Crop Protection Market in Central America

Scroll Down to Read

By Derek Oliphant

Co-Founder

AgbioInvestor

This article will outline the key crop protection markets in Central America, examining the current situation as well as the key future trends expected to influence market development in the coming years.

Market values are Agbiolnvestor’s estimates of the value of crop protection products used on the ground in the agricultural year, expressed in U.S.$ terms at the ex-manufacturer level. For southern hemisphere countries, the agricultural year is approximately July to June, for example ‘2023’ refers to the value of products used on the ground between July 2022 and June 2023. For northern hemisphere countries, the agricultural year is approximately October to September, for example ‘2023’ refers to the value of products used on the ground between October 2022 and September 2023.

The most recent full data year available is 2022, with preliminary estimates provided for 2023.

In Central America, crop yields remain lower compared to more developed markets. In addition, aside from Mexico, crop protection product usage is generally on a much less intensive basis than leading crop protection markets in the Americas.

MEXICO |

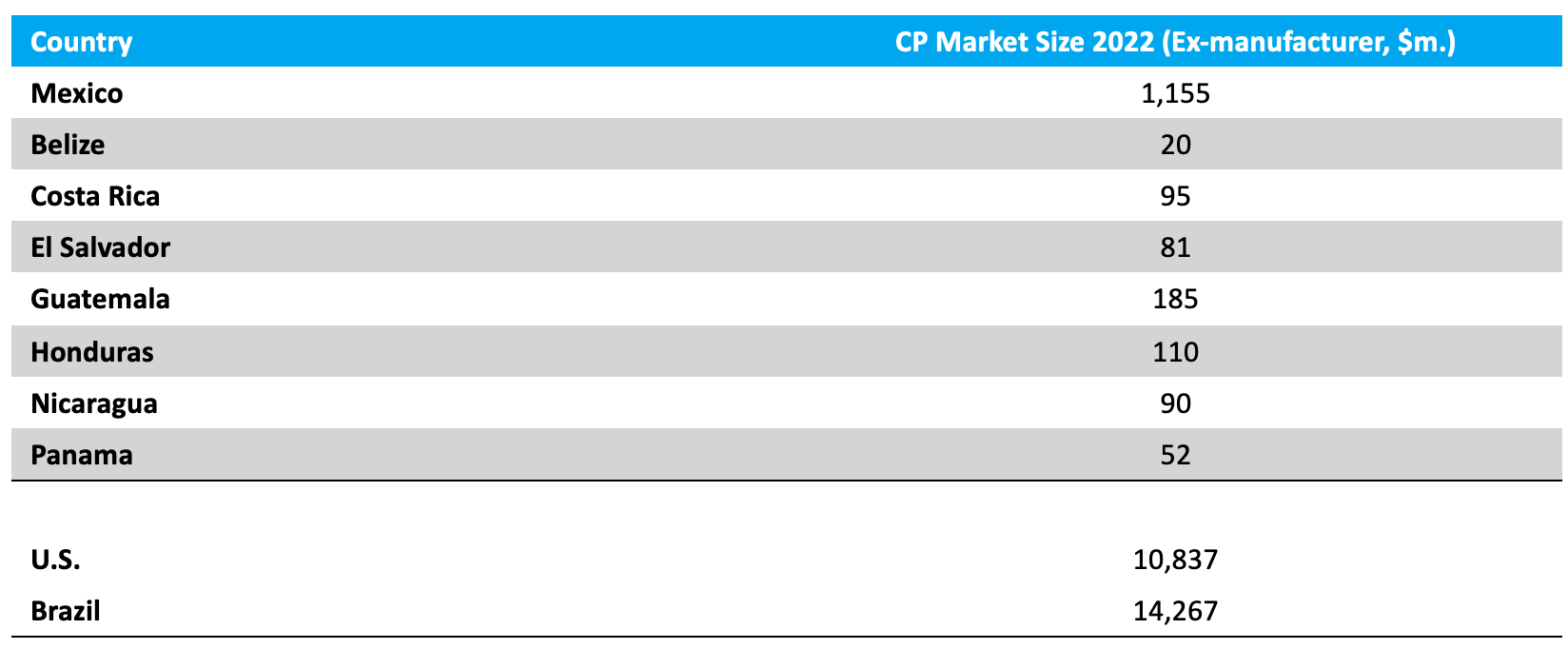

In 2022, the market for crop protection products in Mexico increased by 17.4% to $1,155 million. At this level, the country is ranked as the 13th most valuable in terms of crop protection sales globally in 2022. Between 2017 and 2022, the crop protection market in Mexico has increased steadily at an annual average of 5.9%, marginally ahead of the industry average. Preliminary estimates for the Mexican crop protection market in 2023 suggest an increase of 11.3% in U.S.$ terms to reach $1,285 million, although this reflects decline of 3.0% in local currency terms.

The agriculture sector in Mexico in recent years has advanced at a rate ahead of the country overall, with growth in agricultural GDP outstripping total GDP. Between 2017 and 2022, total GDP has grown from $1.15 trillion in 2017 to $1.41 trillion in 2022 in current U.S. dollar terms. At this level, GDP of agriculture and forestry has increased from $39 billion to $59 billion over the same period. The country has placed a focus in recent years in creating and maintaining a position as a key exporter of agricultural produce, primarily fruit and vegetables (F&V), with this resulting in a shift of focus in terms of crop protection spend away from grain crops and towards the high value F&V sector.

The economy in Mexico is amongst the largest in the Latin America region, behind only Brazil, and more than 90% of overall trade is through free trade agreements.

The economy in Mexico is amongst the largest in the Latin America region, behind only Brazil, and more than 90% of overall trade is through free trade agreements.

These agreements are integral to the country’s agriculture sector, although the drawback of this highly industrialized economy is that agriculture in the country is affected by low-cost imports from its trading partners, who generally place more of a focus on the production of row crops.

Although maize is the most significant crop cultivated in the country in terms of area, it is mainly grown as a subsistence crop for domestic consumption. As a result, the area is not generally subject to fluctuations in maize prices. However, imports from the U.S. are significant, although in many cases, this is utilized for animal feed. Genetically modified (GM) technology has not been introduced, with authorities reluctant to alter the genetic base of domestic maize. Due to the cultural significance of the crop in the country, there is almost no prospect of GM maize varieties being introduced in the near future; as a result, the prospects for maize herbicide sales are relatively buoyant compared to other Latin American countries where GM technology has been readily adopted.

There have been several measures and government programs put in place to incentivize grain crop cultivation, however, these remain in their initial phase, and it is not yet clear how this will affect planted areas and, subsequently, the crop protection market. Grain crop cultivation is generally undertaken on a less intensive basis than in most other countries in the Americas, partly due to the greater focus placed on fruit and vegetable production.

The 2022/23 season was characterized by drier-than-average conditions, which resulted in some crop damage and water supply shortages. Planted areas for the main maize crop were below average levels, primarily due to lower precipitation. However, yields for the minor crop, which is harvested between May and June, were well above average. Sorghum areas also declined, however, the cereal sector benefited from increased wheat areas and a bumper harvest of the main crop.

Removing glyphosate from the market is expected to result in a shift in weed control practices. This is expected to result in wider use of selective herbicides, potentially boosting the overall value of the herbicides market in the country, evidenced by the latest year in which the herbicide market (+20.6%) outperformed the domestic crop protection market (+16.4%) in terms of year-on-year growth.

Despite the potential requirement to boost production for domestic demand, the country is also increasingly looking to expand export opportunities, with exports of arable produce to Middle Eastern countries, including the UAE, Kuwait, Qatar, and Saudi Arabia, rising significantly in the last decade. China is also becoming a key destination for Mexican exports, including for sorghum, the main cereal crop in the country. Generally, exports focus more on F&V crops and livestock, with grains often diverted for use in animal feed.

In efforts to boost crop production and meet rising domestic and overseas demand, the country has been investing in improving its irrigation infrastructure in recent years, including through increased technification. Mexico ranks sixth in the world regarding irrigated agricultural land, with over 60% of the value of national agricultural production requiring irrigation, including maize, wheat, and sorghum.

Mexico as a country has significant growth potential, with the middle class expanding rapidly. Over the next five years, this middle class is expected to drive increased demand for produce, including fiber for clothing production, and maize, cereals, and oilseeds for use in food production and for animal feed.

The increasing focus on F&V production has benefited the crop protection market in recent years, with this sector expected to continue to expand in the coming years. The high number of biological crop protection products that are being introduced is also expected to drive growth, with this sector in line for rapid expansion, ahead of the growth rates expected for conventional crop protection products.

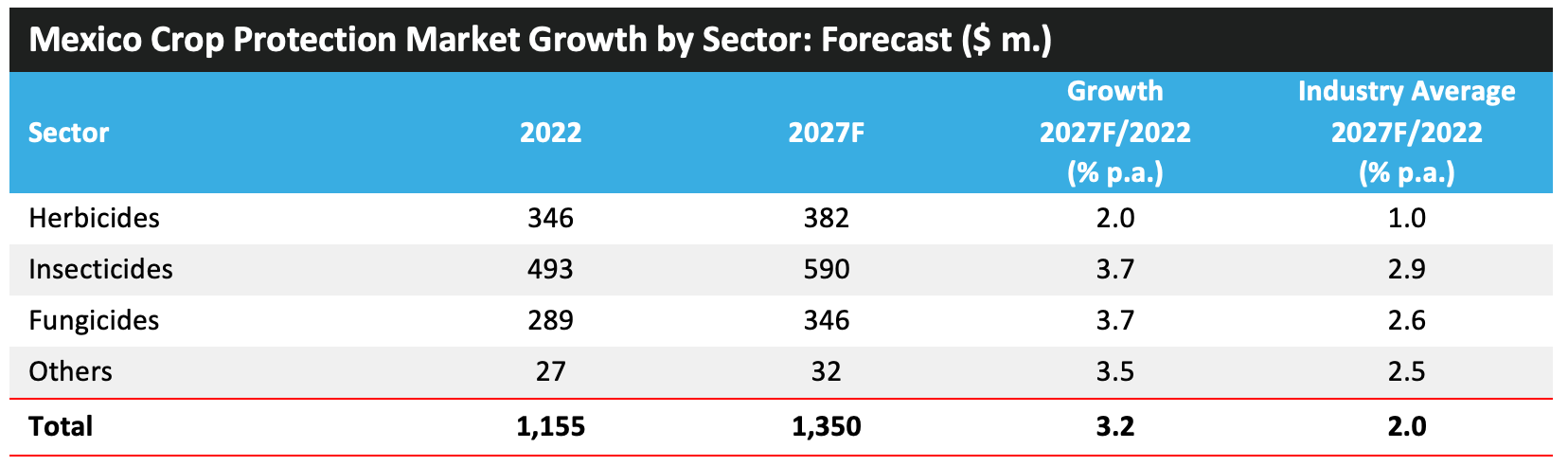

Due to the above factors, the value of the crop protection market in Mexico is expected to increase by an average of 3.2% per annum to reach a value of $1,350 million in 2027. However, this growth could be tempered if the country is afflicted by any prolonged dry spells, as has been experienced in some recent years. Any further advancements towards improving irrigation in the country would clearly mitigate the potential negative impacts of dry conditions.

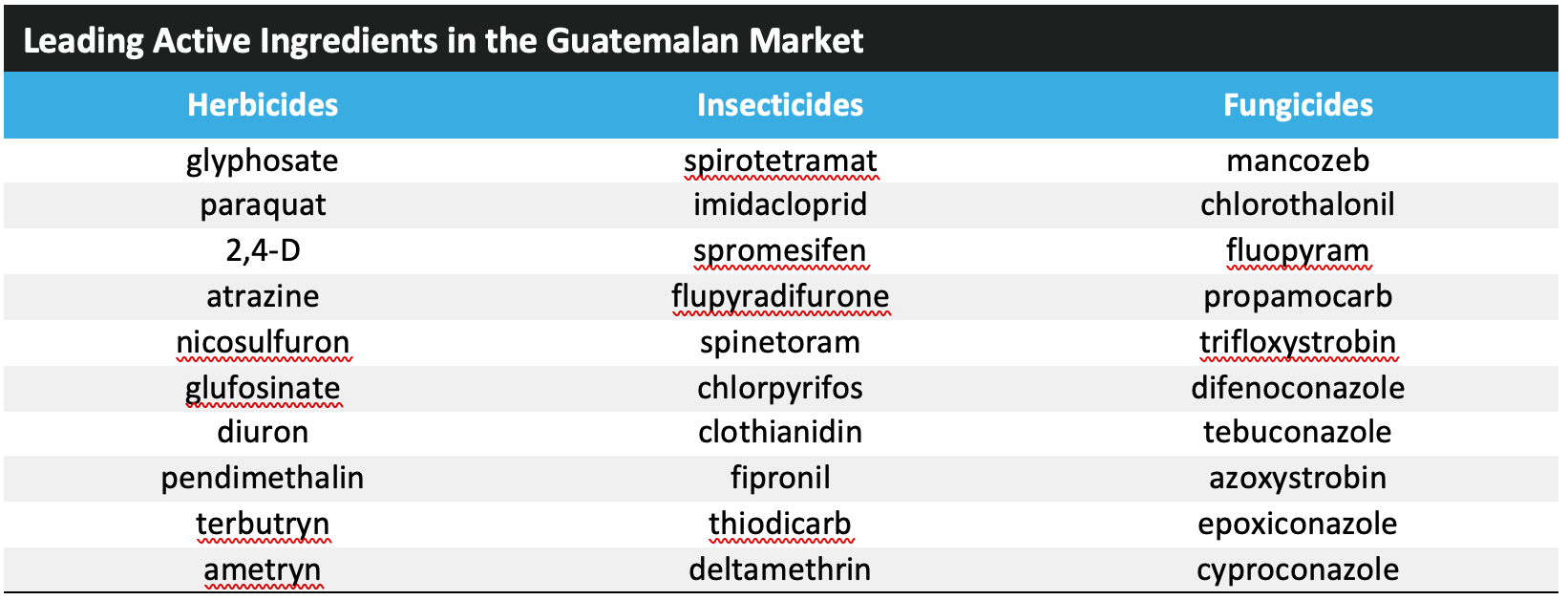

GUATEMALA |

In 2022, the market for crop protection products in Guatemala increased by 15.6% to $185 million. Between 2017 and 2022, the crop protection market in Guatemala increased at an annual average of 11.6%, considerably ahead of the industry average. Crop conditions have generally been positive in recent years, with stable maize areas and production, however in 2022 sorghum production declined by around 10%. The outlook for 2023 is less positive, with the 2023 main season maize crop affected by unfavorable conditions in the main producing regions of Petén and Alta Verapaz. This is due to below‑average precipitation levels during the second quarter of 2023, influenced by the El Niño weather event. Hot and dry weather conditions persisted during July and September, although conditions in the more southerly producing regions were more positive. Preliminary estimates for the crop protection market in Guatemala in 2023 suggest an increase of 2.2% in U.S.$ terms to reach $189 million.

Guatemala is still a country in the earlier stages of development where agriculture accounts for a major share of GDP (13.3%) and export income (32%). Agriculture is developing on two fronts: quality F&V production, mostly for export, and plantation crops, with less of a focus on staple crop production of maize, beans, and rice. The country still has low labor costs that allow it to be price competitive in export markets. Average expenditure on agrochemicals on a $/ha basis is relatively high, likely due to the large share of the market attributable to F&V.

Key trends in production are the increase in the planting of oil palm and melons, but a fall in rubber and sorghum.

The maize area has been essentially static, although there has been a limited improvement for dry beans and the small area of rice.

Compared with other developing countries, Guatemala has a stronger agrochemical active ingredient manufacturing infrastructure, but a significant formulation capability, indicated by 63.6% of imports being of technical material. The major source of product is China, but with more advanced products coming from the EU and U.S. Guatemala is a member of the World Intellectual Property Organisation. Industrial property law is overseen by the Ministry of Economic Affairs Registry of Intellectual Property.

Guatemala is considered one of the highest risk countries in the world from geological activity and climate change, with drought affecting agrochemical market performance in recent years. Cyclones, volcanic activity, and natural disasters are a threat. Poverty and the impact of rising plantation crop production have affected subsistence farmers, with migration from the country a significant issue. However, the continuing increase in the value of crops for export should continue to drive growth of the agrochemical market, particularly if weather conditions are favorable.

NICARAGUA |

In Nicaragua crop conditions have also been relatively favorable over the last two seasons. Conditions in 2023 were also generally positive, with low drought‑related stress to crops. After a decline in 2020, maize output has been on the rise and is expected to reach levels near the recent average. Paddy production is estimated at an above‑average level reflecting an increased use of high yielding varieties and an expansion of planted areas. For sorghum output is expected to be about 20% below the five‑year average, due to a reduction in planted area, as prices of sorghum declined significantly early in 2023 and remained low throughout the year. Planting of the 2024 main season maize commences in May. Current weather forecasts are projecting above‑average rainfall amounts between March and May, which is likely to replenish soil moisture and benefit planting operations.

Agriculture remains a key part of the Nicaraguan economy despite accounting for only 15.8% of GDP and employing 30.6% of the workforce. Agriculture is divided between crop production for domestic consumption and commodities for export. The country enjoys a positive balance in trade in arable products, which account for 18.8% of all exports from the country. Agrochemical usage on a per hectare basis is high compared to other developing markets, although similar to that in the other Latin American countries of Bolivia, Guatemala, and Ecuador.

Nicaragua has a climate conducive to the production of many different crops, ranging from temperate highlands to tropical swampland.

However, concerns regarding climate change are an issue, with dryness affecting both agriculture and the agrochemical market in recent years. As in many developing markets, there is a dichotomy between crops to feed a growing but impoverished local population and crops for export to support the economy.

Nicaragua has only limited agrochemical formulation capability, indicated by only 1% of imports from the U.S., China and India being of technical material. The most significant product sources are China, the U.S., the EU, and India. A substantial amount of product is supplied through companies and formulators based in neighboring Costa Rica and Guatemala. Industrial property law is overseen by the Registro de la Propiedad Intelectual (RPI). Patents and trademarks are granted on a first-to-file basis; patents have a 20-year term. Illicit trade and copy products are a long-term issue in Nicaragua, although the country is a member of the World Intellectual Property Organisation.

The Nicaraguan agrochemical market enjoyed significant and steady growth until the weather-impacted years of 2018 and 2020. The country generally has ample water supply, although distribution is uneven, with heavy rain normal in the Caribbean lowlands. Inland areas are, however, much drier. Water supply management, the responsibility of the Nicaraguan Institute of water, is an issue, and only 10% of arable land is irrigated. Improved irrigation could result in crop yield enhancement. If these issues can be overcome, then continuing growth of the agrochemical market in Nicaragua can be expected. •

Phil Mac Associates LLP trading as AgbioInvestor. Registered in Scotland. Company Number SO306534. Registered Office: Suite 18, Vineyard Business Centre, Pathhead, Midlothian, EH37 5XP, Scotland. A list of members of Phil Mac Associates LLP is available here www.agbioinvestor.com/team

Ingo Bartussek – stock.adobe.com

ink drop – stock.adobe.com

2rogan – stock.adobe.com

eweleena – stock.adobe.com

Derek Oliphant – AgbioInvestor