China Price Index: Downward Price Trends for Glyphosate, Glufosinate a Tipping Point for Key Herbicides

14 March 2022

14 March 2022 Editor’s note: Contributing writer David Li offers a snapshot of current price trends for key herbicides, fungicides, and insecticides in the Chinese agrochemical market in his monthly China Price Index. He also provides insight into why prices of glufosinate and glyphosate are trending downward, as well as what the crisis in Eastern Europe might mean for an already fragile supply chain.

View all

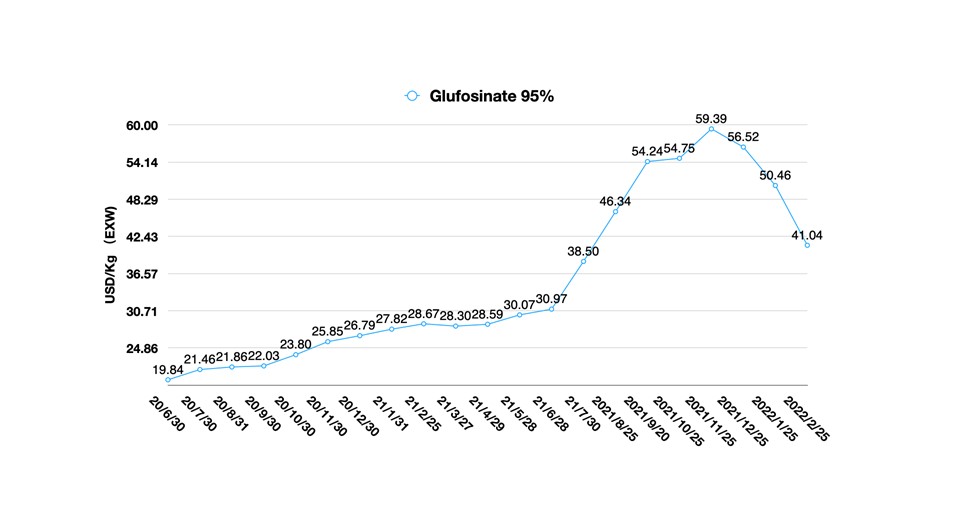

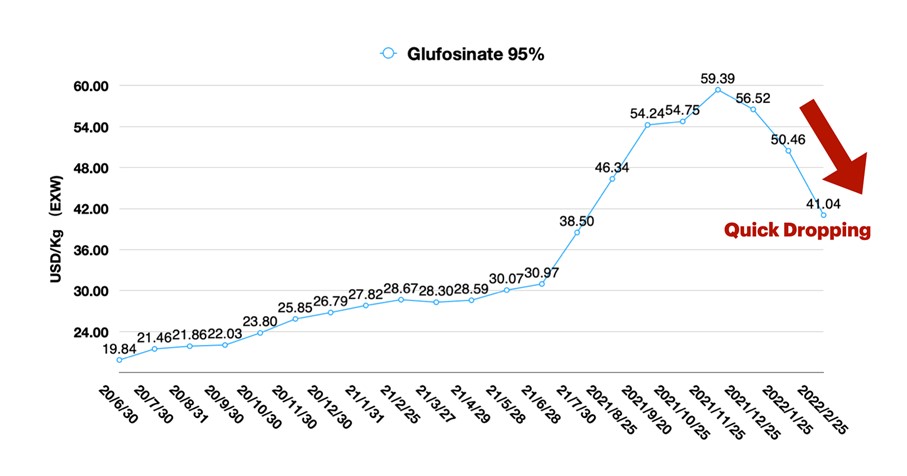

Chinese manufacturers often introduce their new capacity below market value. For example, the price for glufosinate AI dipped to EXW 37 USD/Kg, which is lower than the recent market price of EXW 41 USD/Kg when Lier Chemical and Yongnong Chem made new product available to buyers. And by the end of 2022, Veyong is expected to release additional glufosinate into China’s ag market. The increased inventory is accelerating the drop in cost for glufosinate AI, which was already experiencing a downward pricing trend.

Even with the price drops, there is still room for the herbicide’s key producers to decrease prices even further due to weak global demand. Even so, it’s recommended global sourcing teams make procurement decisions continuously because lower prices for glufosinate could dilute the previous high-cost AIs on retailers’ balance sheets. Meanwhile, it can also decrease the risk of a Black Swan event.

The was some additional positive news in the form a partnership between Bayer and M.S. Technologies. Bayer made the announcement in a release on 22 February, which stated “a distribution agreement with M.S. Technologies, LLC for soybeans containing the Enlist E3 trait. The objective of the agreement is to provide Bayer’s customers with more choices and additional tools for integrated weed management. And Bayer will distribute soybean seed with Enlist E3 technology beginning in the 2023 crop season in brands that will be launched later this year. Bayer and M.S. Technologies are working together to help growers manage the growing challenge of herbicide-resistant weeds.”

It is a remarkable milestone for the third-party alliance team inside Bayer CropScience. The future white brand can make up the gap in the company’s portfolio and feed demand with the right timing. To employ multiple sites of action against the most troublesome weeds is the top priority for maintenance of farmers’ yield. With the strong demand from rural fields, Bayer’s license-in strategy will enhance the multinational’s portfolio position on the market landscape. It will drive Bayer to move to a “higher demand” level.

M.S. Technologies is the key for the collaboration of the trait license. According to the introduction on its website, Bayer first introduced LibertyLink soybeans, providing farmers with an option for superior over-the-top non-selective weed control in soybeans with no yield lag in 2009 (BASF purchased LibertyLink in 2017). M.S. Technologies and Dow Agrosciences (now Corteva) introduced Enlist E3 soybeans to the marketplace in 2019. Soybeans with the Enlist E3 trait will provide tolerance of glufosinate, new 2,4-D choline, and glyphosate herbicides. In 2018, Bayer successfully completed the acquisition of Monsanto. The new portfolio of Xtend became the face-to-face competition for Corteva’s Enlist System. The competition brought rising demand for burndown herbicides. Like Bayer’s Head of R&D on CropScience Division, Robert Reiter, said in Bayer CropScience 2022 Innovation Pipeline Update: “Simplification is powerful.”

Bayer and Corteva are both making the rural field practice simpler. And their scientists are trying their best to control resistance and delay troublesome weeds. Along with Bayer’s five herbicide tolerance soybean launch, the farmers will not be struggling to choose XtendFlex or Enlist E3. If farmers are familiar with 2,4-D technology, they can make better informed decisions while learning about dicamba. In the near future, genetically modified crops will have synergistic efficacy by bringing Bayer’s HPPD and PPO herbicides into the system. Bayer CropScience will likely reach €30 billion in sales in the coming decades.

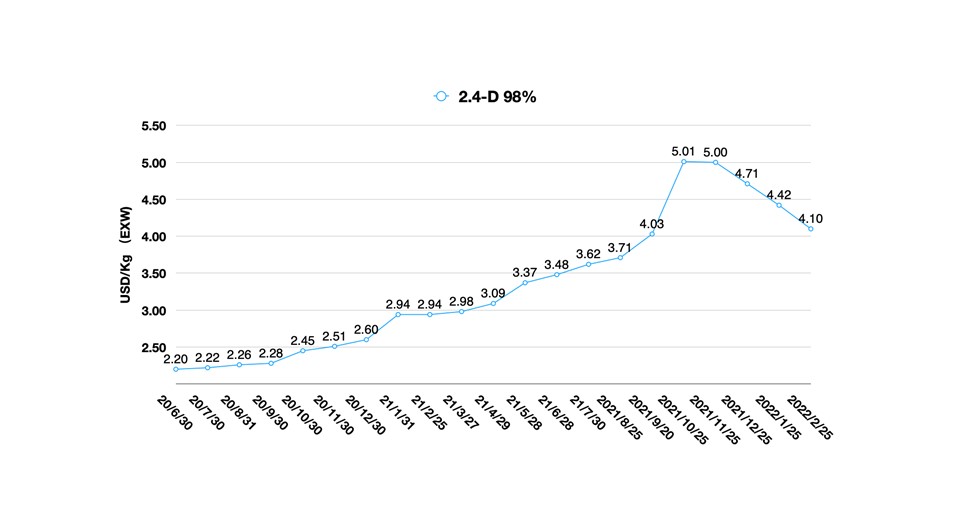

One good thing for Chinese suppliers could be extension of portfolio value for long-tail generic AIs, like glyphosate, 2,4-D, dicamba, and glufosinate. Because of regulatory restrictions on traditional products and the expense (it can cost more than USD 250 million), it will be difficult to bring new molecules to the market. The efficacy of long-tail portfolios will become more important to keep multiple modes of action part of integrated crop protection solutions.

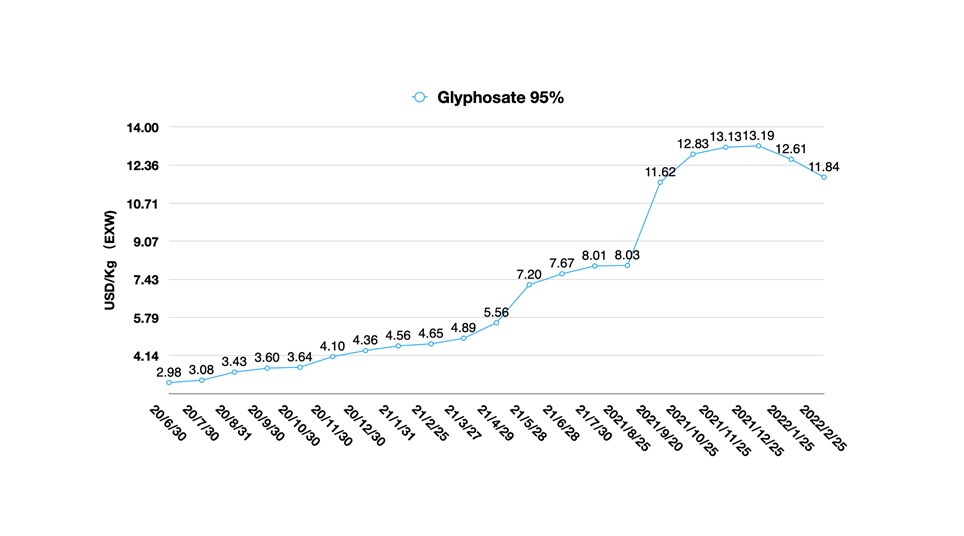

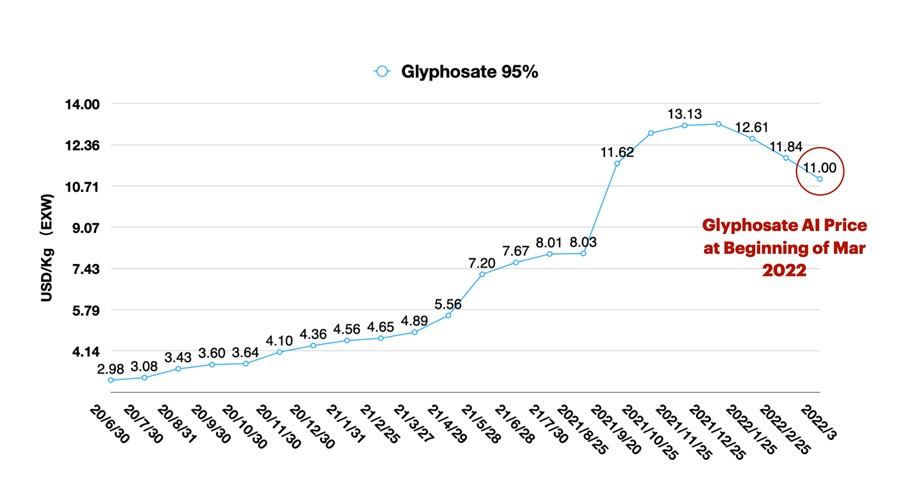

Back to glyphosate supply, the cost of glyphosate is on the way back to more traditional margins. The force majeure letter from Bayer CropScience, brought a short-term concern inside China’s supply market. Weak demand and anticipation pushed down glyphosate AI prices to a lower margin level with unexpected speed. During the first week of March 2022, glyphosate AI prices hovered around EXW 11USD/Kg. The price drop trend seems softer than glufosinate because the export business is expected to support higher-level pricing for some time. The recent Beijing Winter Olympic games did not affect glyphosate product much according to comments from some retailers’ supply chain directors. Following the adjustment of China’s “Double Control” policy, the 2022 production of agrochemical will be on the right track without national policy impact.

However, the current Eastern Europe crisis has set the world on edge and introduces uncertainties as concerning as any since the end of World War II in 1945. Add in COVID-19, the global energy shortage, and the high cost of raw materials and we have several factors that could impact the chemical industry. Guaranteeing raw material supply to European manufacturing plants will be very challenging for EU procurement teams. Because Russia delivers about 40% of the EU’s natural gas supply that region’s energy consumption could be transferred to a quota system if the conflict continues through the 2022 winter season, according to Wallstreetcn. In other words, the EU could experience interruption of active ingredients supply. In addition, transportation could also be disturbed — for example, shipments and flights with crop protection product cargo from Europe to the Asia Pacific market.

On the other hand, the supply of generic AIs made in Asia is expected to be stable due to the sufficient and integrated industry value chain. China has its own full value chain for the chemical industry whether it’s oil, fine chemicals, or other products. And its upstream manufacturers are mainly state-owned or big stock listed companies. Key agrochemical manufacturers have operated their own upstream production for many years. If there is a need, there are many ways to ensure the country has an adequate supply of crude oil and gas from China’s national inventory to keep the production stable. Due to the “Double Control” policy in September 2021, Chinese manufacturers are aware of our “fragile supply chain system.” China’s chemical value chain can handle such complicated situations after having experienced several varied and severe impacts.

As for the availability of energy, China re-evaluated the coal supply for industrial production. The government prepared well to support smooth production through 2022. And China’s government had already strengthened the supply of energy and agreed to increase the sales price of industrial electricity up to 20% maximum. The new electricity price mechanism will be the optimistic factor for China’s production this year. It can support fine chemical manufacturers to control the cost at an acceptable range.

Since the increasing of safe inventory was completed in 2021 for the main multinational companies and retailers, 2022 will bring a return to more traditional consumption levels from farmers. A new balance of demand and price had been established. The high cost of ag inputs pushed farmers to have alternative portfolios and highly efficient solutions. Resistant weeds encourage the multinational companies to upgrade their programs with multiple active ingredients, not only focusing on glyphosate or glufosinate. The panic buying on “inferior solution – glyphosate” will be less likely to happen on the farmers’ side in coming few months with China’s low-price glyphosate and glufosinate launch into global markets. 2022 could be a tipping point of strong growth for a sustainable, integrated farming experience without the fear of shortages.

Global inflation is still a big issue even though the chaos interrupted rising interest rates. According to historical crude oil prices, every big rise in the price has been a harbinger of a potential crisis to come. As I mentioned in my previous articles, inflation is due to quantitative easing (QE) monetary policy or shortage of commodity supply. Currently, the world is facing three drivers to increase the risk of crisis: The QE monetary policy around world, the supply chain disruption globally, and the shortage of supply caused by conflict. A catalyst in chemistry is any substance that increases the rate of a reaction without itself being consumed. The artificial drivers are the catalysts to change the world quickly.

As an ordinary agriculture business practitioner, I do not have the answers on the chaos sprouting from political or economic points of view. But such unexpected situation lights up the words from a famous ancient Chinese philosopher, the Laozi. Nature always makes up for the loss. The crescent moon will gradually change into full moon. Humans need to know nature’s rules, learn from them, and learn the most important thing is to get things done based on those natural rules. In 2022, the global population that will succeed will be those who find a different way to make sustainable growth with a long-term natural concept.