China Price Index: What Renewed China-U.S. Cooperation Means for Global Ag Markets

21 May 2026

21 May 2026 Editor’s note: Contributing writer David Li offers a snapshot of current price trends for key herbicides, fungicides, and insecticides in the Chinese agrochemical market in his China Price Index. Below he also examines how renewed China-U.S. trade cooperation could reshape soybeans, crop protection markets, and global agriculture.

View all

According to Reuters on May 18, China committed to buying at least $17 billion of U.S. agricultural products annually in addition to soybeans for three years, the White House said on Sunday, after a summit of the two countries’ leaders in Beijing last week. And both have agreed to expand agricultural trade and tackle non-tariff barriers for beef and poultry, China’s commerce ministry said on Saturday.

The Chinese government extended the highest level of hospitality during President Trump’s visit. This fully demonstrates the respect and importance that Chinese leaders attach to the top decision-maker of the U.S. In their public statements, both China and the U.S. characterized their bilateral relationship as a ‘constructive and strategically stable relationship.’

Plan for Stability

The Ministry of Foreign Affairs of the People’s Republic of China elaborated on the meaning of this relationship in its official report: “Constructive strategic stability” means positive stability with cooperation as the mainstay, healthy stability with competition within proper limits, constant stability with manageable differences, and lasting stability with expectable peace. Building a constructive China-U.S. relationship of strategic stability is not a slogan. It means actions in the same direction.

Certainty is extremely rare in this chaotic and complex era. Through this summit, China and the U.S. are clearly sending a message to the world that, on the foundation of peace, and within the framework of complementary advantages, manageable competition, and the bottom line of avoiding conflict, bilateral relations remain highly resilient.

Agriculture, which has long been both the easiest and the most fragile link for cooperation between China and the U.S., is likely to see substantial changes for both countries following this summit. The open and cooperative stance both sides demonstrated during the summit, by opening their national doors, has greatly inspired agricultural practitioners in both China and the U.S.

Following the U.S.-Iran conflict, international geopolitical risks have dealt a severe blow to global agricultural supply chains and trade. Tightened global supplies of crude oil and liquefied natural gas have triggered worldwide supply shortages and driven up the costs of agricultural inputs. Inflation risks are mounting across emerging economies worldwide. Rather than excessive currency issuance, greater attention should be paid to supply shortage-driven inflation in these economies.

China’s energy structure is only 6% to 7% vulnerable to a potential closure of the Strait of Hormuz. Its full-industry-chain supply system has become a cornerstone of global economic stability. In particular, steady operation of agricultural input enterprises has to some extent guaranteed the sustainable supply of crop protection products. After all, no one wishes to discover cracks in the foundation of their house amid turbulent times.

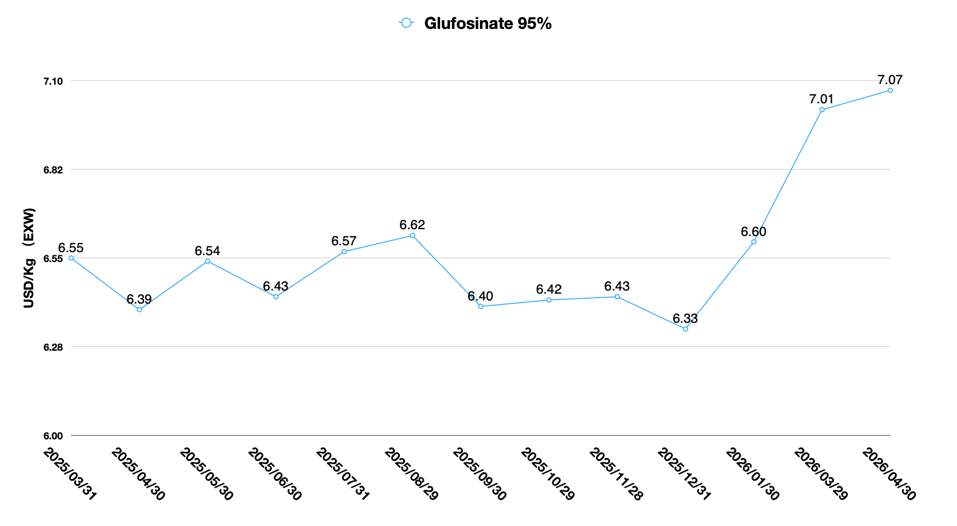

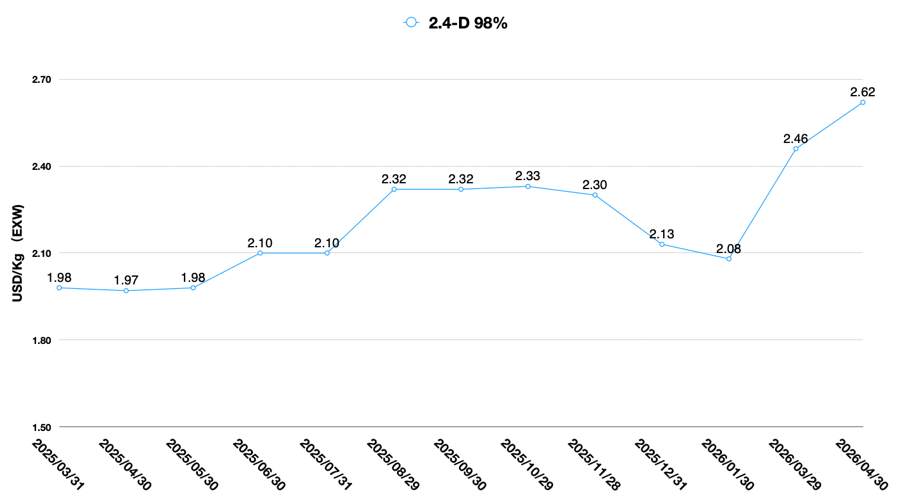

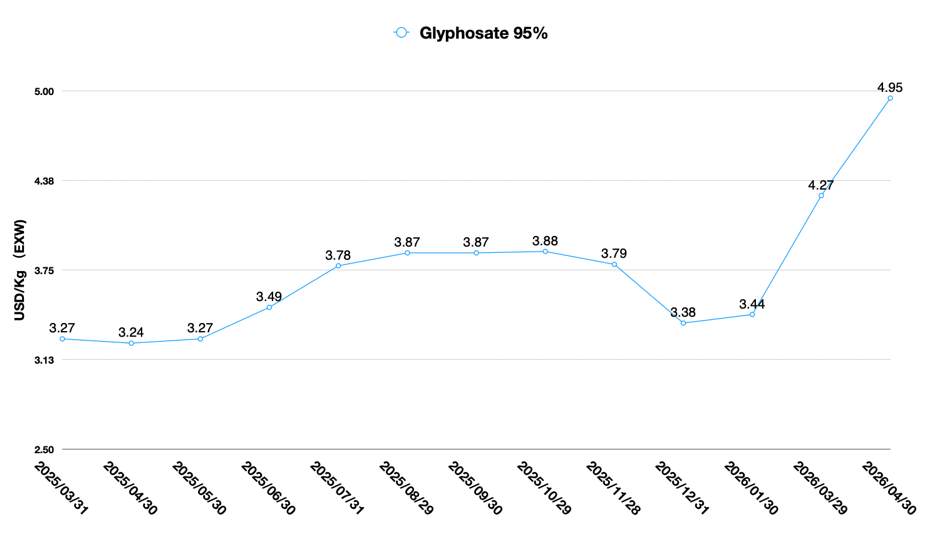

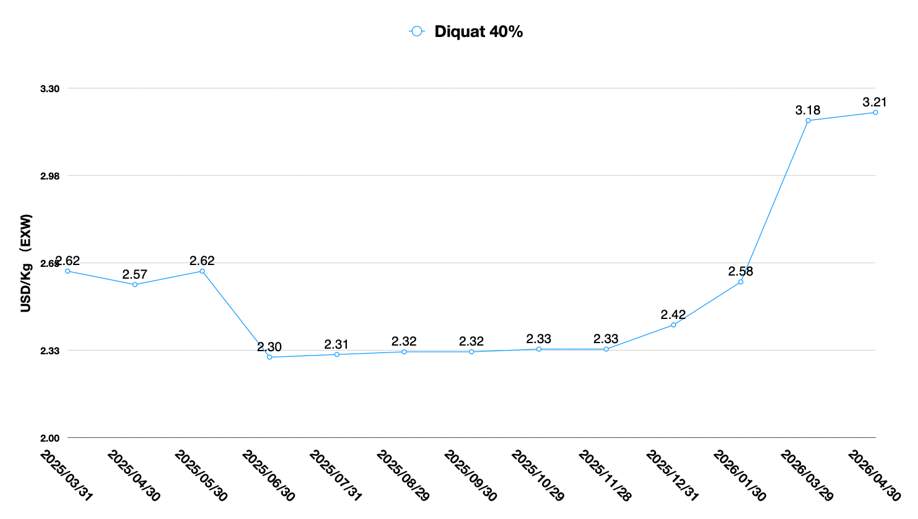

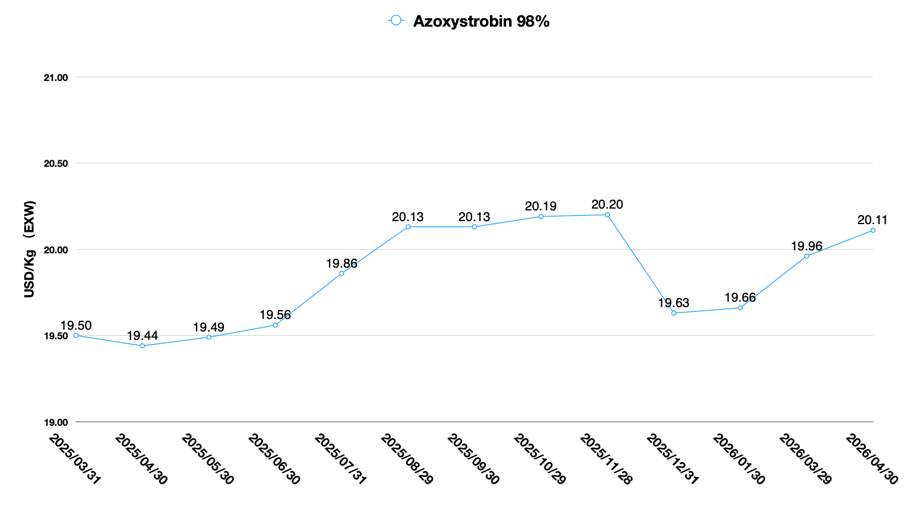

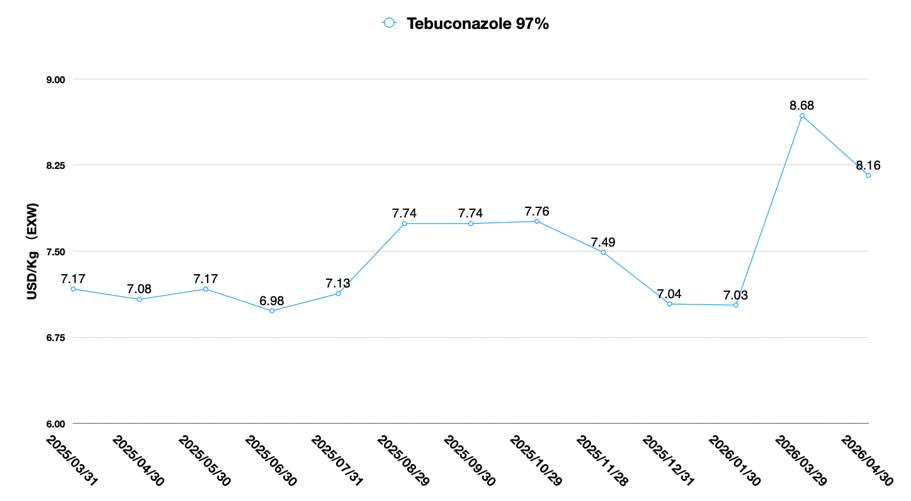

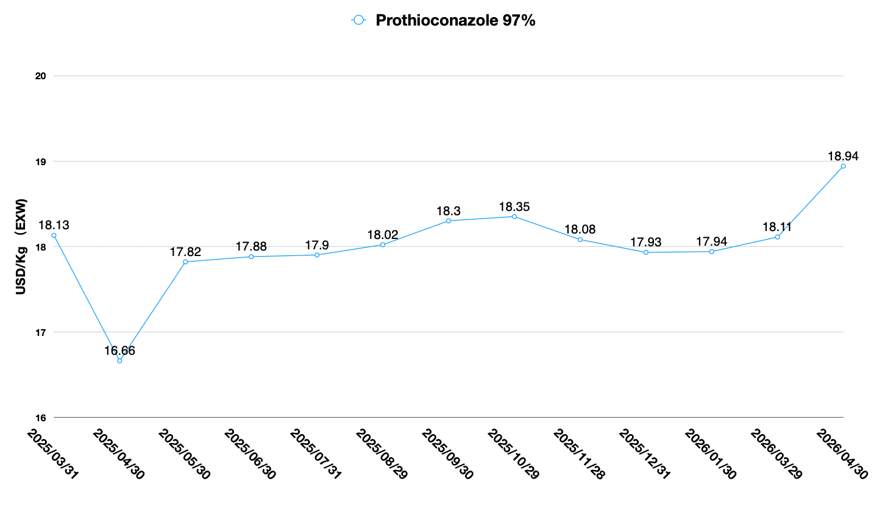

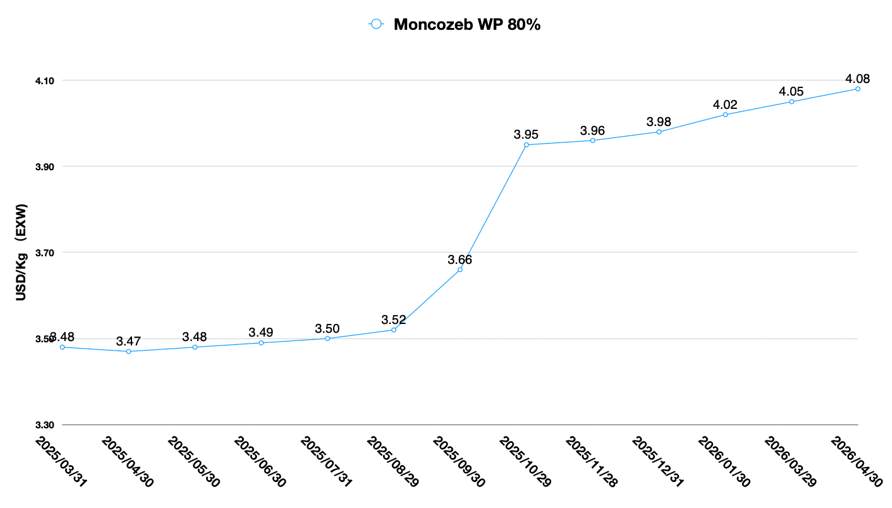

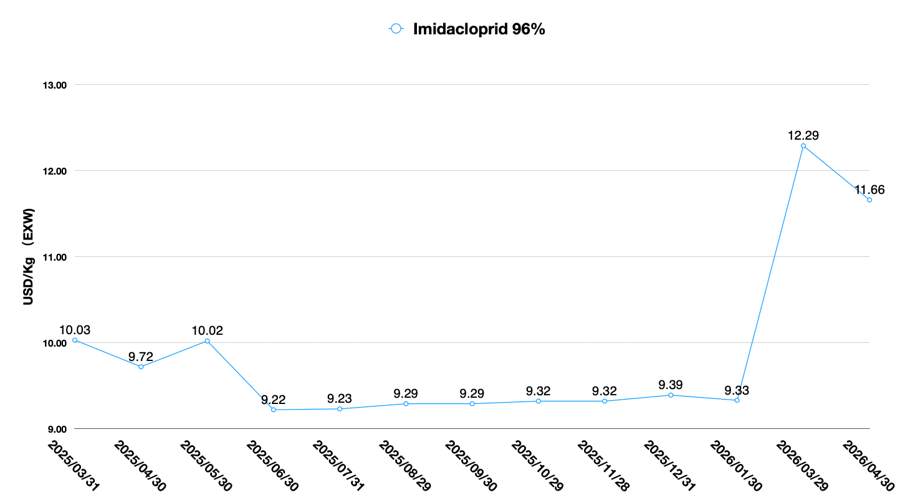

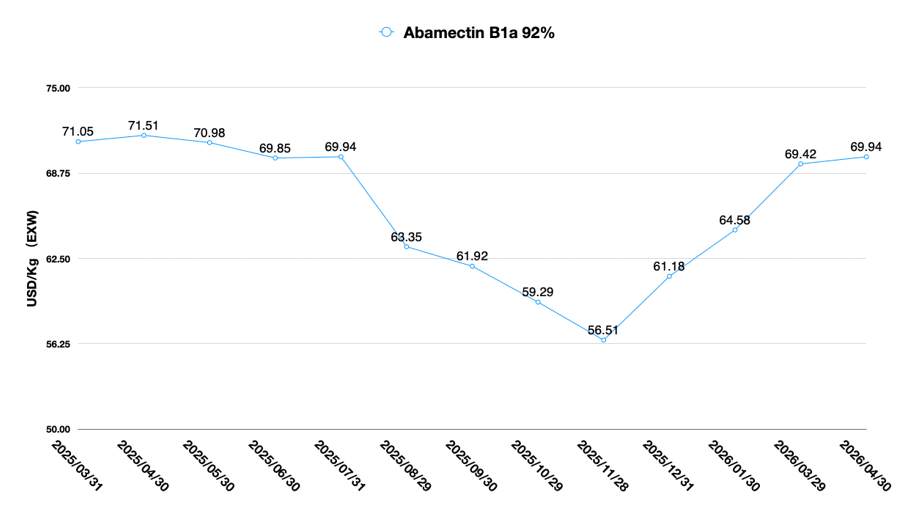

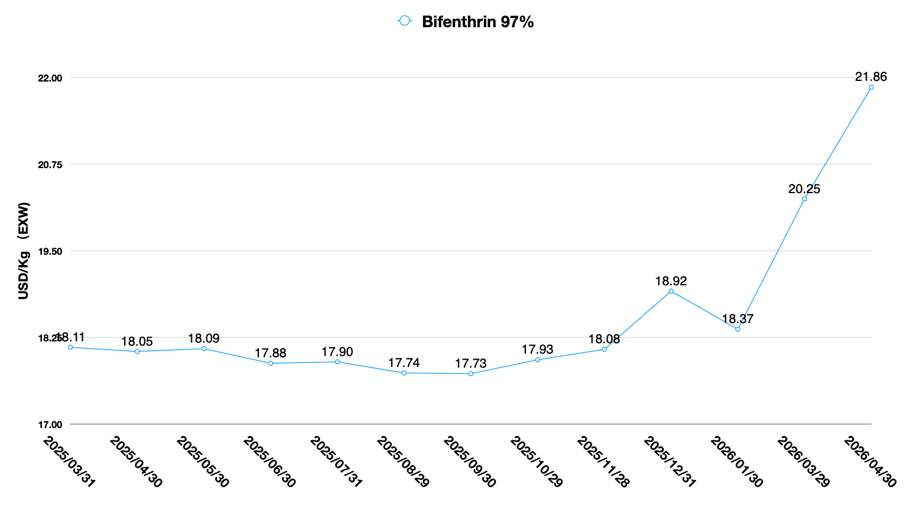

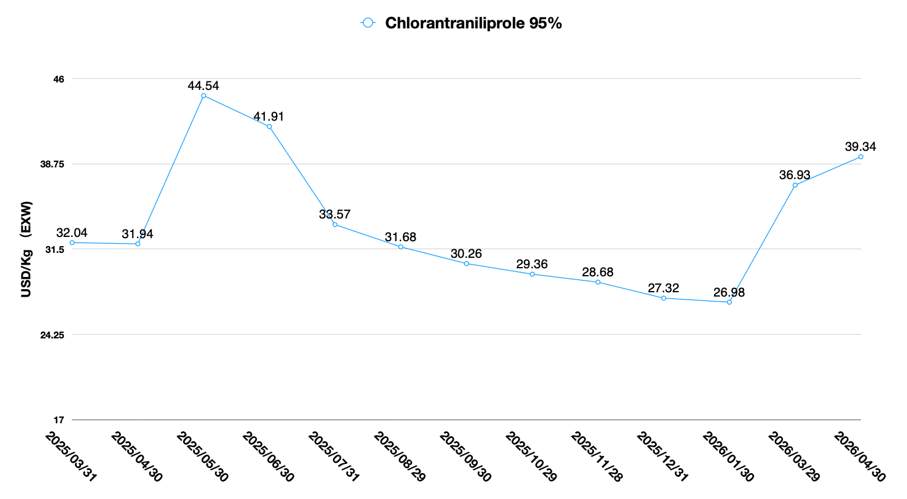

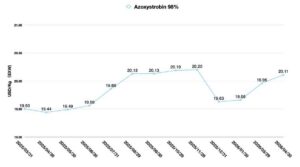

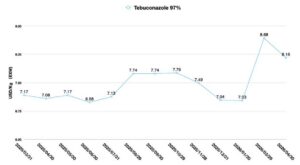

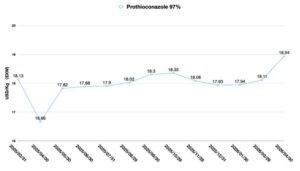

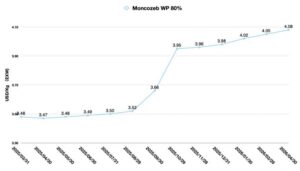

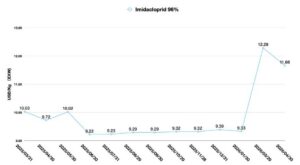

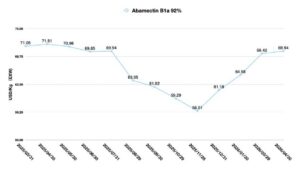

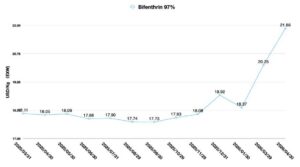

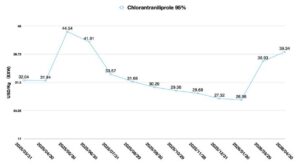

China’s Technical Pesticide Market

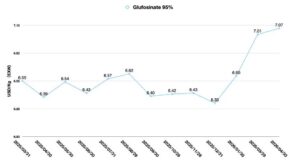

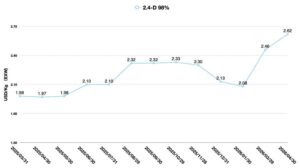

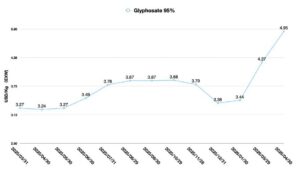

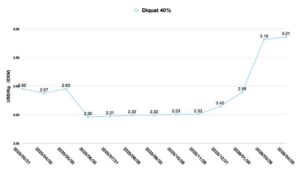

There has indeed been a certain increase in raw material supply costs, especially sulfur and its downstream raw materials. Tight supply of PMIDA and glycine relevant to glyphosate, as well as bromine used for diquat and chlorfenapyr, has significantly pushed up prices of downstream technical pesticides. In the short term, prices in China’s technical pesticide market have surged rapidly.

Meanwhile, quotations of formulated products from China’s suppliers have substantially squeezed profit margins of distributors to a certain extent. Domestic manufacturers adopt a cautious pricing strategy, while traders seize the opportunity to earn spreads by utilizing low-cost inventory stocked earlier. Performance pressures dating back to 2023 have forced enterprises to step up efforts to boost profit margins.

Nevertheless, the scenario of sharp price hikes paired with rising sales volumes seen between 2021 and 2022 is unlikely to recur. Overseas demand serves as a clear market barometer. Farmers in North America hold growing concerns over the prospects of agricultural commodity trade.

Fierce market competition has prompted overseas clients to adopt a more conservative stance amid price increases of products like diquat, such as switching to glufosinate as an alternative. Some distributors have also opted to delay purchases. Restocking demand in North America can be readily satisfied by stable branded products from multinational enterprises. Prior to the arrival of North America’s purchasing season, most distributors remain on the sidelines.

Boosting Sales Volume

To some extent, the market landscape hinges on competitors’ strategies. Major multinational corporations have recently released their Q1 2026 financial results. It is evident that all of them are facing headwinds from price declines across South America. Increased sales volume is virtually the only way to offset such negative impacts.

To boost sales volume, they tend to incentivize channels to stock up on branded products to the fullest extent possible. Regional sales teams are likely to push sales KPIs down the distribution chain to hit targets, which largely depends on the inventory absorption capacity of distributors. It is quite common to relieve sales pressure by taking distributors as a buffer. Hence, actual field consumption is what we truly need to focus on.

Combining three key factors: no large-scale supply shortage on China’s supply side, uncertain purchasing willingness among distributors, and the impact of branded products from multinational corporations — especially generic products in the mature declining stage — on distribution channels, these will pose certain adverse pressures on China’s pesticide supply prices.

Against this backdrop, low-quality formulated products have frequently emerged in overseas markets. To sustain profit margins or minimize losses, suppliers often produce goods with insufficient active ingredient content and poor emulsification stability.

China’s Soybean Imports

Another Reuters report merits widespread vigilance. Dated March 2026, titled “Tighter checks disrupt Brazilian soybean exports to China,” it states that: “Tighter phytosanitary checks are hitting Brazilian soybean shipments to China, threatening to squeeze supplies to the world’s top importer after authorities in the South American country stepped up inspections at Beijing’s request.” Brazil’s Agriculture Ministry increased inspections on soybean shipments to China following Beijing’s repeated findings of pesticide- and fungicide-coated beans, four trade sources said.

The quality of agricultural inputs carries equal weight with agronomic technologies in influencing the quality of farm produce. Following the signing of the agricultural product trade deal between China and the U.S., Brazil will face fierce competition from American soybeans.

If U.S. soybeans are priced competitively this October, China’s import demand in 2026 is highly anticipated, in comparison with its purchase of USD 18 billion worth of U.S. soybeans back in 2022.

The advantage of the North American market lies in its well-established distribution channels, where major distributors wield strong market control. Accordingly, North American distributors face limited quality risks when sourcing Chinese pesticide technicals.

LATAM Channel Fragmentation

As an increasing number of Chinese enterprises launch ToC sales in Latin American markets such as Brazil, the dominance of large distributors is waning, and channel fragmentation has become a new trend. This poses a fresh challenge to formulated product quality control across Latin America.

Furthermore, quality control shall not merely rely on suppliers’ Certificates of Analysis (COA). More importantly, on-site quality supervision and accountability mechanisms within local distribution channels are essential. In some cases, formulated product quality does not require verification by GLP-certified laboratories. Simply using a volumetric flask can easily test whether stratification occurs or crystals precipitate after the formulation is mixed with water.

Nevertheless, Latin American distributors are generally highly price-sensitive. Their price-only procurement logic for pesticides has exposed farmers to rising formulated product quality risks, which in turn leads to prominent issues concerning agricultural product quality and pesticide residues. This has become a core factor undermining the overall quality of China’s upstream supplies. To break this vicious cycle, the fundamental solution is to enable high-quality, reasonably-priced pesticide formulations to gain widespread market recognition.

The Wrap-Up

In summary, the resumption of high-level exchanges between China and the U.S., two major economic powers, is crucial to the stable operation of the global economy, especially the agricultural economy. China has emerged as one of the world’s major purchasers of agricultural commodities. Certainty in major-country relations will stabilize global geopolitics and anchor sound growth logic for global agricultural trade.

Meanwhile, agricultural practitioners should fulfill social responsibilities. Both Chinese enterprises and multinational corporations shall compete under unified quality standards such as CIPAC test methods to drive innovation and vitality in the global agricultural market. High-quality pesticide formulations with superior cost performance are likely to be the optimal development direction in the future.