Chile Fast Becoming an Export Destination for Agrichemicals

13 August 2018

13 August 2018 That the global crop protection market did indeed turn a corner in 2017 is now confirmed as data from the last few outstanding countries has become available.

Five months into 2018 there are very few unprocessed data sets remaining that could swing the needle much from the current estimate. That growth estimate, although not earth-shattering, is for an increase of close to 1.8% from the relatively low base of $53 billion in 2016. On that basis the Global Crop Protection market in 2017, when measured at ex-company level and using average-year exchange rates, will come in just over the $54 billion mark.

The contrast of market growth as compared to declining sales of the leading multinational companies shows that 2017 was not a normal year in this respect, and the overall market performed rather better than the multinationals.

Buy-back out of over-burdened channel inventories primarily in Latin America but also in other territories is cited as a key contributor to this apparent contradiction. It is also clear that many of the smaller generic companies performed well. Sales of the leading Chinese companies (export and domestic) increased by close to 20% in local currency, dampened somewhat by currency movement when expressed in U.S. dollar terms. China Pesticides PLC was not slow to capitalize during the “merger year” while focus of the multinationals was elsewhere.

One market in which this was particularly apparent was Chile. Import statistics from 2017 show that nearly $100 million of final formulated product was imported out of China into Chile. Very little if any of this was re-exported. Compared to 2016, that import value rose some one-and-a-half times, making Chile one of the fastest-growing export destinations in 2017. Only Paraguay and South Africa, as defined usage markets, showed a faster growth rate of imports in 2017 as compared to 2016. That growth puts Chile as the 15th largest for Chinese-formulated product in 2017 as compared to the 17th largest in 2016, again expressed in value terms. Volume of technical imports saw at least a similar increase.

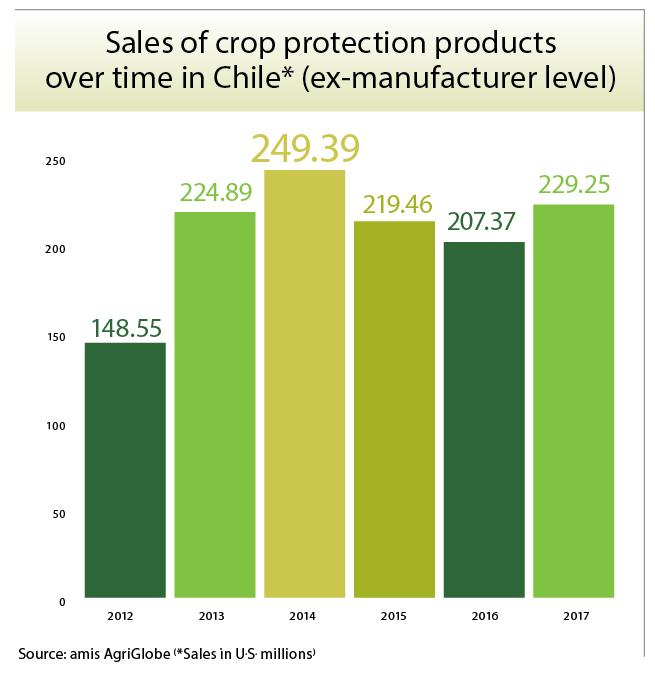

In line with global markets, Chile saw a decline in 2015 and once again in 2016 in value terms. The market recovered somewhat in 2017, helped by the strengthening of the peso against the U.S. dollar. Although still preliminary, the latest 2017 figures estimate the Chilean market to be valued at just under $230 million at ex-manufacturer level. Although margins and markups at each distribution step from manufacturer to end-user are not especially high, the relative complexity and number of steps within the distribution system does mean end-user level value is considerably higher.

Despite the fact the Chilean market overall is dominated by generic material, the vine fungicide market in particular is one that remains the focus of the multinationals. Data from Kleffmann 2017 end-user panels show that proprietary formulations based on boscalid and pyraclostrobin, as well as those based on cyprodinil/fludioxonil, dominate in terms of market share.

There is also a significant presence of biologicals. The insecticide sector is more of a mixed bag, with proprietary formulations based on spirotetramat and spinetoram important, but also more generic formulations of acetamiprid, buprofezin, and fenpropathrin significant. Overall in terms of product mix, the insecticide and fungicide sectors are as developed in their product use as the traditional European vine-growing areas of the world. The herbicide market, not surprisingly, is dominated by commodity products and is very much a generic market, with the remainder of the market a relatively complex mix of plant growth regulators, in which both multinationals and generics are important.

Editor’s note: Analysis provided by Kleffmann Group is based on data collected from farmer surveys, interviews with distributors in emerging markets, proprietary market trend studies, subject matter experts, and open-source information. The farmer surveys continue to provide the bulk of the data for the analysis, although the group’s program of “trend studies” is becoming more significant. For more information, visit kleffmann.com.