India Boasts Fastest-Growing Significant Crop Protection Market

19 December 2018

19 December 2018 As presented at the Agribusiness GlobalSM Trade Summit in Phoenix, Arizona, in August, the global crop protection market in 2017 increased at a rate of 1.9% in nominal terms over that of 2016.

As such, the market for crop protection products in 2017, when measured at ex-manufacture level and using average year exchange rates throughout, comes in at $54.15 billion. That the market had, in fact, seen positive growth in 2017 of close to 2% had been predicted in January 2018.

A 2% growth rate, while not earth-shattering, is an important milestone in that it does bring to an end, quite abruptly, the period of decline seen in 2015 and 2016. This fact, rather than the absolute size of the growth, is important in a sector that has seen so much merger and acquisition activity, in that it provides confidence to the wider investment community.

That “confidence” has been needed was all too apparent in the week of 10 August 2018, when share prices for companies across the board collapsed on the back of negative court rulings out of California regarding glyphosate. Share prices are now slowly recovering, but it does illustrate all too clearly the importance of a “unified strong and positive message” on the benefits of crop protection to the global economy.

In looking for a first positive message for the global crop protection industry, one needs to look no further than India. The country is often reported as the fastest-growing world economy. According to the World Bank, the Indian economy will see a robust GDP growth of 7.3% in this financial year and 7.5% the next two years as “factors holding back growth in India fade. These figures allow India to retain the tag as the world’s fastest growing major emerging economy and one that has consistently been a good couple of points over and above the global GDP growth rates since the financial crash of 2009.

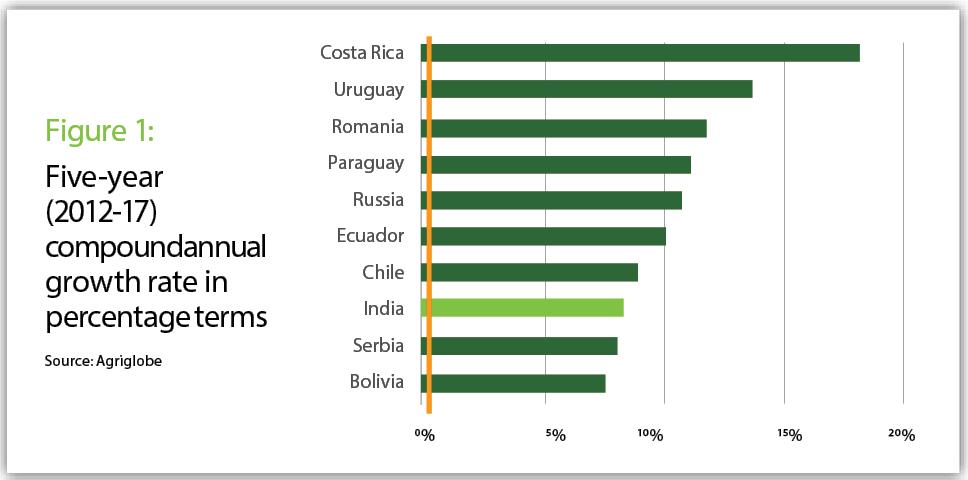

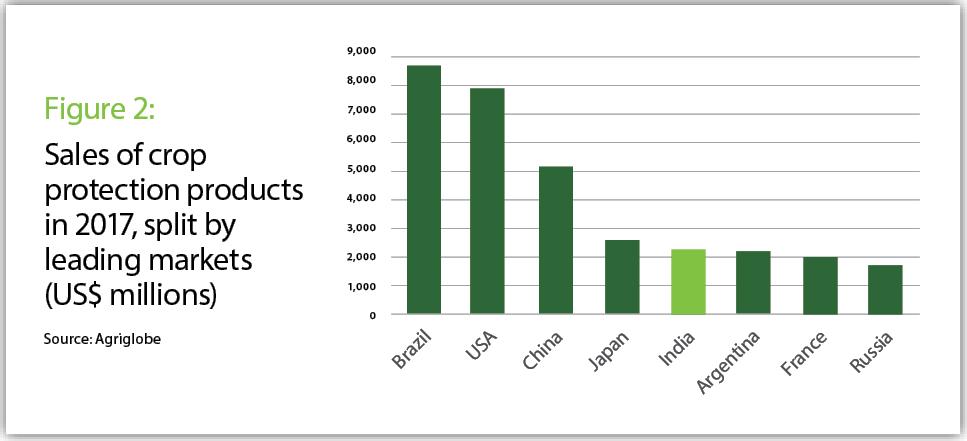

The same can be said to be true for the crop protection market. While India is not the fastest-growing market over the last five years (that particular tag goes to Costa Rica), India can be said to be the fastest growing market of significance (Figures 1 and 2).

While position No. 8 out of 10 is not in the top flight when the sheer size of the Indian market (as fifth largest globally) is taken into account (Figure 2), it is clear that, as with the macro-economics of GDP, India can be considered as the fastest-growing world agrichemical market of significance, with only Russia coming close.

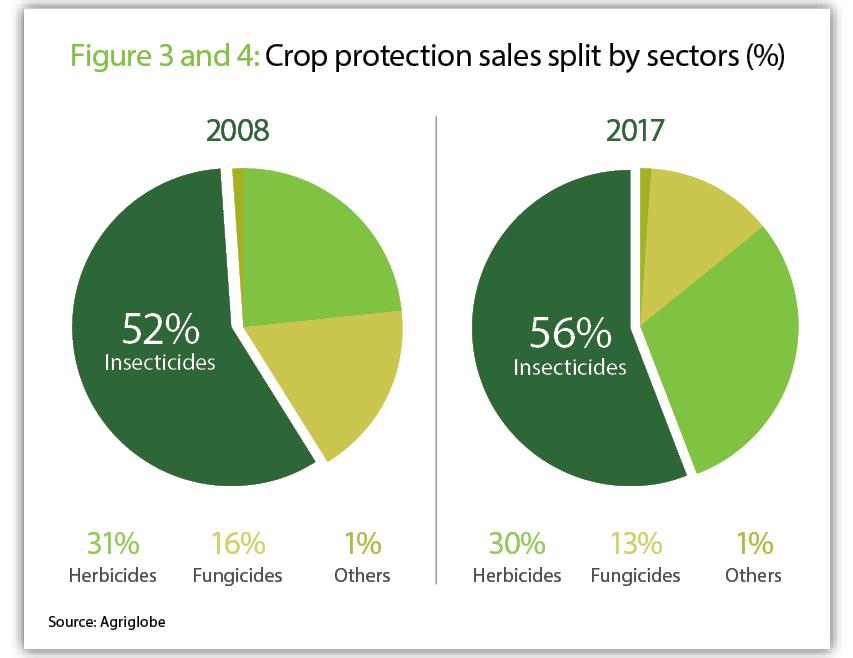

India, like most markets, suffered a decline in 2009 (as a result of the financial crisis) and then again in 2015, when among other factors a marked decline in commodity prices took place. India, however, suffered less than most markets and came out of this 2015 decline in 2016 rather than 2017, a testament to the resilience of the Indian market. However, how much the market is developing is a more moot question. If we look at the splits between the sectors between the 2008 base year as compared to 2017, the market is largely of the same structure (Figures 3 and 4).

A simple comparison of Figures 3 and 4 shows that the market has over the last 10 years or so remained insecticide dominated, with essentially no additional penetration from the other sectors, including fungicides. If we also take into account the impact of Bt cotton in this market, it could reasonably be argued that insecticides had significantly strengthened their position at the expense of the other sectors.

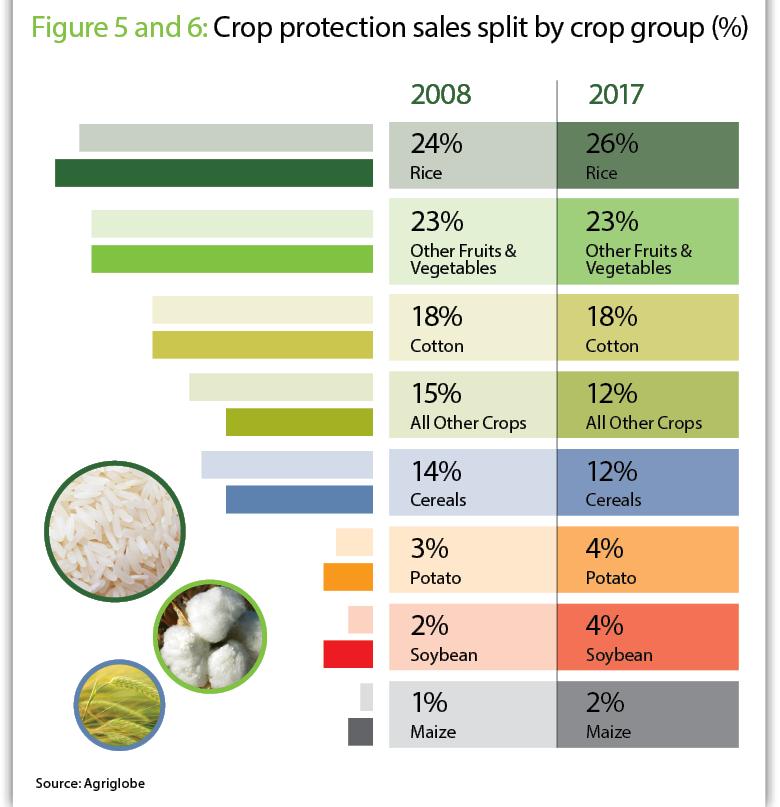

The same is true if we compare the relative significance of the different crop groups in terms of pesticide spend as in Figures 5 and 6.

Essentially the market in 2017 is the same as it was in 2008, with an appreciation in the relative importance of rice. While not necessarily an issue, the lack of market penetration by crops other than rice in India needs to be put into context with other developing markets (so for example the rise in soybeans in Brazil over this time period) and the success of other Asian markets in rice reduction programs. As one final measure of market development, if we look at the share of imported foreign formulated pesticides in value terms, that proportion has stayed persistently under one-third of the total market value despite the launch of many new molecules specifically targeting the rice sector in this time period.