Live from Vegas, Day 2: After the M&A Dust Settles

9 August 2017

9 August 2017

Alex Polinsky (right) and Jim DeLisi explain what’s driving the most recent round of M&A activity, the ongoing impact it will have on the industry, and where we’re headed over the next several years.

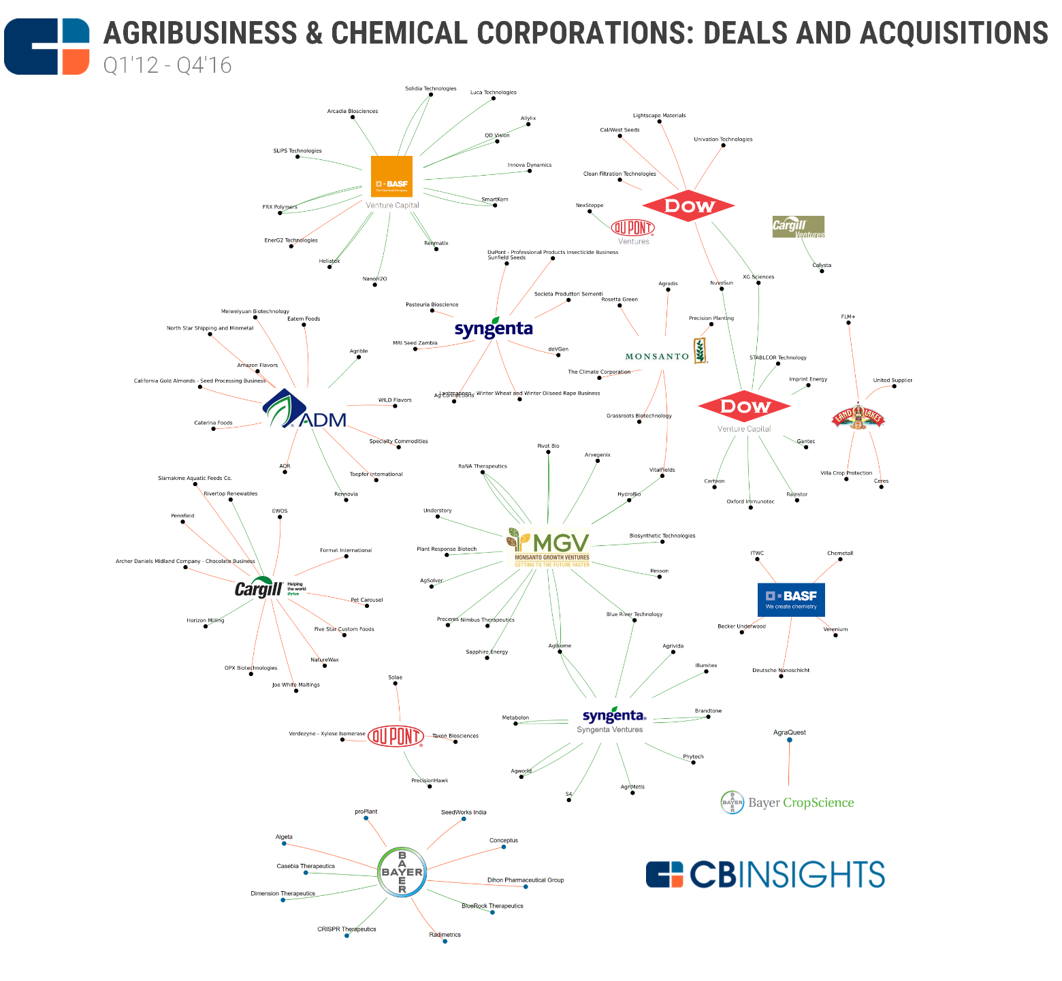

In their Wednesday morning session kicking off day two of the AgriBusiness Global Trade Summit – Americas, Jim DeLisi, owner of Fanwood Chemical, and agchem industry veteran and consultant Alex Polinsky, took a historical look at merger and acquisition activity in the agchem market and shared what the landscape will look like when the most recent round is over.

That is, at least until the next M&A wave starts – probably 15 years from now, a continuation of the cycle of the last nearly half-century.

When the current merger activity dies down, control over the agchem industry by the top three new companies will be extensive, DeLisi said. He expects BASF, which has a reported $50 billion to spend in the space, will make a move at some point soon, likely on the sought-after glufosinate/LibertyLink assets that Bayer is poised to divest in order to satisfy regulatory authorities. Syngenta/ChemChina is probably the only other realistic bidder for the assets.

The new Bayer/Monsanto is widely expected to dominate the space once the dust settles in 2018, with ChemChina/Syngenta coming in at number 2 and Dow-DuPont close behind. BASF is projected to occupy a distant fourth, followed by FMC, with its acquisition of DuPont assets, at number 5.

Rounding out the top 10 players in the agchem space: Nufarm, UPL, Platform Specialty, Albaugh, Sumitomo, and AMVAC. The next five are likely all to be Chinese manufacturers, DeLisi said.

With U.S. agribusiness having lost a staggering $15 billion in value from 2008 through 2016 on the back of spiraling commodity prices, Polinsky discussed the need for innovation to continue – M&A, essentially, represents the path of least resistance to keep revenue and profits high enough to support more R&D.

Mergers are also set to consolidate the distribution phase of the industry as everyone aims to get more out of the supply chain to drive profits back to their former healthy state, he said. On this front, keep an eye on two companies that could present the so-called “Amazoning” of the agchem industry: FarmTrade and Farmers Business Network (FBN).

“Firms like these could flatten the supply chain and might be the beginning of the ‘Amazoning’ for grower supplies,” DeLisi said. “If the Chinese government does succeed in helping the export of finished and formulated products and gets into this kind of distribution network, it could eliminate a lot of costs involved in getting things to market.”

He added: “There is no doubt that the internet is coming to ag chemicals in a much bigger way.”