China Price Index: Shipping Woes Complicate Supply Chains, Prices Mostly Stable

15 June 2021

15 June 2021 The shortage of empty containers has driven the shipment costs up sharply in May. According to China Customs, there still aren’t sufficient shipments in China ports. The China Entry and Exit Shipments were 1.7% lower YOY 2020. Before the COVID-19 pandemic, the shipments were around 39.67 thousands on April 2019. Currently, congestion of empty containers in U.S., Australia, and EU ports is the key reason of the difficult shipment arrangement in China.

View all

While overseas shipping costs have been elevated for some time, the shipment cost in May increased abruptly, which brought unexpected risk to global supply chain management. The China Containerized Freight Index (SCFI) increased around 136.8% YOY 2020. The shipping dynamic, including labor availability, has been exacerbated by the state of the pandemic in India, which has impacted the supply chain globally. Shipping companies have prioritized the health and safety of their crews, making labor resources tight in key ports around the world, and especially in India.

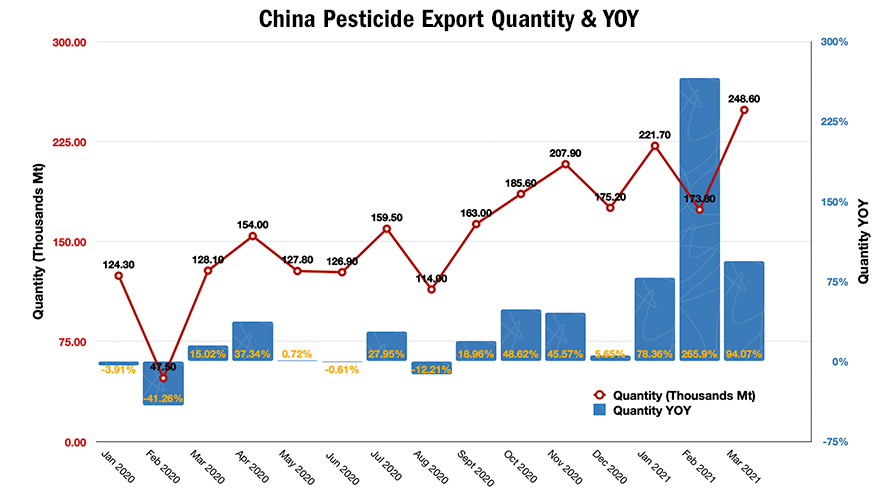

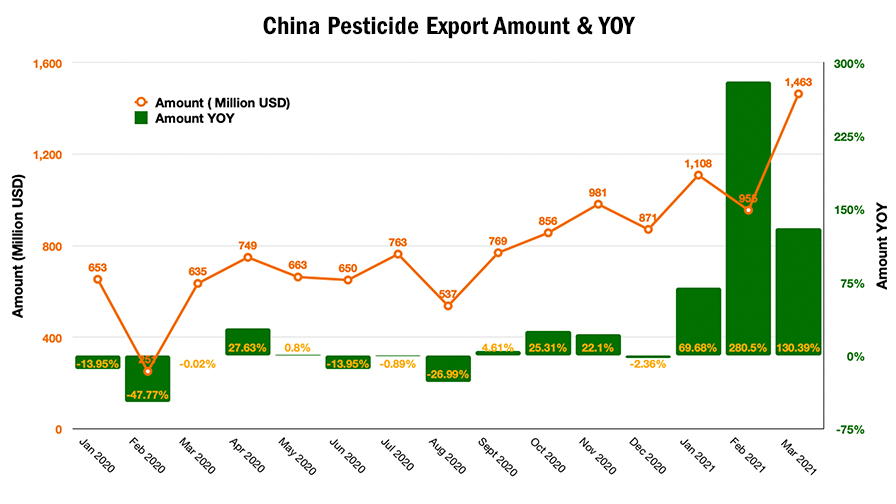

On the other hand, the global demand is booming as vaccination rates increase. In the first quarter of 2021, the U.S. import from China increased 62.7%, and the China export to U.S. went up 57.9%. For agrochemical active ingredients, quantity of China exports increased 94% YOY 2020. The amount rose to $1.463 billion, 130.39% YOY 2020. China is a critically necessary commodity provider to the world.

However, global quantitative easing has raised the risk of inflation. The strong CNY currently is a defending strategy. Key commodity prices and food prices are rising around the world. Quantitative easing in post-pandemic recovery can stimulate the economic growth by making money more available, but a side effect is that pricing of key commodities will rise. Higher prices for everything – raw materials, finished goods, labor, shipping, steel, concrete, and agriculture commodities – will offset the efficacy of quantitative easing.

The U.S. Federal Reserve is being watched closely this week as it considers higher interest rates. If liquidity is limited, then commodity prices could drop quickly. But rate increases aren’t guaranteed and could be premature, as many economists attribute the current high prices of commodities to “structural shortage” in post-COVID-19 recovery, and not a result of demand growth over pre-pandemic levels for goods and services.

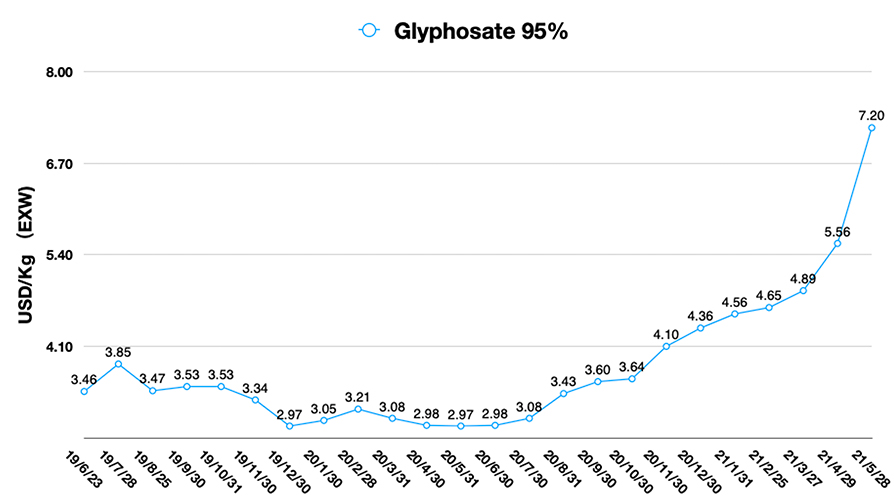

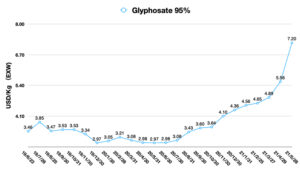

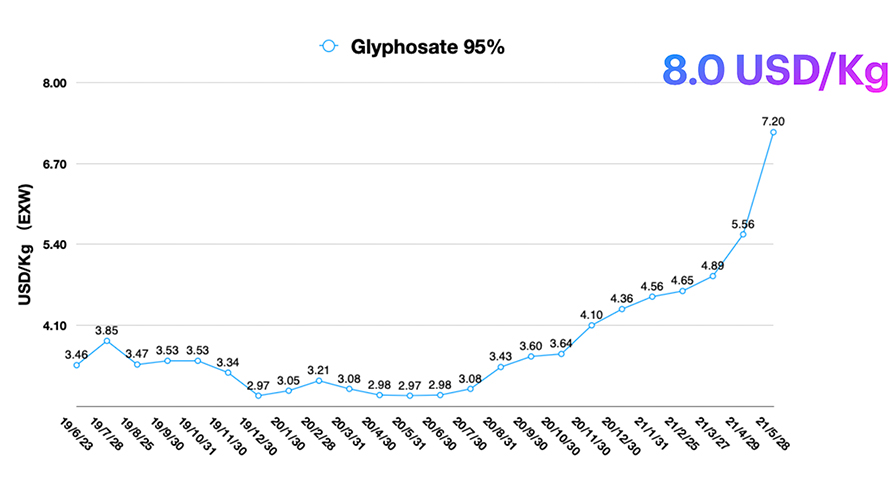

The price trends for Chinese-produced glyphosate illustrates the broader macroeconomic dynamic contributing to higher prices. In the case of glyphosate, key shortages have been a result of Fuhua Flood in 2020, shortage PMIDA supply in the beginning of 2021, high prices of glyphosate’s raw materials, and production limitation of Xingfa till April 2021. When the exporting orders poured into China manufacturers, it lengthened the ETD (Estimated Time of Departure) as a result of the confluence of factors. This created urgency for many companies, including the multinationals, which are trying to manage these new lead times so they can manage their supply chains. Very little of the price increase can be attributed to demand dynamics, but those dynamics could be shifting as a result of longer lead times and uncertain availability of overseas shipping.

Normally, the LATAM demand starts from July, and China domestic demand begins in October. Influenced by global early procurement, it can be sure that glyphosate price would be keeping in high level till the beginning of 2022. The price of glyphosate EXW could reach $8/Kg soon.

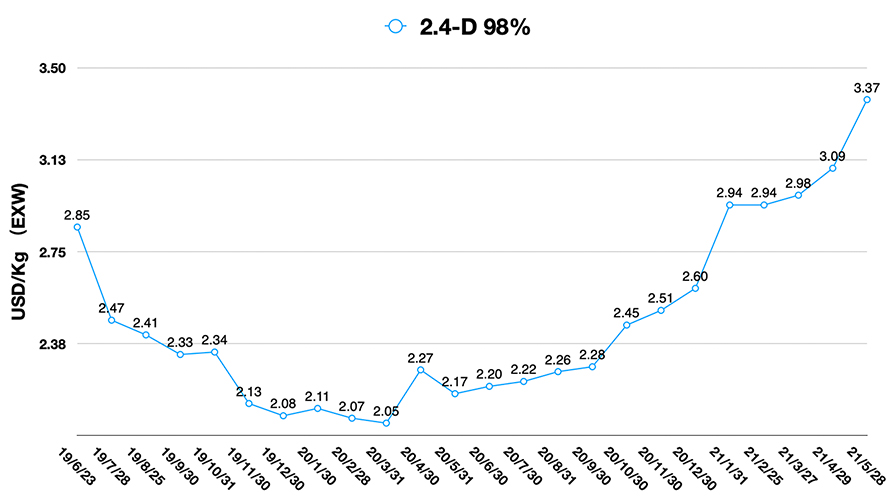

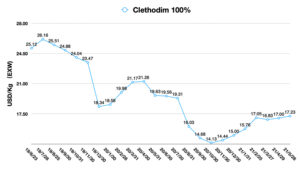

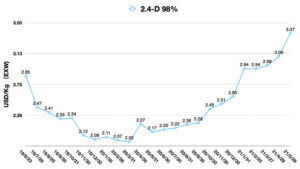

The preparation for 2021/2022 season will be starting earlier than usual due to the uncontrolled shipment cost, shortage of shipment, and high pricing. Prices for alternative herbicides for glyphosate are elevated, but prices for selective herbicides are weak.

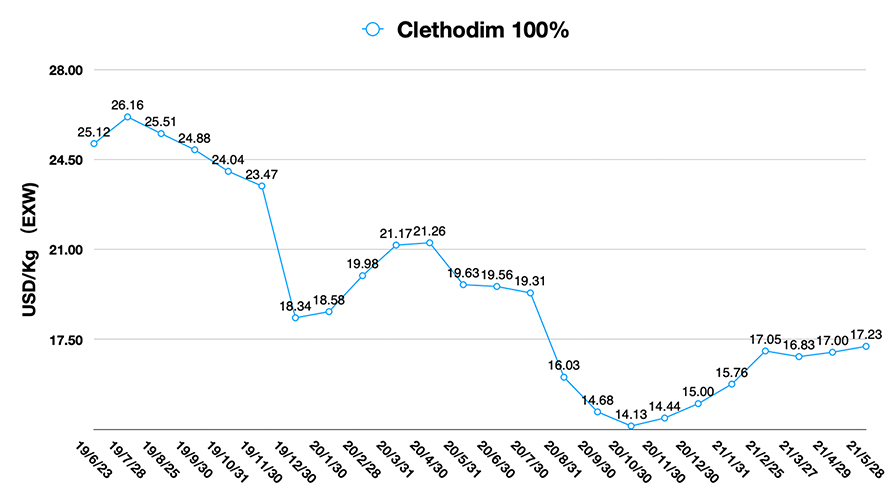

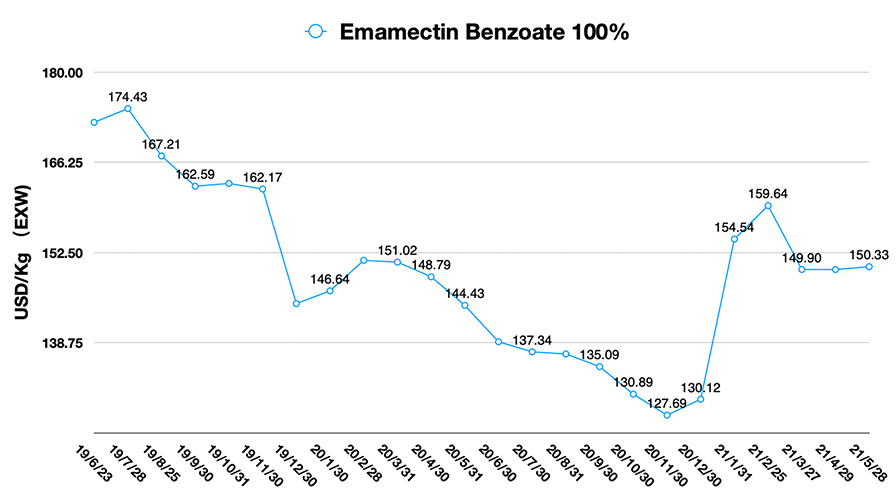

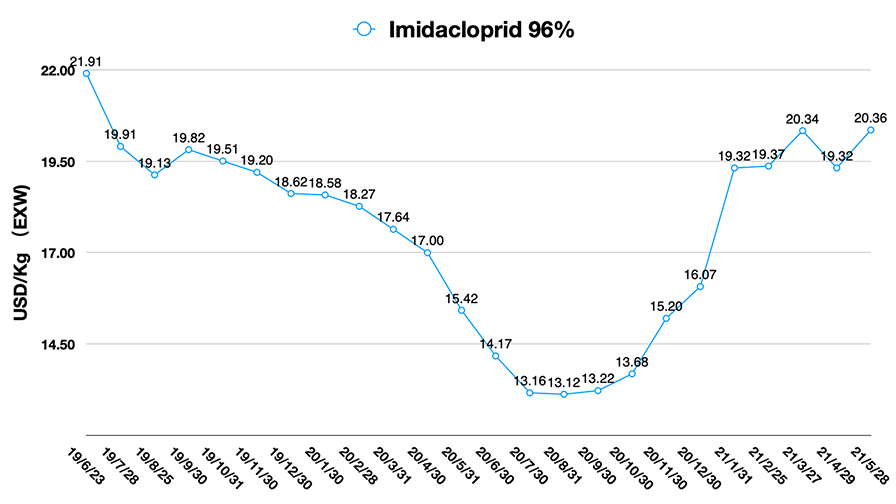

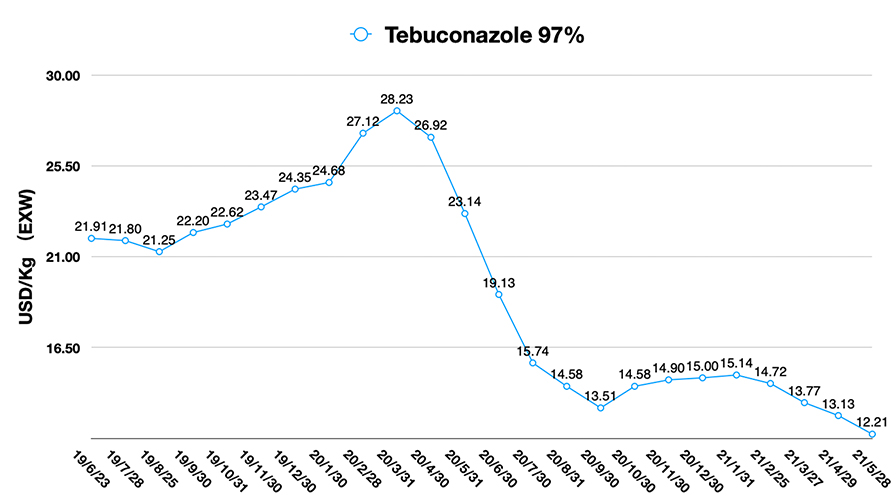

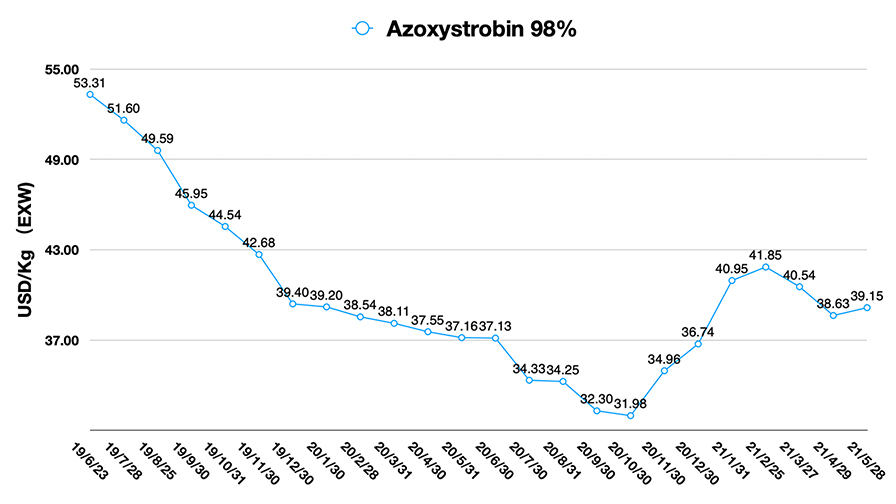

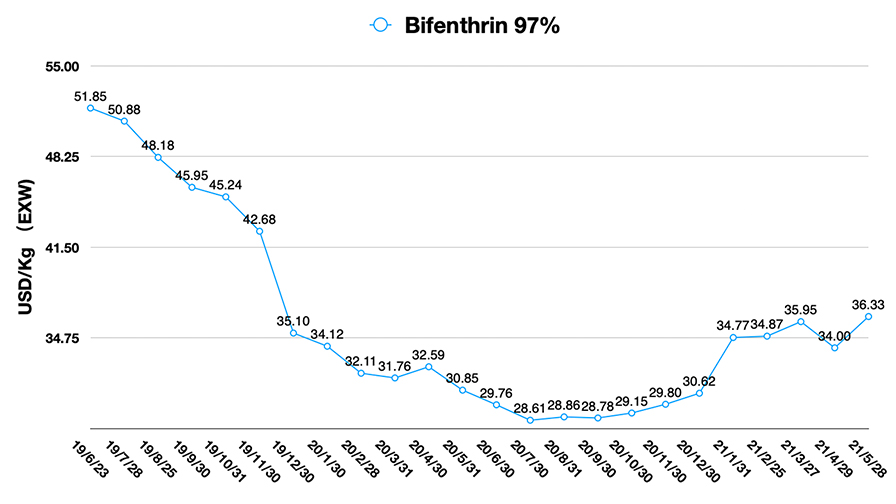

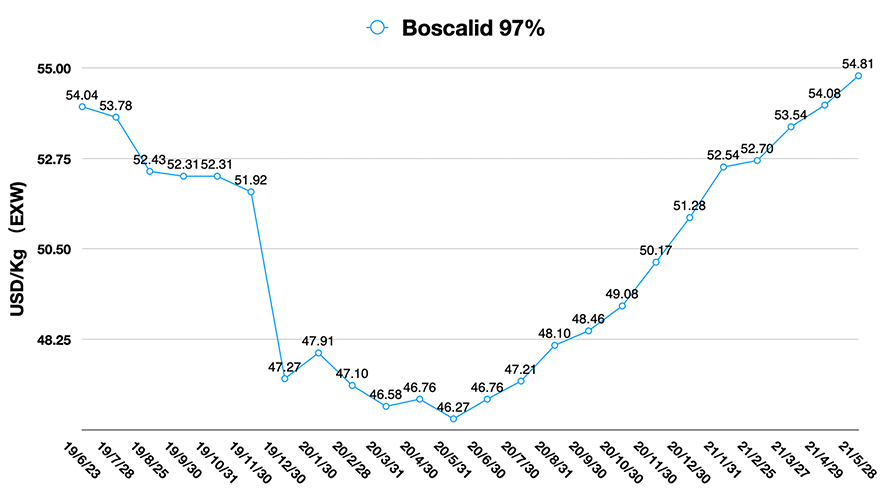

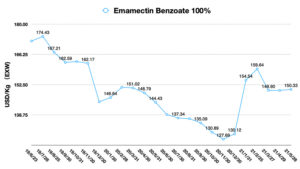

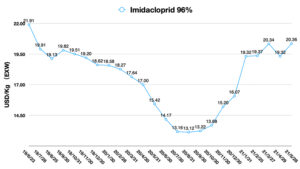

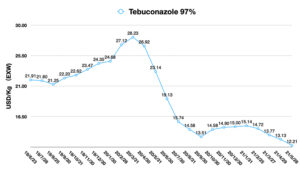

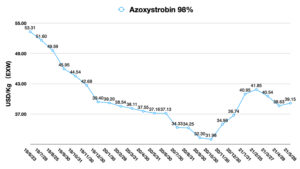

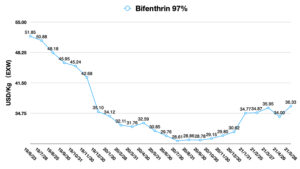

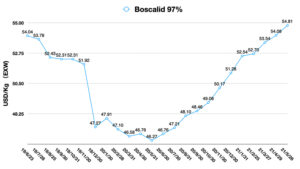

For fungicides, triazoles are facing deflated pricing. SDHI fungicide prices are dropping slightly due to weak demand from overseas. The main fungicides price trend is becoming stable. The emamectin benzoate price increased as a result of strong exporting demand and higher production costs. Low inventories and higher production costs also has inflated the price of neonicotinoid insecticides. Pyrethroid pesticides prices are driven up by higher costs of raw materials. But those are the exceptions as about 65% of insecticides are facing weak price levels through May 2021.

Pricing and unstable supply is creating higher risk for global buyers. The Eastern Hemisphere sourcing strategy must have deep collaboration with Western marketing and sales strategy. For example, high pricing of glyphosate needs new strategy of marketing. The sales pipeline and consumption by farmers could be renewed by the whole commercial operation team for crop protection companies.

Money doesn’t think. It is just a commodity that’s used to transact for goods and services to satisfy wants and needs. Only the balance of demand and supply can control the price. Quantitative easing is the enzyme to accelerate a new balance in societies around the world.