China Price Index: Fortune Comes After Difficulties

The market has already begun to adjust, but until the new market equilibrium arrives, the key for supply chain teams is timing.

Scroll Down to Read

THANK YOU TO OUR SECTION SPONSOR

Anhui Huaxing Chemical Industry Co., Ltd

BY DAVID LI

CONTRIBUTOR

According to the International Monetary Fund (IMF), China’s economy is set to rebound in 2023 as mobility and activity pick up after the lifting of pandemic restrictions, providing a boost to the global economy.

According to Reuters, the IMF previously raised its 2023 global growth outlook slightly due to “surprisingly resilient” demand in the United States and Europe, an easing of energy costs and the reopening of China’s economy after Beijing abandoned its strict COVID-19 restrictions. The IMF revised China’s growth outlook sharply higher for 2023, to 5.2% from 4.4% in the October forecast after “zero-COVID” lockdown policies in 2022 slashed China’s growth rate to 3% — a pace below the global average for the first time in more than 40 years.

However, the IMF also mentioned that China still faces significant economic challenges including contraction in real estate markets, which remains a major concern. In addition, there is still uncertainty around the evolution of the virus. Long-term headwinds to growth include a shrinking population and slowing productivity growth.

Just one day before the IMF updated predictions of China’s economic growth, China’s State Council Information Office held a press conference (Feb. 2) to introduce the work and operation of commerce in 2022 and answer questions from reporters. According to the Ministry of Commerce, the biggest challenge from 2022 was supply chain obstruction and lack of compliance ability. Heading into 2023 concerns were expressed over weak foreign demand and declining orders, an important change.

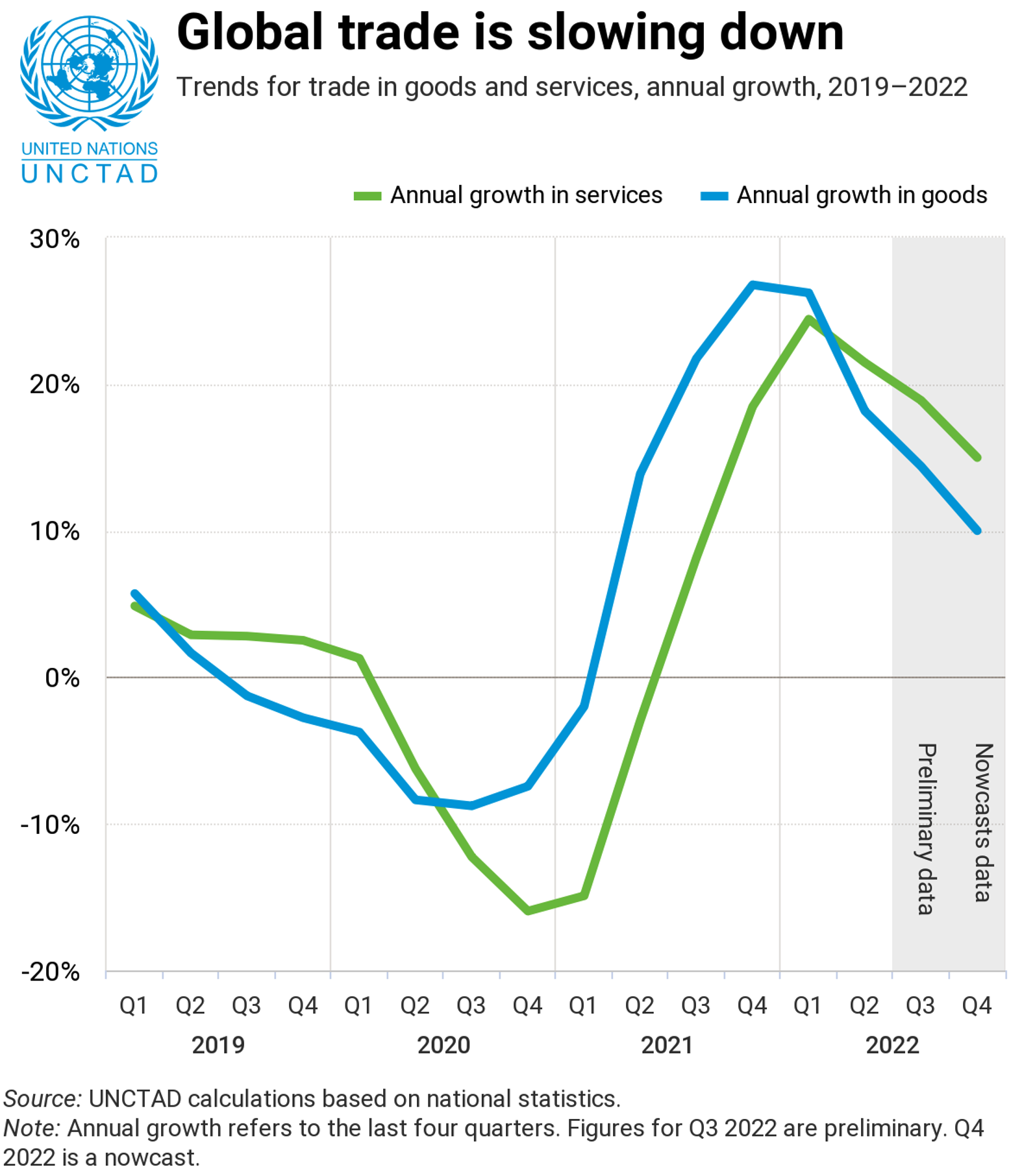

The contraction in overall global trade volumes became a major influence on Chinese exports beginning in August 2022. According to the United Nations Conference on Trade and Development’s (UNCTAD) latest Global Trade Update, released on Dec. 13, global trade reached a record $32 trillion in 2022, with strong growth in both goods and services. Trade in goods grew by 10% over 2021 to an estimated $25 trillion, partly due to higher energy prices. Trade in services grew by 15% to a record $7 trillion. However, the global trade slowdown that began in the second half of last year is expected to continue to affect the global economy through 2023 due to geopolitical tensions and continued strained financial conditions. It is safe to say that global growth will reach a downward inflection point, or rather, a recession, starting in 2023.

Chart 1: Global Trends for Trade in Goods and Services

As a country with massive manufacturing capacity, China’s economic structure is characterized by “Dual Direction of Import & Export Oriented.” That is, raw materials such as crude oil, natural gas, and other resource-based raw materials need to be imported continuously and steadily. The final products produced are mainly for the global consumer market. This “Dual Direction” economic structure of China means that its manufacturing industry is affected by even tiny fluctuations in overseas consumer markets. In the global economy, the U.S. and Europe are critical to China’s manufacturing growth. In 2022, China’s imports and exports of goods surpassed the 40 trillion CNY ($5.97 trillion USD) mark, reaching 42.1 trillion CNY ($6.28 trillion USD), an increase of 7.7%. In 2022, China’s exports to the U.S., EU, and ASEAN accounted for 16.2%, 15.6% and 15.8% of China’s overall export trade, respectively. The growth rate of export to U.S., EU, and ASEAN was 3.7%, 5.6%, and 15%.

Among China’s top three trading partners, ASEAN is an import and export-oriented economy, so China’s exports to ASEAN are also ultimately influenced by the global consumer market. Strong exports to ASEAN could also reflect the shift of supply chains from China to multi-manufacturing centers around world. China’s exports in both Q3 and Q4 2022 were significantly lower than the previous year due to weak global demand and the impact of China’s COVID-19 pandemic control on production and logistics. The hope was that demand for Chinese products from overseas markets would improve in 2022. That didn’t happen as expected.

Chart 2: China Export YOY

Fortune Comes After Difficulties.

The Chinese philosophy does not believe that good things will always be good. Conversely, we do not believe that bad things will always be bad. The sun and the moon come and go, and the night will eventually lead to dawn. This is what the traditional Chinese believe is the way the universe operates. Starting in January 2023, the China Caixin Manufacturing PMI began to rebound, a sign of recovery for Chinese supply. The confidence of global players in China’s supply is gradually being restored as Chinese society has fully returned to normal production and life order.

Chart 3: China Caixin Manufacturing PMI

In 2023, global sourcing managers will refocus their sourcing strategies on “In-Time Delivery.” High safety stocks will become a thing of the past. Scattered orders and price sensitivity will be a common issue for Chinese AI sales managers this year. The off-peak season for glyphosate sales will return to normal in 2023.

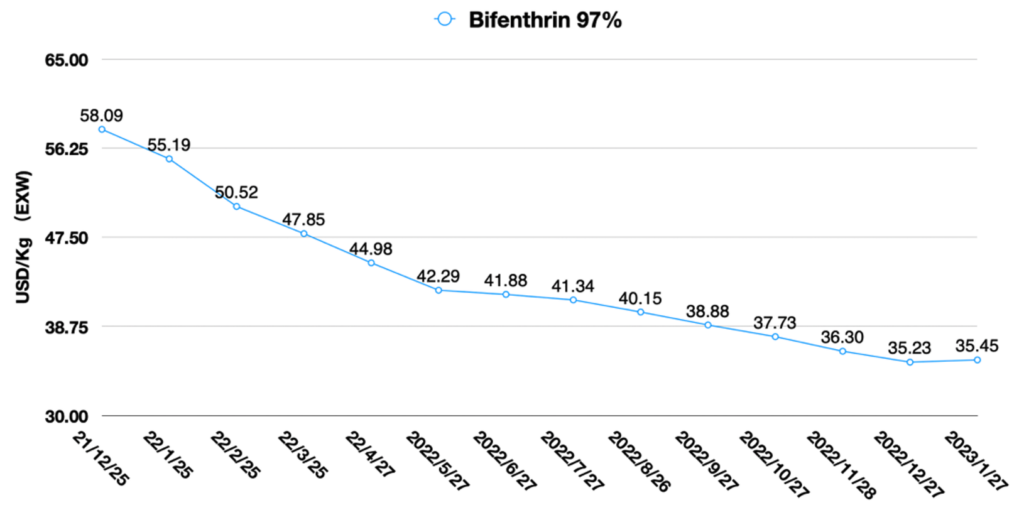

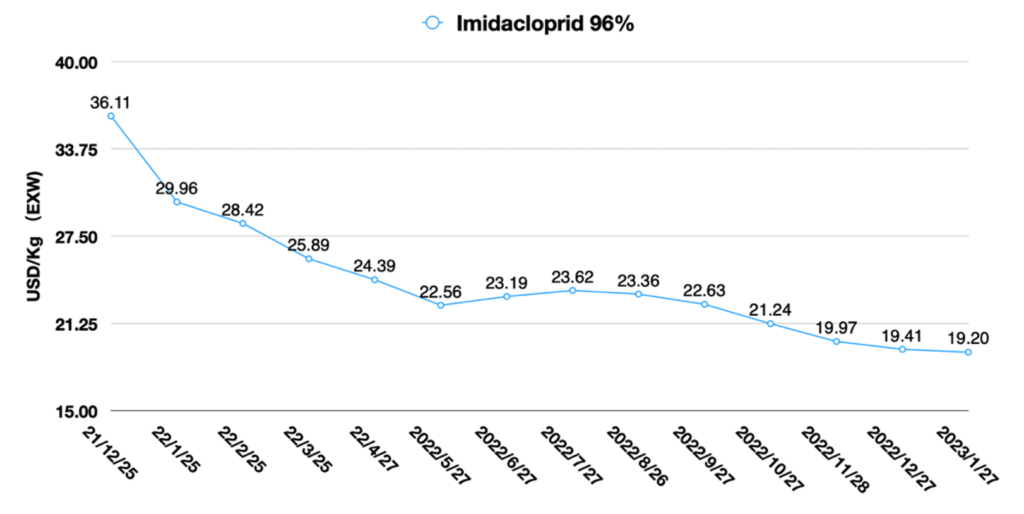

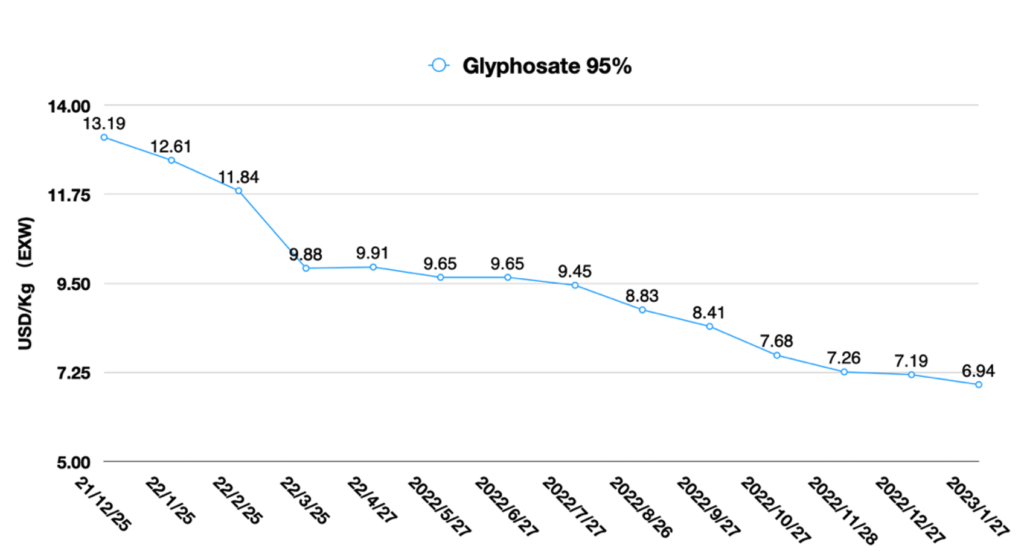

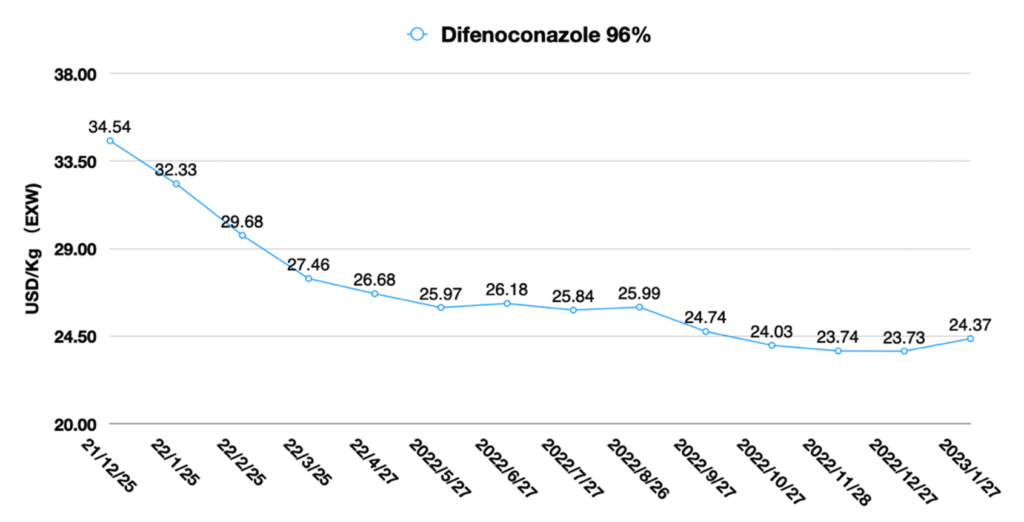

In China’s burndown herbicide market, the price of glyphosate AI remains in a steady downward trend. From October 2022 to now, the monthly price reduction of glyphosate 95% AI is around 0.45 USD/Kg. The adjustment of upstream raw material capacity according to downstream end-use demand has a lag. Only after a period of depressed demand, raw material supply could adjust its upstream capacity accordingly. The gross margin of glyphosate raw material has been reduced recently due to the heading up raw material cost.

The fall application season in the southern hemisphere is nearing its end, and there is some consumption of field application. The extent of product inventory depletion in the channel needs further investigation. Therefore, it is unlikely that overseas customers will purchase newly produced glyphosate AI on a large scale in the short term.

In March, the product roll-out in the northern hemisphere will be completed. The de-stocking strategy in the northern hemisphere has just started. Bayer Crop Science and generic companies’ strategies are likely to shift from “brand pricing” to “value pricing” to stimulate channel inventory depletion. And generic glyphosate’s gross margin will take a significant hit during the “stock consumption season.” It will be diminishing the pricing level of generic glyphosate by reverse. In-sum, sales of glyphosate produced by Chinese companies, the world’s largest supplier of generic glyphosate, will be lower than in 2022. The operation rate will continue to be negative, and this aspect will delay the magnitude of glyphosate price cuts.

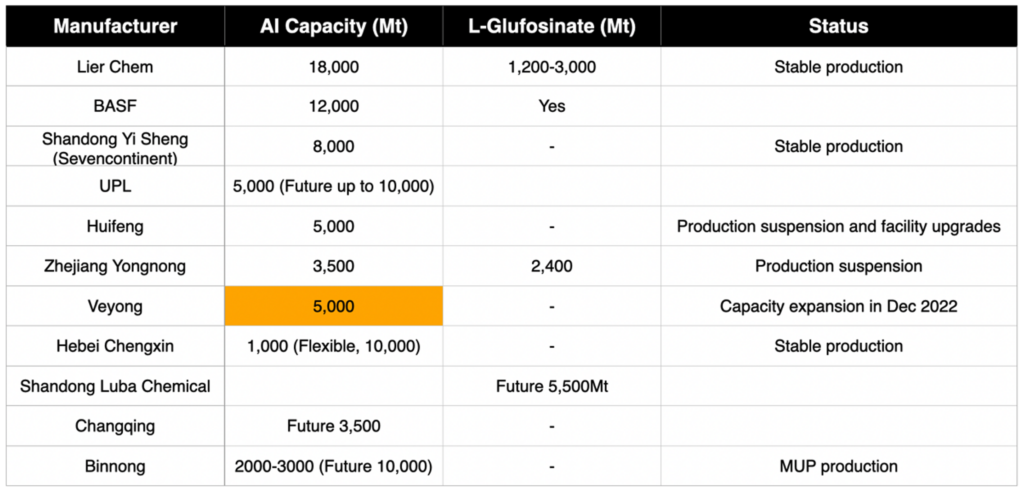

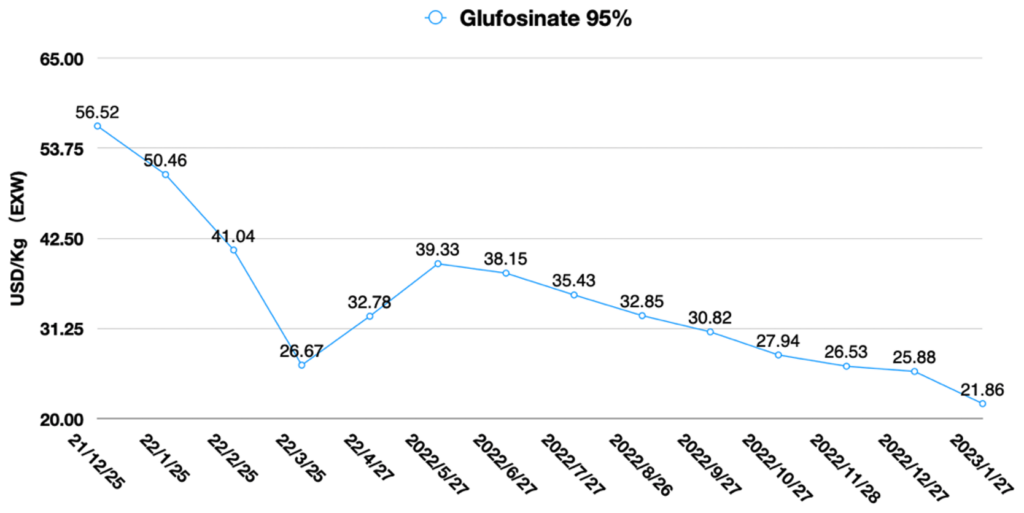

The competitive situation for glufosinate, another very important burndown herbicide, is much tougher. Due to the capacity added by Veyong in the fourth quarter of 2022 and the possible new capacity rising in the first quarter of 2023, buyers generally hope to see the performance of glufosinate prices after the new capacity is landed. Although the increase of domestic glufosinate capacity in China has affected its price firmness in the long run, the global registration of new capacity still needs some time to be granted. There is still a long way to go from global distribution strategy design to implementation on the ground. A malicious price war should be avoidable for a period of time, probably. At present, the gross margin of glufosinate is around 42%, and the producer who can control upstream raw materials has more advantages in production costs will likely be the last standing player. In the short term, supply and demand is the decisive factor for the current price of glufosinate.

Chart 4: Global Key Glufosinate Capacity

All in all, 2023 will see excesses before the “new equilibrium” arrives. Until the new market equilibrium arrives, the key competency for supply chain teams is “timing capability.” Controlling costs should not require the team to buy at the lowest point of raw material prices, but should require the team to make the lowest risky choice given an assessment of the combined market supply risks. Or the team should be able to make the choice that maximizes the company’s return given a certain level of risk. That’s what I call “timing capability.”

When developing global strategies, I always like to think in terms of long-term returns. This gives us a different perspective on the development of a region, a country, a people, and even a person. Long-term thinking will give one an unspeakable sense of certainty. It allows one to generate wisdom by sustaining a deep commitment in a field. Thus, his systematic thinking allows him to predict future trends. Immortals with the ability to predict future do not exist, while those who have the ability to choose the right timing and do not go with the flow certainly do exist. We just need to wait for a timing, a timing after difficulties.

• HERBICIDES •

• FUNGICIDES •

• INSECTICIDES •