. Now in its third year and hosted on the company’s software platform Kleffmann4you, the database segments product use by geography, crop types, active ingredients and seed varieties.