Crop Protection Market Development in Latin America

Scroll Down to Read

By Derek Oliphant

By Derek Oliphant

Co-Founder

AgbioInvestor

This article will outline the development of the crop protection market in Central and South America, examining the current situation as well as the key future trends expected to influence market development over the next year.

Market values are Agbiolnvestor’s estimates of the value of crop protection products used on the ground in the agricultural year, expressed in US$ terms at the ex-manufacturer level. For southern hemisphere countries, the agricultural year is approximately July to June, for example ‘2023’ refers to the value of products used on the ground between July 2022 and June 2023.

The most recent full data year available is 2022, with preliminary estimates provided for 2023, as well as outlook for the 2024 season, which is currently underway.

The most significant factors which affected the crop protection market performance in 2023 were:

- Recovery from adverse weather (e.g. U.S., Europe).

- Very dry conditions in southern South America; dryness in parts of Asia (e.g. Indonesia) but more favorable in other countries (e.g. Vietnam); dry in Midwest U.S.; favorable in EU.

- Declining agrochemical prices, non-selectives, and Asia Pacific worst affected.

- Commodity prices lower than 2022 but remain high by historical standards.

- Fertilizer and energy costs fell from peaks in 2022, but still high.

- High inventories driving a disconnect between ex-company sales and usage on the ground:

- Inventories built up due to high levels of pre-purchasing to alleviate supply concerns and unfavorable mid- to late-season weather on key regions (Western U.S., Europe).

- Retailer and on-farm stocks now being used, with usage on the ground sustained due to relatively high pest pressure and improved conditions in aforementioned regional markets.

- Company sales also impacted by overall reduction in agrochemical pricing, but worst effects of reduced prices expected to impact market on-the-ground in 2024.

| Latin America Crop Protection Market Overview 2023 |

In Central & South America, La Niña conditions led to severe dryness and high temperatures in Argentina, Paraguay, and southern Brazil, impacting soybean production in particular. Large areas of Argentina have also been impacted by wildfires. The ongoing drought conditions in the region have also had an impact on logistics, with the water level in the Paraná River in Rosario, Argentina, at its lowest level since 1945. However, wetter conditions in less southern regions of Brazil, while benefiting yields, also led to increased pest pressure, particularly of whiteflies and white mold. The wet weather restricted field access for farmers, limiting the opportunity to apply pest control products in a timely manner. In addition, large areas of soybeans in key growing regions were affected by seed rot, while corn leafhopper pressure was significant in the Safrinha maize crop in Brazil.

In 2023, dry conditions have impacted large areas of the region, particularly in Argentina, with this expected to be a significant negative, particularly as crop abandonment in the worst affected areas has been high. However, conditions in the key crop protection market of Brazil were more positive, and higher crop areas and pest pressure boosted volume usage. According to Sindiveg, the Brazilian crop area treated with pesticides increased by 13.4% in the first quarter of 2023, with this being a key application time in the 2022/23 agricultural year. While the falling prices of key agrochemicals, notably glyphosate and glufosinate, depressed the value of the market compared to 2022, prices during the early part of the 2022/23 season were still high by historical standards so the worst impacts on market value are not expected to be felt in this current year.

The crop protection market in Central and South America benefited from a continued strong ag economy in Brazil, despite the impacts of dry conditions on soybean output and more recently cold conditions for Safrinha maize.

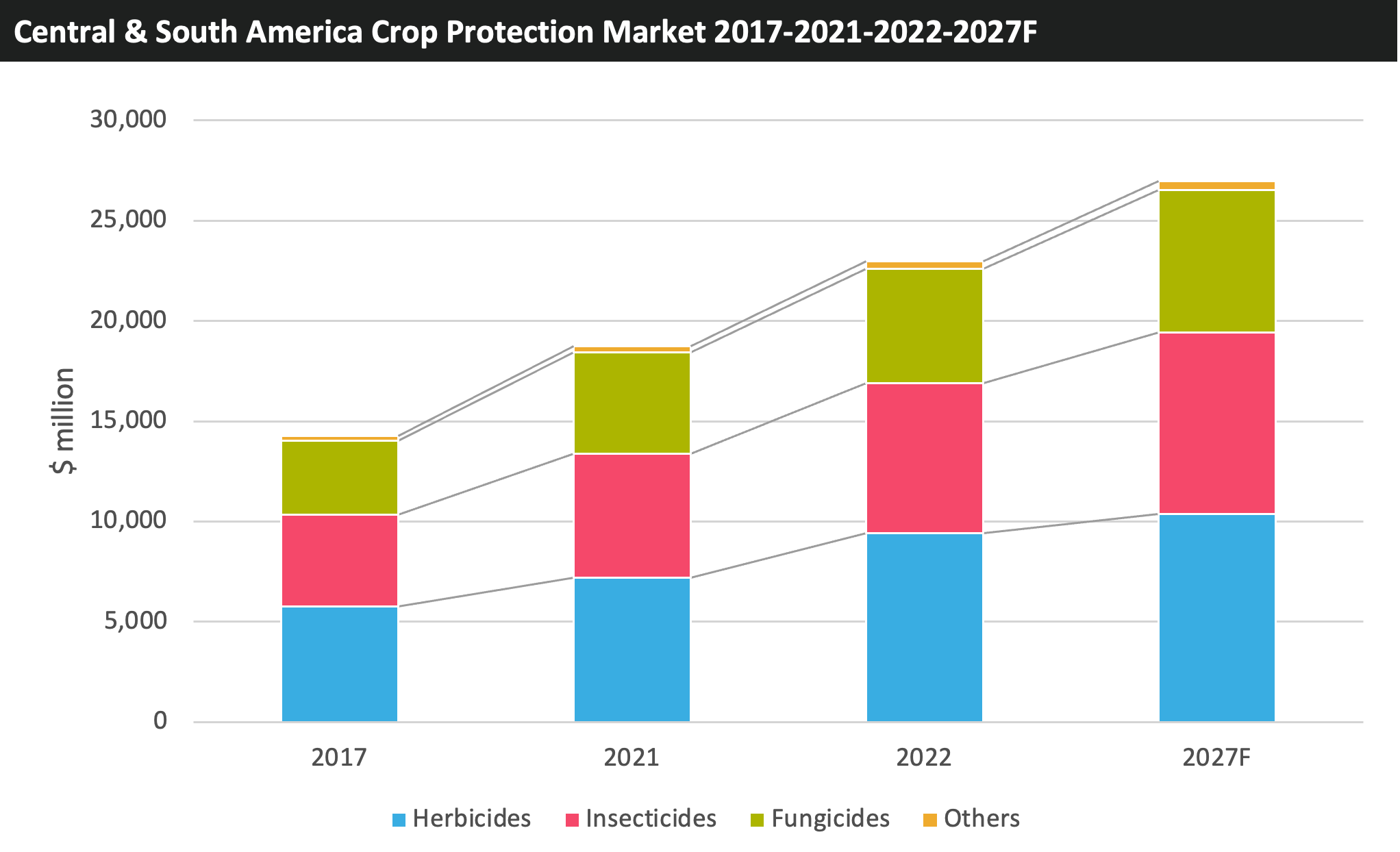

These factors have been largely offset by the higher planted areas for most key crops, as well as high pest pressure in more northern regions, where wetter weather has been more conducive to disease pressure. Argentina is slightly more negative, where the weather has had more of an impact across all key crops. In other countries, dry weather also impacted Paraguay and Mexico, although positive conditions prevailed in other notable markets such as Chile, Colombia, and Bolivia. As a result of the above factors, we expect the value of the crop protection market in the region to have increased 9% in nominal terms in 2023 to reach $25,045 million.

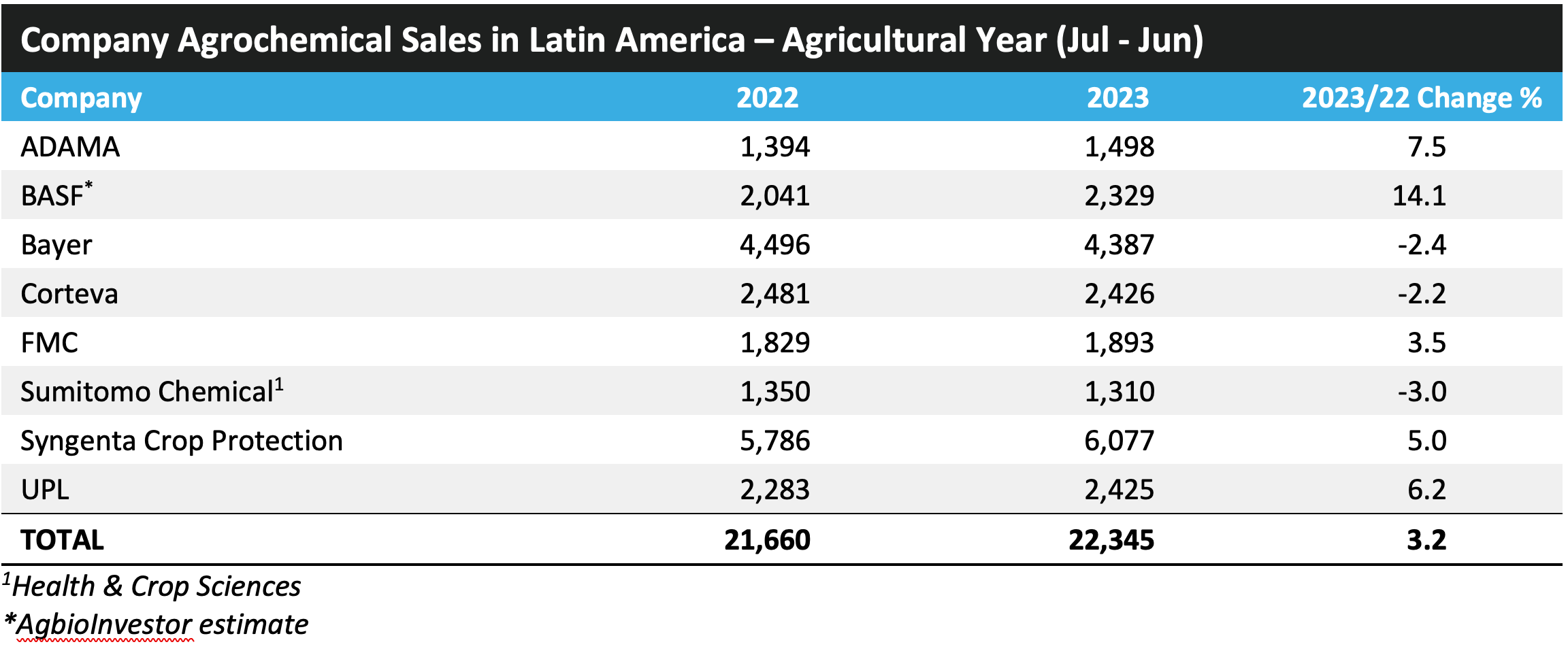

The table below outlines the sales performance of the leading agrochemical companies in the agricultural year in Latin America in the agricultural year 2023 (July 2022 – June 2023):

| 2023 Market Expectations |

The crop protection market in 2023 was relatively flat in terms of value development, with the impacts of lower agrochemical prices and unfavorable weather conditions in certain regions holding back growth. However, this was offset by:

- positive conditions leading to recovery in much of Europe;

- a strong ag economy and market in Brazil, where the impacts of price declines were not fully felt during crop protection product purchasing times;

- improved weather in the Western U.S.; and

- high pest pressure in key country markets, notably Brazil and China.

However, the market in 2024 can be expected to decline as the full impacts of falling agrochemical prices are felt in Central and South America and the continuing impacts of the El Niño weather event are felt in much of Asia Pacific. In addition, expectations for lower areas of certain key crop and country markets (e.g. cereals in France and Argentina; maize in Brazil and the U.S.; cereals and canola in Australia) can be expected to impact the market in 2024.

It can be expected that company performance in 2024 will benefit from the stabilizing inventory situation as we move into 2024, with sales in 2023 being hampered by high supplies in many regions, notably the U.S. and Europe. However, the effects of reduced agrochemical pricing are expected to continue, particularly in southern hemisphere countries such as Brazil in 2023/24.

The key factors behind the assumptions for decline in 2024 are:

- Low agrochemical prices.

- El Niño leading to dry conditions in much of Asia Pacific.

- Declining commodity prices.

- Logistical issues in certain key shipping locations (e.g. Panama Canal, Mississippi River, Rhine).

- Weather impacting Brazil (although rust pressure higher than previous year).

| Central and South America |

- Brazil soybean area expected to be up by 2.8%, but maize down by 5.3%. Overall crop area expected to be up by 0.4%.

- For soybean, a number of factors are expected to impact crop development, including:

- key regions impacted by hot and dry weather, with some areas requiring to be replanted and expectations for yield impacts.

- soybean planting commenced earlier than usual at request of cotton growers to provide larger window for Safrinha cotton planting, leading to concerns over increased rust and disease pressure.

- Sugarcane area and production expected to be up sharply, benefiting from favorable weather and recent investments in the sector to support ethanol production.

- Expectation for historically strong El Niño, potentially ranking in the top five strongest El Niño events on record.

- Brazil soybean crop impacted by weather.

- Plantings disrupted in some regions by wet conditions.

- Growers advised to extend planting schedule.

- Asian rust pressure rising.

- ~5% of crop in Mato Grosso required replanting due to hot and dry conditions.

- Safrinha maize area in Brazil expected to be negatively impacted by delayed soybean planting.

- Export prospects of Safrinha maize lowered due to low water level of Amazon River, hampering logistics.

Argentina impacted by dry weather, with soil moisture not yet replenished following last years’ severe drought.

In Brazil, the progress of the 2023/24 soybean crop is behind last year, and also behind the five-year average at this stage. While the crop benefited from recent rainfall, dryness remains a concern across many regions. Hot and dry weather has negatively impacted soybean development and accelerated maturity, while erratic rainfall distribution means that the crop condition is highly variable. The soybean crop cycle was shifted earlier this season following a petition to the Ministry of Agriculture from cotton producers to allow more time for Safrinha cotton planting after harvest, with the ideal Safrinha cotton planting window closing around the end of January. This caused some agitation among soybean and maize producers concerned about the impact the earlier season on rust and disease pressure. Since 2006, a soybean-free period to mitigate Asian soybean rust has been implemented in key regions, as the pathogen is viable for approximately 60 days without a host plant.

The Paraná Agricultural Defense Agency (Adapar) advised soybean producers, especially in the Southwest, South and South-Centre Zones of the region, to extend the planting schedule for soybeans until 31 January 2024, following a request from growers. The measure considers the impact of wet weather earlier in the season, which made planting in these areas difficult. Adapar is encouraging growers to remain vigilant in monitoring Asian rust and adopt the control measures recommended by technical assistance professionals in their respective regions.

Unusually hot and dry weather in Mato Grosso has severely impacted newly planted soybeans and could lead to growers who intended to plant a second crop of cotton after this soybean crop now choosing between replanting the worst affected soybean areas or switching to full-season cotton, with this causing a potential reduction in soybean acreage in the state, but to the benefit of cotton. Drought conditions in the north of Brazil, which are causing low water levels in some of the upper tributary rivers of the Amazon River, have also led to concerns regarding export prospects for the Safrinha maize crop. If the dry weather persists, there is a risk of shipping costs rising in Brazil without a corresponding boost in global prices, which could exert financial pressures on local farmers and traders.

However, some benefit to growers could be provided by the significantly reduced water levels in the Panama Canal following severe drought conditions associated with the onset of El Niño. This has limited the number of ships able to pass through the waterway. Historically dry conditions, including the region’s driest October on record, have caused water levels in Gatun Lake, the main source of water used in the canal’s lock system, to fall considerably. As a result, the Panama Canal Authority has reduced the number of daily transits from 29 to 25 ships, with this to be further limited to 18 ships a day in February 2024, representing 40%-50% of the Panama Canal’s usual full capacity. In response, bulk grain shippers transporting crops from the U.S. Gulf Coast export hub to Asia are reportedly sailing longer routes and paying higher freight costs to avoid vessel congestion and record-high transit fees. These higher costs have the potential to reduce demand for U.S. maize and soybeans suppliers and benefit markets less reliant on produce moving through the Canal, such as Brazil.

In addition, the Safrinha maize area in Brazil is expected to be negatively impacted by delayed soybean planting in west-central Brazil and the state of Tocantins, as soybeans planted after 1 November will not allow enough time to plant Safrinha maize within the ideal planting window. In addition, low domestic maize prices are also discouraging Safrinha maize plantings. Brazil’s Ministry of Agriculture estimates that the combined area of Brazil’s three cultivation seasons for maize is to fall by 5.6% in 2023/24, however based on early indications of seed and fertilizer sales, the decline could be as much as 20%.

Recent heavy rainfall in southern Brazil, associated with the onset of El Niño conditions, is expected to favor the development of key soybean diseases, including Asian soybean rust and damping-off.

The number of soybean rust cases in Brazil more than doubled between November and December, with current weather conditions favoring the development of the disease.

The rise in cases is likely to have been driven by the recent development of El Niño conditions, which are associated with milder and wetter winter conditions in South America, and the earlier start to the soybean season, which shortened the soybean-free period and potentially provided reservoirs for viable pathogens to persist.

In Argentina, agricultural trade has been impacted by a lack of soybeans as a result of drought and farmers holding onto produce due to expectations that the Argentinian peso will weaken following recent electoral results. The country’s 2022/23 maize and soybean crops were impacted by severe drought conditions associated with the La Niña event, with production declining by 30.5% and 43.2% respectively. In 2023/24 the soybean area in Argentina is expected to rise by 3.8%, with higher areas also forecast for cotton (+9.4%), rice (+3.1%) and peanuts (+5.4%). The area under maize is projected to fall by 1.0%, with area declines also expected for wheat (-5.1%), sunflower (-14.0%) and barley (-11.1%).

Paraguay was also negatively affected by dry weather conditions related to La Niña in 2022/23, and there were concerns moving into this current season as southern regions were affected by heavy rainfall while northern regions experienced hot and dry conditions with much of the soybean crop requiring replanting. However, weather has recently improved such that production expectations have been raised, with expectations that this could be raised again if the favorable weather is maintained.

For 2024, agrochemical price reductions stemming from a normalization of supplies, particularly from China, and the impacts of high inventories can be expected to depress the value of the market. However, weather conditions in regions such as Argentina and southern Brazil are expected to be much improved, with crop production in Argentina expected to rebound from the severe declines experienced in the drought-ravaged 2022/23 crop. Th El Niño climatic event is typically associated with increased rainfall in parts of southern South America, which is expected to alleviate the extreme dryness which has affected these regions during the La Niña phase.

For Brazil, while the declining prices are a key concern for market value in 2024, the soybean area is expected to increase again, and the country is expected to further solidify its strong position as a supplier of key crop commodities to export markets, primarily to China. This is expected to continue to benefit the crop protection market moving forward, although a further negative for 2024 is the delayed soybean harvest and subsequent impact on the maize area. •

Derek Oliphant – AgbioInvestor

Join us at AgriBusiness GlobtalSM LATAM Conference on 14-15 May in Panama City, Panama, to explore new business opportunities and establish relationships with key players in the LATAM region. Register early to save and set the groundwork for generating new business and partnerships in Latin America! ABGLATAM.com