Moroccan Professionalism Drives Rising Market

19 March 2015

19 March 2015 By Alice Bouchikhi

Kleffmann Group

Morocco is the fifth-largest economy in Africa and has shown positive growth in 2014. Agriculture in Morocco is the main employer for the country’s 33 million people, and it contributes about 15% to the country’s GDP.

About 9 million hectares are arable land, of which only 4.6% (2011) are irrigated. Scarce irrigation makes smallholder farmers vulnerable to drought. In an average year, irrigated land contributes to 45% of agricultural production, 75% of agricultural exports and 35% of farm employment.

Morocco produces many agricultural commodities, especially cereals, grown on 63% of the arable land. Wheat production ranges from 1.5 to 10 million tonnes per year (an average of 7 million tonnes since 2005). Yet production meets only 60% of domestic demand. The cultivated area for wheat increased slightly from 2.6 million hectares in 2007 to 3.2 million hectares in 2013.

Cereal production in Morocco is highly dependent on the appearance of droughts and therefore varies greatly from year to year. The production of other crops remained more or less stable during the past years.

While comparing yields, they are increasing for the majority of crops. For cereals, yields were decreasing until 2010. Since 2012 they are improving but continue to be unstable. Compared with yields of other countries in this region, yields in Morocco are the highest only for tomatoes and watermelon. For almost all other crops, Morocco’s yields are low in the country comparison.

The major limits to agricultural growth in Morocco can be identified as: scarce land and water, precarious land tenure, periodic droughts, soil erosion, poor access to credit, lack of farmer organizations, rural illiteracy and tlow level of technical training.

Morocco’s farms are generally very small. According to the last census (1996), there were 1.5 million farms with an average of 5.8 hectares each. As Figure 1 illustrates, more than 80% of the farms were smaller than 10 hectares, covering around 46% of the area. On the other hand, 12% of farms were equal or bigger than 10 hectares, but covering almost more than 50% of the area.

A market research study conducted by Kleffmann Group with distributors in 2012 revealed a new picture of distribution of farm sizes in Morocco. According to the interviewed distributors, 22% of farms were 10 hectares or more in 2011. More than 40% of the farms are between 5 and 10 hectares and the rest are less than 5 hectares. In general it can be assumed that in comparison to the census results, farm size has increased in Morocco since the mid-1990s.

Crop Protection Trends

Ninety percent of the crop protection market is now private; 95% of products are imported ready to be used. The remaining 5% is formulated based on pre-mixes or concentrates. More than half of products are imported in appropriate containers, and about 35% to 45% of products are repacked into smaller packages adapted to small farmers’ needs.

Product import values have increased more than import volumes (Figure 2) illustrating that Moroccan farmers prefer newer, low-use actives despite higher prices for them compared to older commodity chemicals, such as organophosphates.

Product import values have increased more than import volumes (Figure 2) illustrating that Moroccan farmers prefer newer, low-use actives despite higher prices for them compared to older commodity chemicals, such as organophosphates.

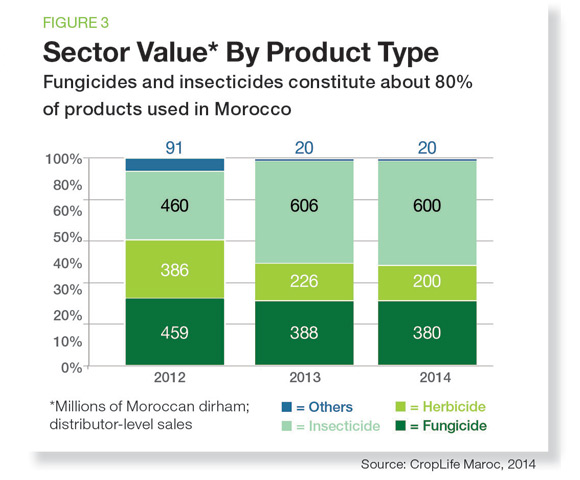

In 2011 Kleffmann Group estimated the total Moroccan crop protection market at $156 million at the farm level. In 2014 CropLife Maroc estimated this market to be around $127 million at the distributor level. Fungicides and insecticides are the dominating crop protection segments followed by herbicides (see Figure 3).

Cereals are the biggest crop by value, accounting for almost one-third of the market. The remaining two-thirds are covered by fruits and vegetables (including grapes, tomatoes and potatoes) and other crops such as olives, maize and nuts. Syngenta was identified as the market leader in Morocco followed by Bayer CropScience and BASF. These top three companies achieved a combined market share of more than 70% in 2011 according to Kleffmann Group’s study results.

The trends in general are positive and indicate growth of agribusiness and more professionalism and efficiency in agricultural production due to increasing farm sizes in Morocco. Government policy and support contribute to this evolution toward more efficient, market-oriented agriculture with better access to improved technology. In 2010, new arrangements targeted two categories of farmers: small farmers with  holdings up to 5 hectares and those with larger holdings. Besides government policies, climatic conditions (such as periodic droughts) are also important factors for Moroccan agriculture’s development.

holdings up to 5 hectares and those with larger holdings. Besides government policies, climatic conditions (such as periodic droughts) are also important factors for Moroccan agriculture’s development.

Distribution Structure

Kleffmann Group results on the distribution channel structure indicate a well-organized, three-level-channel structure with distributors, dealers and retailers. Sixty-one percent of distributors and 4% of crop protection companies sell directly to farmers. Interesting is the fact that the influence of the distributors on every supply chain is strong, and even farmers mainly buy from distributors. The results show that for payment terms, an average of 36% of farmers pay for agrochemicasl after harvesting in Morocco, and almost half of farmers make their payments between 30 to 60 days.

The smuggling and counterfeiting market should also not be ignored in Morocco. According to CropLife Maroc these products are estimated to account for 10% to 15% of the market. The situation is exacerbated by the concentration of 600 to 650 sale points in irrigated and agricultural areas. This leads to the proliferation of traveling merchants and counterfeit products.

How farmers become aware of products and become familiar with brands and make their product choices can be grouped in three main categories, according to the Kleffmann study: (1) Farmers follow recommendations and advice from other farmers or colleagues. Distribution channels (distributors, dealers, retailers) and the industry are also very important influencers; (2) field days/trials and demo plots are relevant sources for farmers to obtain the latest information on crop protection trends; (3) print media, such as brochures, flyers, banners and billboards are the most important information source.

Market Dynamics

Morocco is one of the biggest crop protection markets in the Middle East and Africa region, dominated by Syngenta, Bayer and BASF. Production of vegetables, pome fruits and wheat will increase in Morocco, and it is expected that multinational companies will continue to dominate due to growers’ preference for newer low-use actives.

However, generic products and proprietary post-patent brands are showing strong gains and are expected to increase in the foreseeable future, whereas fakes and non-registered products will decrease significantly due to education and enforcement.

In general, farm sizes are expected to increase whereas the rural population is expected to decrease. The future of agriculture in Morocco will depend especially on climatic conditions (i.e. drought), availability of machinery and equipment and governmental support to introduce new technologies (i.e. irrigation, etc.).

For future success in the market, crop protection companies’ key actions have been identified as training, support and services to farmers and distributors, followed by price policy and payment and credit terms. Product availability and marketing and advertising activities are also important measures.

Alice Bouchikhi is Project Manager Middle East & Africa for the Kleffmann Group, a global research and data consultancy. She can be reached at [email protected].

Kleffmann offers monthly analysis to FCI based on its in-country surveys of farmers. See Kleffmann’s analysis of China next month.