Global Crop Protection Market Trends Impact on South Africa

12 May 2020

12 May 2020 Africa is the world’s second-largest continent at some 30 million km² covering approximately 20% of the Earth’s land. It is bordered by the Atlantic Ocean to the west, the Indian Ocean to the east and the Mediterranean Sea to the north. The cropping area is vast with an estimated agricultural land area of some 1,100 million ha according to the FAO. This equals 23% of the global available agricultural land area and is on-par with that available for all of the Americas.

Within the continent of Africa there is a diverse range of countries from productive South Africa in the south to more climatically challenging countries in central and Northern Africa. By necessity that diversity leads to the sub-division (OECD) of the African continent into five regions: Northern Africa, Central or Middle Africa, Southern Africa, East Africa, and Western Africa. From an agricultural perspective, however, climate is the key factor in determining which countries make up Southern Africa.

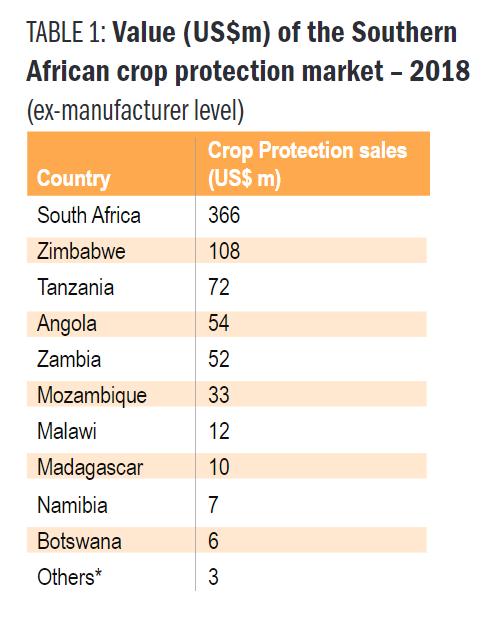

Climatically Southern Africa can best be defined as a “sub-humid and semi-arid climate” and The Southern African Confederation of Agricultural Regions (SACAU) is generally recognized as covering the 12 countries that broadly speaking fall into this climatic region. Accurately quantifying the value of the crop protection markets in each member country is, however, challenging as market research is often incomplete. The latest estimates are, however, given in Table 1.

Climatically Southern Africa can best be defined as a “sub-humid and semi-arid climate” and The Southern African Confederation of Agricultural Regions (SACAU) is generally recognized as covering the 12 countries that broadly speaking fall into this climatic region. Accurately quantifying the value of the crop protection markets in each member country is, however, challenging as market research is often incomplete. The latest estimates are, however, given in Table 1.

Traditionally the region has been the focus of off-patent lower cost products from the “generic” industry rather than from the proprietary side. In 2019 and 2020, however, the increase focus on insecticide sales — in part the due to the fall armyworm (Spodoptera frugiperda) — is beginning to change this as is the raw material price increase of the generics. As such the growth potential and the “price point” of the Southern African market is beginning to become more attractive to both generics and R&D companies alike.

South Africa — A Growth Market for Crop Protection Products

South Africa is the focus of this article given the dominance of the country within the region of Southern Africa.

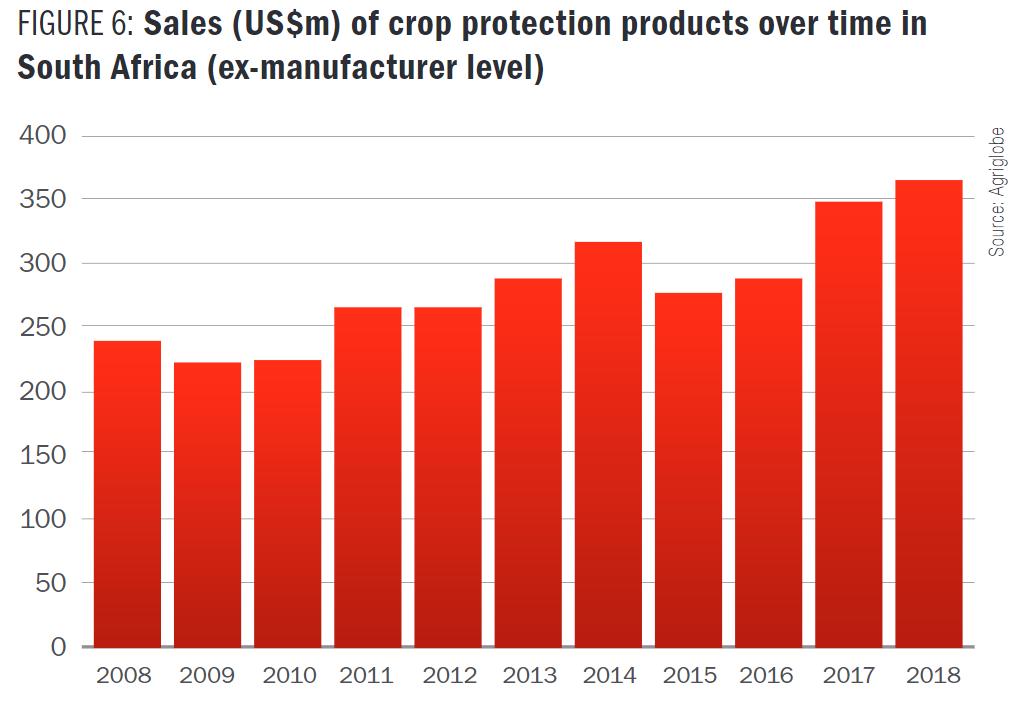

As published in the June 2019 issue of AgriBusiness Global™ the global crop protection market in 2018 increased at a rate of 2% in nominal terms over that of 2017. As a comparative figure the South African country market grew by close to 5% in 2018 as compared to 2017; so, in effect more than twice that of the global average. South Africa has also considerably outperformed the global market growth with a CAGR of 4.4% per annum over the time period 2008 to 2018 as compared to a more modest CAGR of 2.3 % per annum for the global market over the same time period.

As published in the June 2019 issue of AgriBusiness Global™ the global crop protection market in 2018 increased at a rate of 2% in nominal terms over that of 2017. As a comparative figure the South African country market grew by close to 5% in 2018 as compared to 2017; so, in effect more than twice that of the global average. South Africa has also considerably outperformed the global market growth with a CAGR of 4.4% per annum over the time period 2008 to 2018 as compared to a more modest CAGR of 2.3 % per annum for the global market over the same time period.

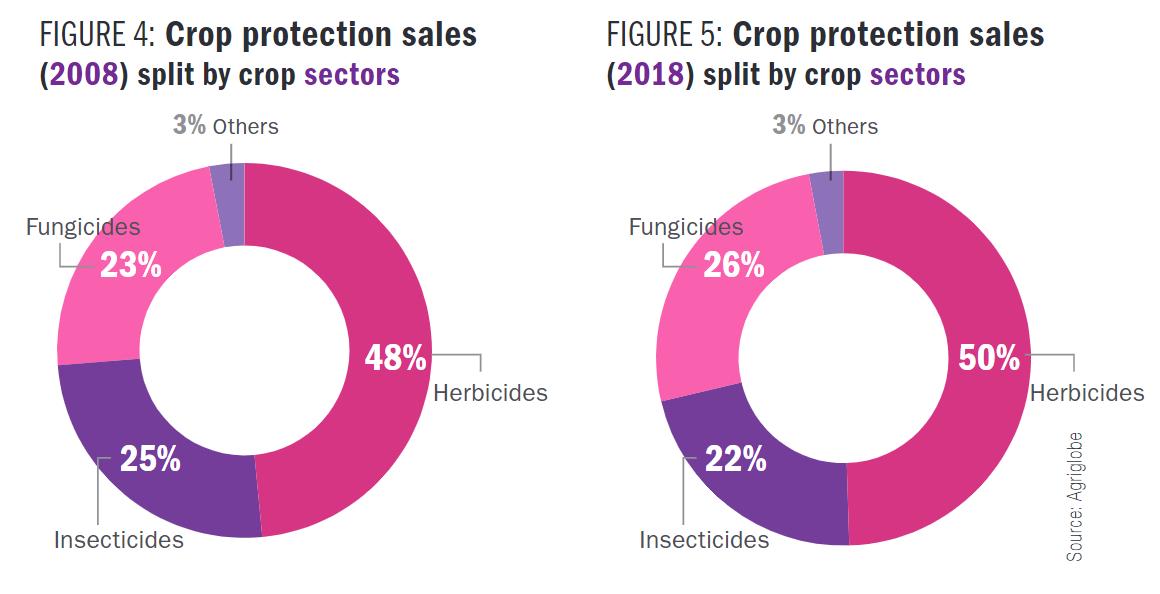

South Africa, like most markets, suffered a decline in 2009 (as a result of the financial crisis) and then once again in 2015, when among other factors a marked decline in commodity prices took place. The recovery in 2016 and 2017 was, however, quite marked (see Figure 6). In addition to increasing in value, the market also changed somewhat and became less focused on insecticides when comparing 2008 sector splits with those from 2018 (Figures 4 & 5).

South Africa, like most markets, suffered a decline in 2009 (as a result of the financial crisis) and then once again in 2015, when among other factors a marked decline in commodity prices took place. The recovery in 2016 and 2017 was, however, quite marked (see Figure 6). In addition to increasing in value, the market also changed somewhat and became less focused on insecticides when comparing 2008 sector splits with those from 2018 (Figures 4 & 5).

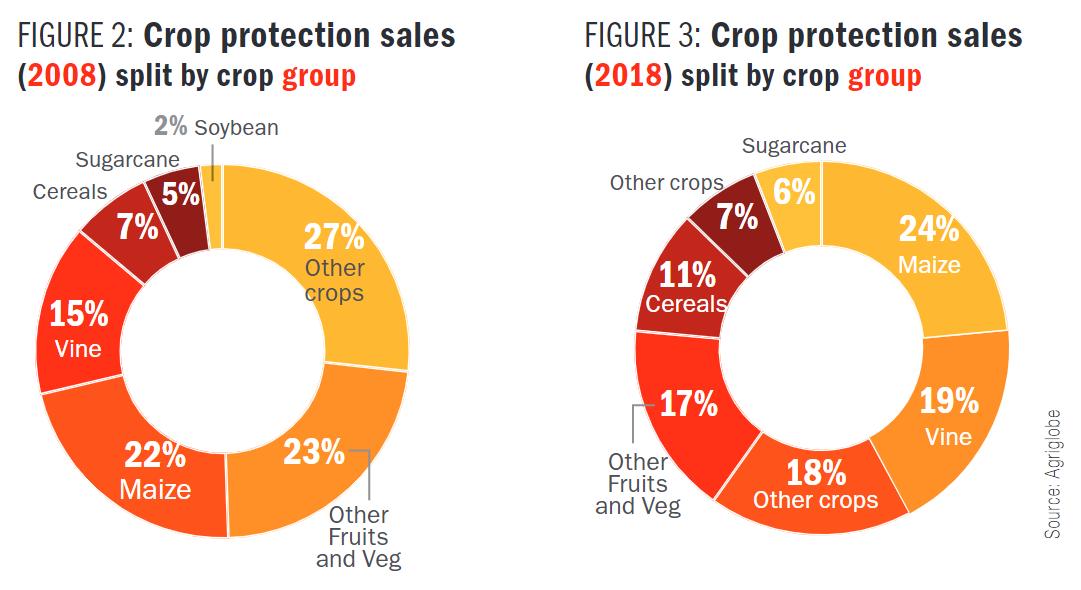

The most striking development of the domestic market over the period 2008 to 2018 is the growth in those crop groups in which the produce is destined for the export market rather than domestic use. Most noticeable in this is soybeans, which in 2008 accounted for sales of crop protection products of just 2%, whereas in 2018 this had grown to over 7% of the total CP market. Crop area planted to soybeans over the same time period also increased from just over 160,000 ha in 2008 to close to 800,000 ha in 2018 (Figures 2 & 3). The growth in the relative value of maize, vine, cereals, and sugarcane are more, however, a reflection of a general increase in intensity of product use (particularly fungicides) rather than any significant change in crop area.

The most striking development of the domestic market over the period 2008 to 2018 is the growth in those crop groups in which the produce is destined for the export market rather than domestic use. Most noticeable in this is soybeans, which in 2008 accounted for sales of crop protection products of just 2%, whereas in 2018 this had grown to over 7% of the total CP market. Crop area planted to soybeans over the same time period also increased from just over 160,000 ha in 2008 to close to 800,000 ha in 2018 (Figures 2 & 3). The growth in the relative value of maize, vine, cereals, and sugarcane are more, however, a reflection of a general increase in intensity of product use (particularly fungicides) rather than any significant change in crop area.

Outlook for 2020

Agronomically 2020 is anticipated to be a favorable year. Despite late planting, due to rainfall deficits, South Africa’s corn and sunflower production estimate has been pushed higher after good weather boosted yields. Specifically, rainfall in December 2019 and January 2020 led to an increase in soil moisture reserves and so minimized the impact of the earlier dry weather conditions at planting. Larger corn planted area will also provide a boost to 2020 crop protection product use. Weather forecasts for the February‑April 2020 period indicate that the cumulative amount of rainfall is likely to be average, underpinning the favorable expectations for most crops.

The outbreak of Foot and Mouth Disease in South Africa in November 2019 is a concern as it potentially reduces the demand for feed grain for livestock throughout all of 2020. Early indications are, however, that the outbreak is under control and restricted to Limpopo Province. Nevertheless, the development of the disease as well as ongoing Land Reform policies both have the potential to disrupt and provide uncertainty to the prospects of the South African market going forward.