China’s $6-Billion Market Continues its Volume Growth

30 April 2016

30 April 2016

Dr. Nomman Ahmed is the Regional Manager of Asia/Pacific

The Chinese Market was flat in harvest year 2015 compared to the previous year, according to recent farmer-level data collected in China by Kleffmann panel surveys. This analysis is also generated by analyzing the market using data from amis AgriGlobe, which includes a multitude of sources including distributor studies (amis Trend), expert interviews, and national association data.

But China’s flat performance in U.S.-dollar terms is more positive than most markets considering the rest of the world’s average 10% decline. China’s crop protection product (CPP) consumption increased, but like much of the world, CPP price softness and devalued local currency pulled value out of the market and the industry.

Farmers in China applied slightly higher volumes of crop protection products in 2015, but value growth was consumed by a falling RMB. The industry did not feel this marginal growth due to higher stocks lower down the chain. 2013 and 2014 were fantastic years for the global and Chinese crop protection market, and the general outlook was positive. Thus — in expectation of a similar market performance in the year to come and slightly higher and increasing prices for key technical material at the end of 2014 — a small stockpiling started in China, especially at the tail end of the distribution chain.

In 2015, it is believed CPP inventories were reduced by 5% to 15% compared to 2014, and the stockpile was most pronounced at the retailer level.

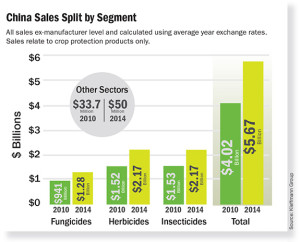

Overall, the crop protection market value rose 0.2% compared to last year to $6.09 billion at ex-manufacturer level amid the lowest levels of both imports and exports in several years. That makes China the world’s third-largest crop protection market and the largest market in the Asia/Pacific Region.

Market Developments

The global crop protection market achieved an average 9.8% growth between 2010 and 2014. In the same period, the Chinese crop protection market rose 16%. In 2015, for the first time since 2010, the Chinese crop protection market did not grow in nominal terms. If China is to continue growing, it needs to manage the many challenges that its industry is faced with.

During the past 20 years, many smaller Chinese enterprises rode the wave of overall market success and got a piece of the cake for themselves. The Chinese crop protection industry seemingly could do no wrong. Environmental concerns and international regulations were not enforced to the extent they are today, and international demand was continuously high. Many smaller enterprises benefited from this boom — they could jump in and earn their share for a year or two and decide to exit before diving into the manufacturing of the next most-hyped chemical coming off patent.

In recent years, industry consolidation and stricter environmental requirements forced out a number of smaller market participants. Among the many small- and medium-sized companies, a few larger corporations have emerged, and they are worthy contenders for global market leadership. ChemChina and Sinochem are only two of these larger corporations.

The widely discussed takeover of Syngenta by state-owned ChemChina will greatly impact the global crop protection market — but what about the impacts in China?

Demand Drivers

With the recently announced two-child policy in place and with the overall need to feed its population, food self-sufficiency is one important issue the country needs to address sooner than later. This seems even more important in times of economic slowdown and the possibility of balance-sheet recession.

Considering that it needs to produce enough food for the ever growing population without relying too much on imports — China’s stance on genetically modified food has been somewhat inconclusive at times. The general echo in public is against GMOs, however, the decision that this technology could be widely adopted in China seems to be around the corner, notably for rice and corn. Should the ChemChina deal with Syngenta go through, advanced genetic engineering could become more readily available in China, which would pave the path for domestic cultivation of genetically modified food. This would allow the company to deliver integrated solutions to the farmer — seed, crop protection, and agronomic support — from a one-stop shop. This is something that has already raised repercussions against the deal both domestically and abroad.

Considering that it needs to produce enough food for the ever growing population without relying too much on imports — China’s stance on genetically modified food has been somewhat inconclusive at times. The general echo in public is against GMOs, however, the decision that this technology could be widely adopted in China seems to be around the corner, notably for rice and corn. Should the ChemChina deal with Syngenta go through, advanced genetic engineering could become more readily available in China, which would pave the path for domestic cultivation of genetically modified food. This would allow the company to deliver integrated solutions to the farmer — seed, crop protection, and agronomic support — from a one-stop shop. This is something that has already raised repercussions against the deal both domestically and abroad.

A “ChemChina-Adama-Syngenta” mega corporation could lead to a monopolistic market situation where winning market shares for foreign players as well as other domestic players would become even more difficult than in the past. ChemChina and Syngenta already indicated that having Adama in the mix would not lead to overlaps, as the intention is to have offerings in both the generic and proprietary segments. The other concern that is widespread domestically, is the involvement of the “state,” which could lead to non-market behavior and give an unfair competitive edge to the new mega corporation.

China’s overall growth has lost some momentum since 2011, but its hunger for commodities continues to grow disproportionately to the global average. China’s growth is increasingly shifting from an industry-driven growth to a more consumption-led growth. The continued growing food demand from China’s surging population, especially for meat, creates enough opportunity for the agriculture industry to continue growing and will most likely also put a hold to the commodity-price slide. At the same time, emerging Asia must contribute more strongly to overall regional growth, which then itself would generate commodity demand large enough to fill the void left by China.

As far as the crop protection market is concerned, further de-stocking can be expected for the running year 2016, which can turn into a slight market growth for 2017, provided that consumption levels remain stable.

Dr. Nomman Ahmed is the Regional Manager of Asia/Pacific for syndicated grower level market research in crop protection and seed at Kleffmann Group. He is also a senior analyst of Kleffmann’s agricultural input market trend information and consulting wing — amis AgriGlobe. His peer-reviewed publications address agricultural economics, climate change economics and agrichemicals. He is a regular contributor to AgriBusiness Global and can be reached at [email protected].