China Price Index: Anti-Dumping Action Against Chinese Glyphosate Reshapes the Global Pricing Landscape

13 July 2026

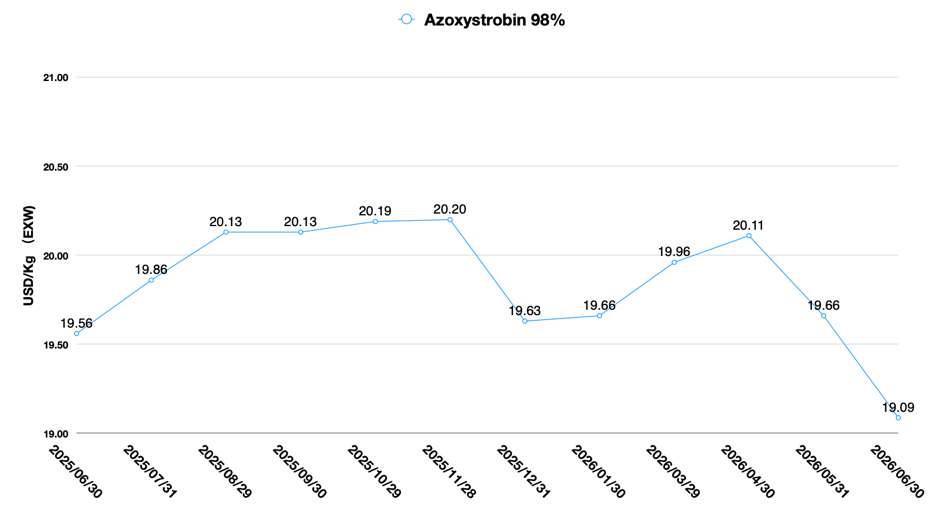

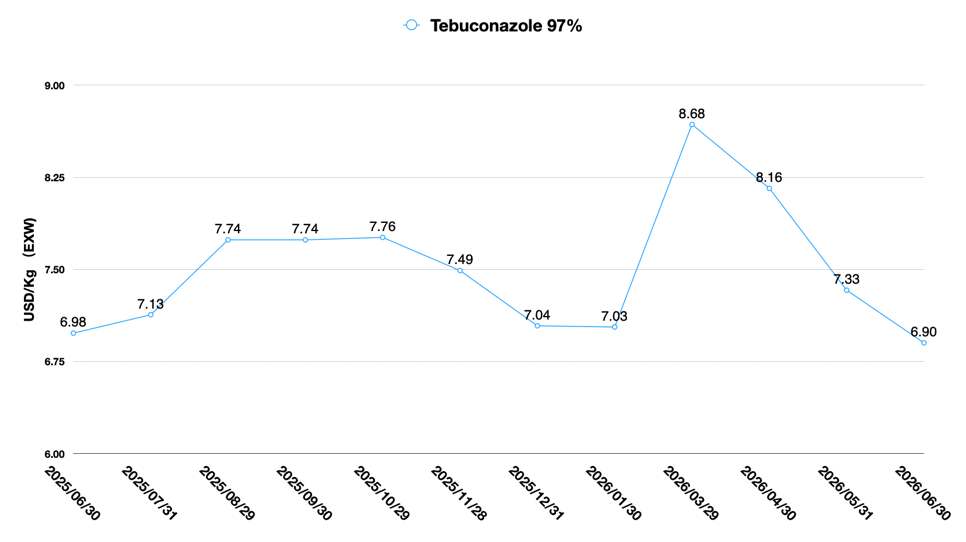

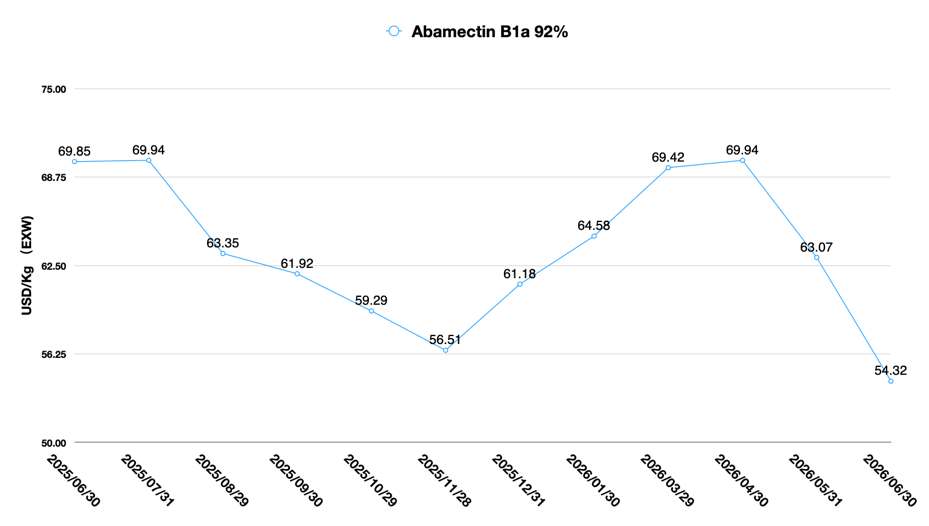

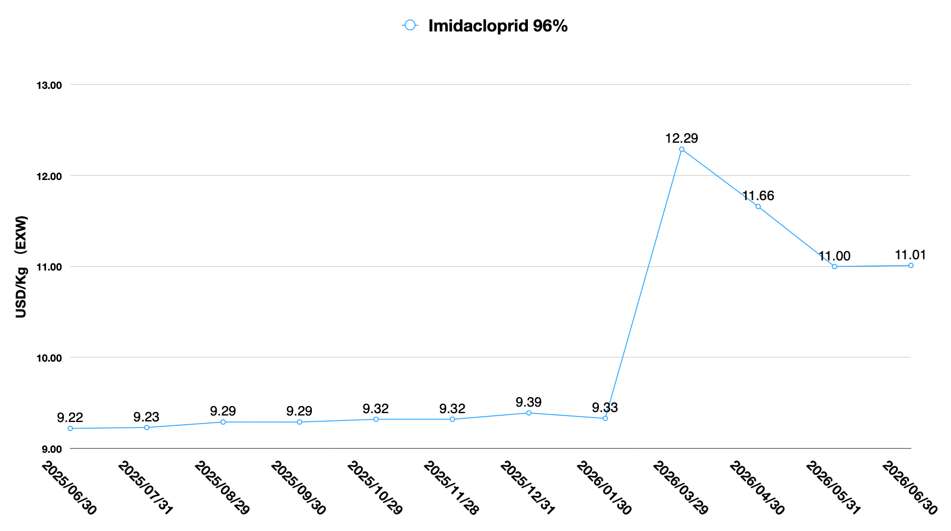

13 July 2026 Editor’s note: Contributing writer David Li offers a snapshot of current price trends for key herbicides, fungicides, and insecticides in the Chinese agrochemical market in his China Price Index. Below he also examines how Bayer’s trade petition, supply chains, and phosphorus dynamics could alter competition, costs, and procurement worldwide.

View all

According to Bayer CropScience’s announcement on July 1, 2026, Bayer Group set up Ruveon LLC to manage the business of glyphosate for the U.S. market. As Bayer mentioned, Ruveon will focus on all aspects of U.S. glyphosate, pricing, go-to-market strategies, production, and logistics and will be solely responsible for the U.S. glyphosate business.

Moreover, Bayer also asked the U.S. government to impose anti-dumping and countervailing duties on glyphosate imports from China. Bayer claimed that China’s subsidized and low-priced glyphosate are undermining U.S. domestic production.

Should anti-dumping duties on Chinese glyphosate be implemented, prices of this core nonselective herbicide in the U.S. market will inevitably rise over the long term. Bayer is under immense pressure to boost profits from its glyphosate business in the United States, stemming primarily from the massive ongoing outlays it has incurred over the past five years to resolve litigation involving its Roundup herbicide.

In February 2026, Bayer announced a settlement agreement with a maximum total value of USD 7.25 billion. Designed to resolve tens of thousands of pending and future lawsuits, the settlement stipulates installment payments spread over a period of up to 21 years. Faced with such an enormous financial burden, the only viable solution is to gradually offset these costs via future profits generated from glyphosate operations.

This is likely the core rationale behind Bayer’s launch of Ruveon, its new dedicated business unit. Independent operation of Bayer’s U.S. glyphosate division can shield the group’s overall share price from adverse impacts stemming from U.S. glyphosate litigations, achieving structural separation between Bayer Group and glyphosate-related lawsuits.

Chart 1: Bayer’s Glyphosate-Related Compensation

| Time | Event | Amount | Notes |

|---|---|---|---|

| 2020 | Large-scale settlement | Approx. $10–11 billion | Resolved most pending lawsuits at the time. |

| 2023 | Jury verdict | $1.56 billion | This award is likely to be significantly reduced on appeal. |

| 2026 | Proposed settlement | Up to $7.25 billion | To be paid in installments over 21 years; pending final court approval. |

| 2026 | Estimated annual expenditure | Approx. €5 billion | Bayer’s estimate for full-year 2026 litigation-related expenses. |

Why the U.S. Glyphosate Market Remains Strategically Important

The global glyphosate market is clearly a stock market. Growth in the planting area of genetically modified (GM) crops represents the sole source of volume expansion for Glyphosate TC, yet this upside potential remains extremely limited. Brazil and the United States are the two core markets for glyphosate.

According to data from AgbioInvestor, Brazil’s GM crop acreage rose by 5.9% in 2023 and 1.4% in 2024. Over the same period, U.S. GM crop planting area dipped by 0.4% in 2023, with a modest increase of only 1.3% recorded in 2024. While Bayer faces fierce competition from Chinese generic agrochemicals across other global regions, the high-value U.S. market stands out as the last stronghold that Bayer is determined to defend.

Against the backdrop of persistently depressed bulk agricultural commodity prices and Chinese buyers shifting their agricultural produce sourcing to South American suppliers, the U.S. agricultural economy relies heavily on government subsidies, which appear to be the sole factor sustaining consistent profitability for American farmers.

As stated in the report Agriculture Market-Mid Year Update and Outlook published by Selcius Partners: “U.S. agricultural subsidies are projected to reach USD 44.3 billion in 2026, nearly matching the record high set during the pandemic. This figure accounts for approximately 29% of total net farm income; without such subsidies, agricultural revenue would drop by roughly 12% in 2026. These support measures only serve compensatory purposes and cannot fundamentally improve industry fundamentals. The entire agricultural sector is heavily reliant on policy backing from the federal government.”

Currently, U.S. farmers’ spending on crop protection products accounts for between 4% (corn) and 6% (soybean) of their total farm expenditures. While spending on crop protection products accounts for a limited share of farmers’ total outlays, such products remain an indispensable tool for U.S. growers to mitigate yield losses caused by diseases, weeds, and pests and safeguard agricultural output.

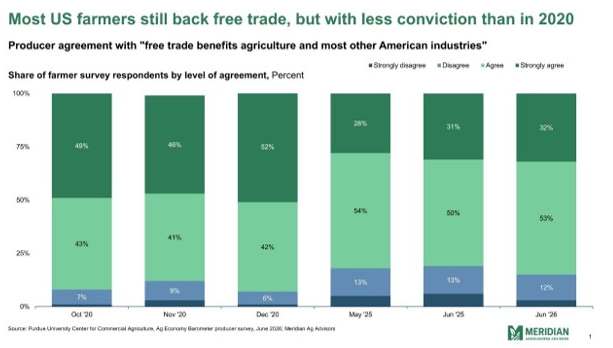

Surveys conducted jointly by Meridian Agribusiness Advisors and the Purdue University Center for Commercial Agriculture show that 53% of U.S. farmers still believe free trade benefits agriculture as well as most other U.S. industrial sectors.

Competition Has Benefited Farmers — But Not Necessarily Manufacturers

Low-priced generic agrochemical compounds from China have helped farmers worldwide cut production costs to a certain extent. Supported by ample supply that eases inflationary pressure, China’s pesticide supplies play a positive role in curbing inflation across various economies starting from agriculture, a foundational industry.

Nevertheless, from the perspective of commercial profitability, capital and enterprises may not welcome unfettered free-market competition. Monopoly is arguably the “optimal route” for capital to secure long-term steady returns when farmers cannot freely choose what product they want.

Farmers form the cornerstone of agriculture. Price competition among generic products enables growers to afford optimal crop protection solutions to a certain degree. For instance, after Syngenta’s diquat faced competition from Chinese diquat supply through FBN, the field application volume of diquat in North America surged by nearly five times. While North American farmers benefited from lower diquat prices and market demand saw remarkable growth, Syngenta’s foothold in the U.S. diquat market remained largely intact. FBN reaped substantial gains amid fierce rivalry over diquat supply between Yongnong and Lier Chemical. Following the flattening of distribution channels, both distributors and farmers have gained benefits from competition among Chinese manufacturers.

Similarly, the real competition lies among Chinese suppliers of Glyphosate TC.

How Chinese Glyphosate Reaches the U.S. Market

Chinese glyphosate manufacturers currently mainly supply Glyphosate TC to major U.S. distributors. Key leading distributors in the U.S. market include Nutrien Ag Solutions, Helena Agri-Enterprises, WinField, J.R. Simplot, and other industry giants. Backed by their dominant market position across the United States and robust distribution networks, these large distributors wield extraordinary bargaining power to drive down prices when negotiating with Chinese suppliers. As a result, Chinese suppliers fail to secure high margins on fully standardized Glyphosate TC; even reasonable profit margins are relentlessly squeezed. Amid a downturn in the global agricultural economy, Chinese manufacturers are forced to compete against one another to secure orders for Glyphosate TC from major U.S. distributors.

Due to tariff barriers between the U.S. and China, finished glyphosate formulations produced in China cannot directly access the U.S. market. Most manufacturers therefore enter the U.S. market primarily by selling Glyphosate MUP.

In terms of distribution channels, while Chinese firms have attempted to replicate FBN’s business model, sales channels for glyphosate formulations in the U.S. are dominated by purchasing groups and platform operators such as Tenkoz and WestLink, alongside independent retailers and individual brokers. This multitiered distribution system suffers from severe fragmentation. Distributing Chinese-made formulated goods through such scattered networks inevitably incurs substantial extra costs. Accordingly, Chinese formulation suppliers cannot adopt an ultra-low pricing strategy for North American distribution across these fragmented channels.

Basically, their target customer profile for U.S. farmers differs fundamentally from Bayer’s. Chinese glyphosate formulations mainly cater to cash-strapped, price-sensitive growers. Consequently, U.S. farmers who opt for Chinese glyphosate formulations exhibit low brand loyalty to Chinese suppliers, creating massive uncertainty for Chinese players’ end market sales.

Stable supply and predictable pricing are critical for growers. Leveraging brand equity and grower reward programs, Bayer’s branded glyphosate products continue to deliver high-quality formulations and services to U.S. farmers. Private-label glyphosate brands owned by U.S. distributors, Chinese brands, and Bayer’s Roundup compete side by side in the marketplace. When Glyphosate TC prices fluctuate, the coexistence of Chinese supply and Bayer’s operations creates an implicit supply buffer for American farmers within the overall supply structure.

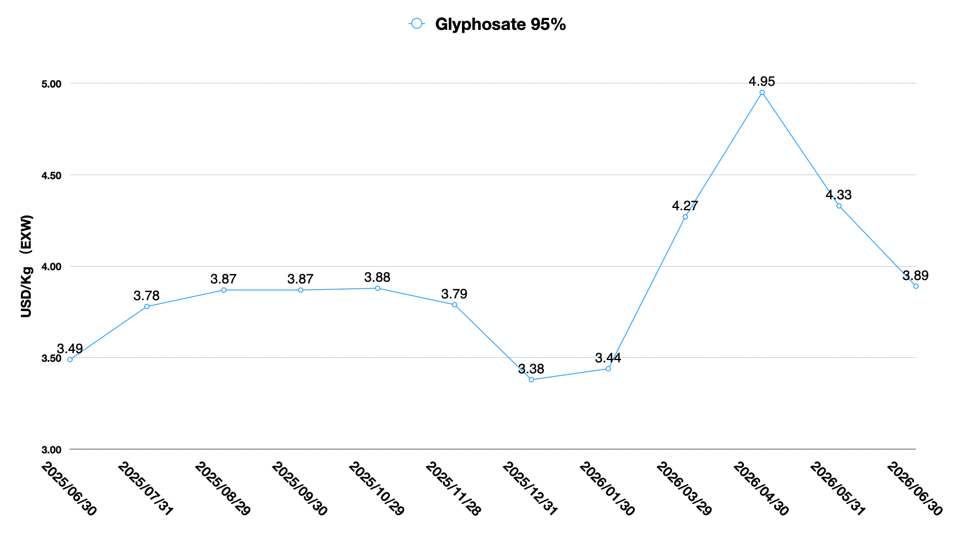

Between 2025 and 2026, China’s Glyphosate TC saw two rounds of sharp price surges. The first rally ran from July to November 2025, and the second has been ongoing since April 2026. Most notably, Glyphosate TC prices in China jumped by a steep 24% between March and April 2026. During these periods, to hedge against drastic price volatility of Chinese supplies, some downstream U.S. distributors promptly shifted their purchasing away from Chinese sources and turned to Bayer’s glyphosate formulations instead.

As Chinese manufacturers are forced to raise selling prices for Glyphosate TC amid cost pressures from yellow phosphorus, U.S. farmers can secure consistent glyphosate supply at relatively stable prices from Bayer, which guarantees predictable returns for their agricultural operations. Such steady earnings allow American growers to maintain viable businesses amid economic swings. Competition on the glyphosate supply side largely preserves farmer surplus.

The Anti-Dumping Timeline Could Reshape Purchasing Decisions

Even though free market competition has delivered sustained profitability for U.S. farmers and the agricultural sector, U.S. agricultural stakeholders will have little capacity to reverse the consequences stemming from Bayer’s anti-dumping petition targeting Chinese Glyphosate TC. The lengthy timeline required to complete anti-dumping proceedings will stand as an extremely critical factor for market participants to weigh. From the date Corteva filed its petition to the final decision by the U.S. government agencies, the entire process of anti-dumping took approximately 14 months.

The key milestones of Corteva’s case are as follows:

Chart 2: Timeline of Corteva’s 2,4-D Anti-dumping

| Date | Event |

|---|---|

| March 14, 2024 | Corteva formally filed anti-dumping and countervailing duty petitions with the U.S. Department of Commerce (DOC) and the U.S. International Trade Commission (ITC). |

| April 23, 2024 | The DOC officially initiated anti-dumping and countervailing duty investigations on 2,4-D imports from China and India. |

| April 1, 2025 | The DOC issued its final determinations of anti-dumping and countervailing duties, finding a dumping margin of 127.71% for the Chinese companies under investigation. |

| April 29, 2025 | The ITC voted to make an affirmative final injury determination (material injury). |

| May 27, 2025 | The DOC published the anti-dumping duty order in the Federal Register. |

As the timeline shows, the final decision involved multiple stages. From Corteva’s filing to the DOC’s final determination (April 1, 2025) took about 12.5 months; to the ITC’s injury determination (April 29, 2025) took about 13.5 months; and to the final issuance of the duty order (May 27, 2025) took about 14.5 months.

The 14-month window spanning July 2026 to September 2027 will constitute a critical procurement period for U.S. distributors. To cover glyphosate demand for the 2026/2027 planting season, U.S. distributors will most likely maintain regular purchasing volumes before the end of 2026.

Chinese suppliers carry ample inventories, and shipments of Glyphosate TC from Chinese manufacturers to Brazil slowed in 2026. Accordingly, domestic Glyphosate TC prices in China will undergo structural adjustments in response to shifting demand.

U.S. distributors are unlikely to build up high inventory levels prior to 2027. Stockpiling large volumes of Glyphosate TC in advance would exert substantial pressure on distributors’ cash flow. Meanwhile, holding excess inventory prematurely incurs extra warehousing expenses and interest outlays — particularly if U.S. players rely on financing to procure Chinese Glyphosate TC ahead of schedule. Therefore, U.S. distributors will adopt a restrained procurement strategy through the fourth quarter of 2026.

In 2027, as Bayer’s anti-dumping case against Chinese Glyphosate TC moves forward, U.S. distributors may advance purchases of Glyphosate TC for the 2027/2028 planting season as early as the start of 2027. Glyphosate TC prices in China typically hit a trough between January and February 2027, with inventory levels also remaining relatively low during this window. Demand for Chinese Glyphosate TC from Southeast Asia and Africa is set to kick off in March 2027, followed by purchasing activity from South American buyers starting in April. Therefore, in H1 2027, U.S. market participants must prioritize supply availability over pricing when making supply chain decisions. Concentrated global demand release will likely strain production capacity among Chinese manufacturers, leading to a high probability of backlogged orders and upward price movement for Chinese Glyphosate TC.

Phosphorus Becomes the Next Strategic Battleground

For Chinese Glyphosate TC manufacturers, there exist two major variables: first, the cost pressure on downstream glyphosate production brought by price fluctuations of domestic yellow phosphorus, and second, the strategic decisions adopted by China Glyphosate TC producers.

Pursuant to Decree No. 893 of the State Council of the People’s Republic of China, phosphate rock has been officially designated a national strategic resource in China. Chinese policymakers are guiding domestic enterprises to rationally utilize domestic phosphate rock reserves.

Driven by accelerated domestic substitution, China’s semiconductor industry has seen a sharp surge in demand for electronic-grade phosphoric acid and high-purity phosphine. These products feature formidable technical barriers and deliver profit margins far exceeding those of conventional chemicals. Furthermore, phosphate rock is a nonrenewable strategic resource, and high-grade deposits worldwide are gradually being depleted.

Fueled by explosive growth in China’s new energy sector, competition for phosphorus resources between food production (fertilizers) and energy manufacturing (battery materials) has intensified dramatically. Going forward, China’s phosphate rock resources are likely to be allocated more toward high-value segments rather than bulk agricultural inputs such as Glyphosate TC.

At the Central Economic Work Conference held in December 2025, China explicitly put forward the requirement to “strengthen the security guarantee of strategic resources.” In February 2026, the United States signed the Defense Production Act to designate elemental phosphorus as a critical national defense material. This signals that geopolitics has become the primary factor shaping the development of the yellow phosphorus industry. Macroeconomic policies also serve as the key driver behind price fluctuations of yellow phosphorus in China. In 2027, domestic yellow phosphorus prices in China are likely to emerge as the core variable determining the cost pricing of Glyphosate TC.

On the other hand lies the strategic transformation of Chinese manufacturers. Faced with uncertainties surrounding potential punitive tariffs on Glyphosate TC, it is difficult to predict how Chinese enterprises will respond. Nevertheless, from the perspective of sustainable business development, China’s Glyphosate TC industry may advance strategic transformation plans in advance. The risks arising from overreliance on Glyphosate TC operations to underpin financial performance may compel these firms to identify new revenue growth drivers.

For Bayer CropScience, Chinese Glyphosate TC and private-label glyphosate formulations distributed by U.S. distributors will continue to pose headwinds to the earnings recovery of Bayer and Ruveon from Q3 2026 through Q2 2028. Tensions between Bayer and U.S. growers may undergo a fundamental shift as a result of the glyphosate anti-dumping case. This transformation raises several critical questions: Will U.S. farmers still strongly prefer Bayer’s offerings for other crop solutions and integrated seed-plus-crop-protection packages? How will U.S. distributors navigate negative perceptions of Bayer held by local growers and agricultural associations amid the fallout from Bayer’s policy moves? How will Bayer contend with competition from Chinese manufacturers across global markets? Within China, how can Bayer build mutual trust in its partnerships with domestic Chinese collaborators?

There is an ancient Chinese idiom: draining the pond to catch all the fish (overexploiting resources for short-term gains at the cost of long-term sustainability). Every multinational crop protection firm across the globe takes “driving income growth for farmers and safeguarding food supply” as its core vision. This mission is easy to uphold during periods of robust economic expansion. However, when enterprises fall into operational difficulties, maintaining commitment to this vision becomes a severe test.

Companies are forced to choose between short-term profits and long-term visions, and this dilemma bears no fundamental logical link to the impact of Chinese supplies, given that Chinese suppliers inherently serve multinationals and large distributors in U.S. market. Meanwhile, the core challenges facing Bayer CropScience go far beyond simple competition over Glyphosate TC: Fluropyram, bixafen, prothioconazole, etc. will be still under fierce competition. Perhaps time will deliver a fair resolution.