China Price Index: How Industrial Upgrading Is Key to Sustainability in the 14th Five-Year Plan of the China Agrochemical Industry

28 February 2022

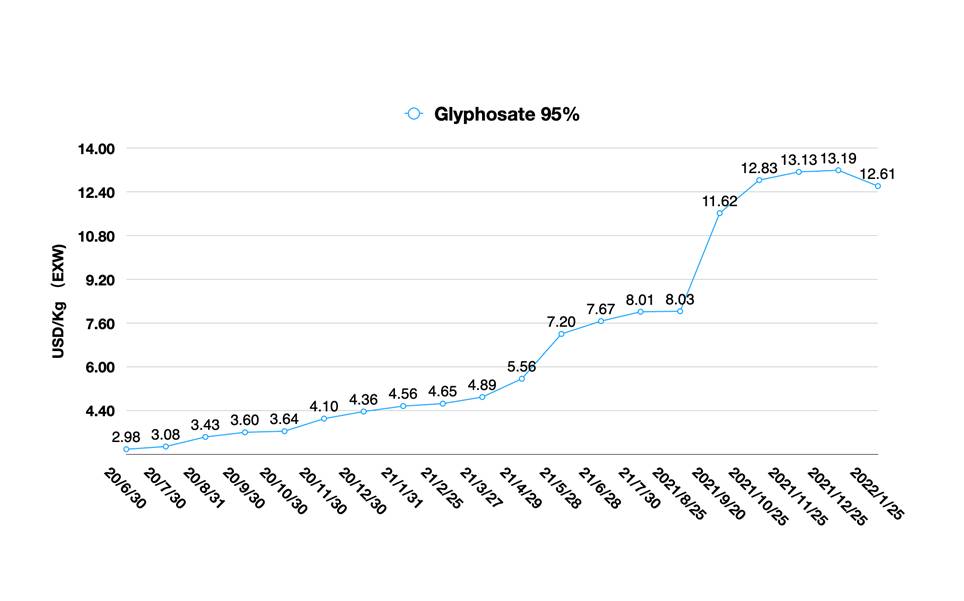

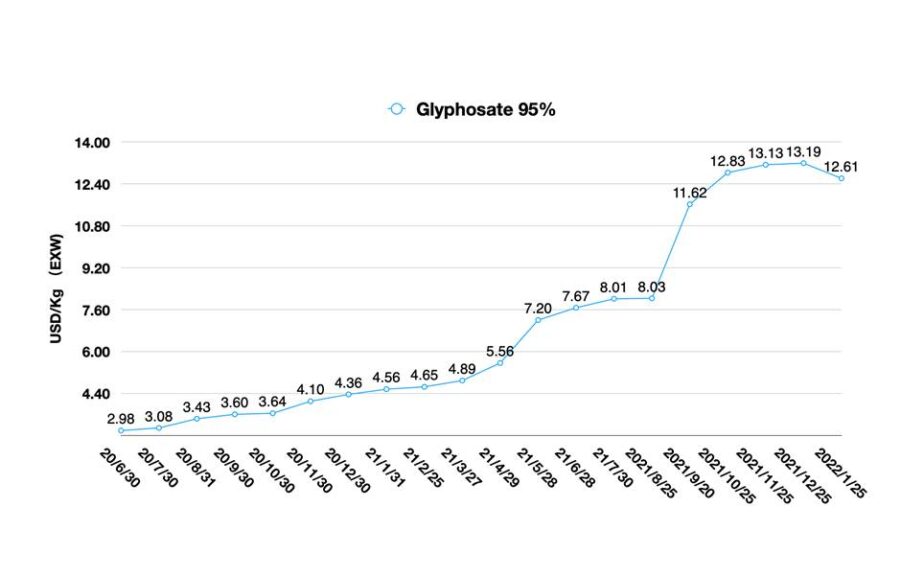

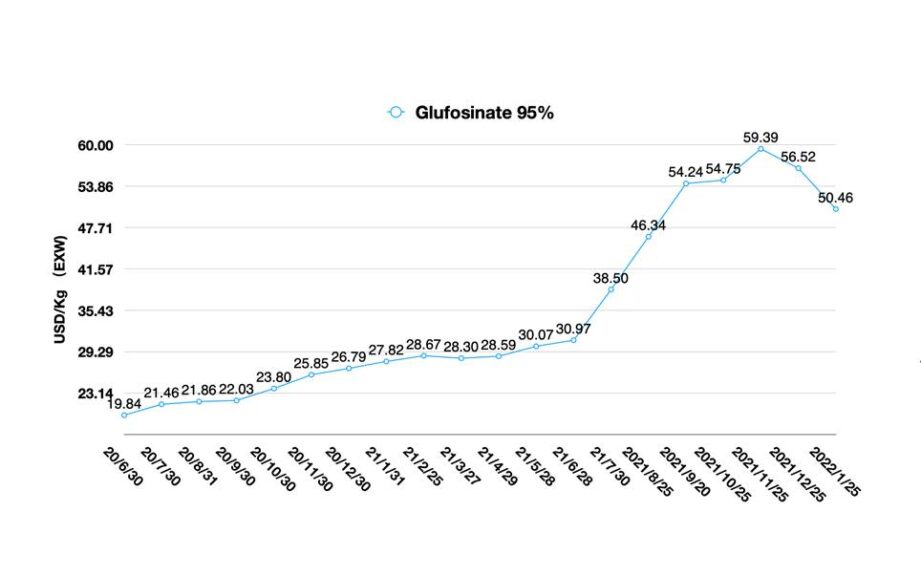

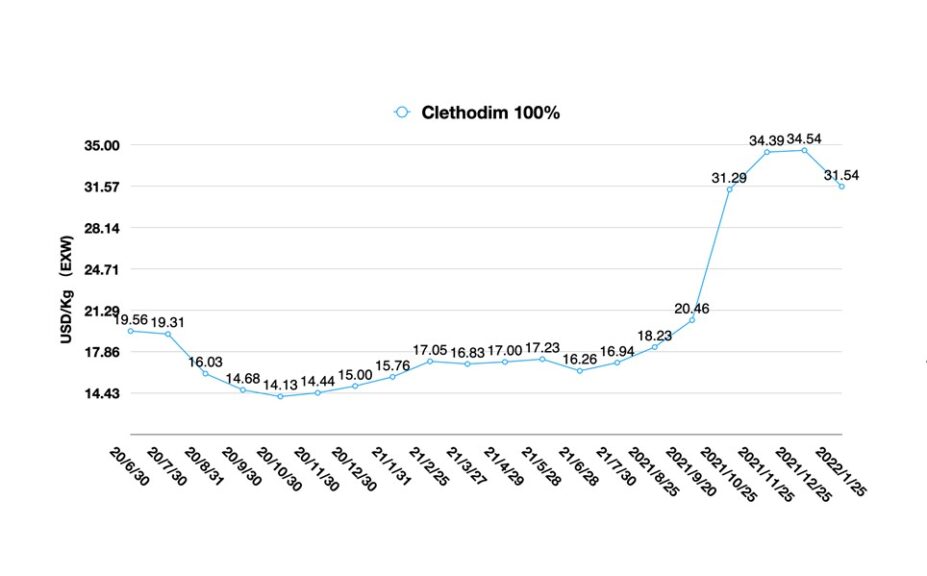

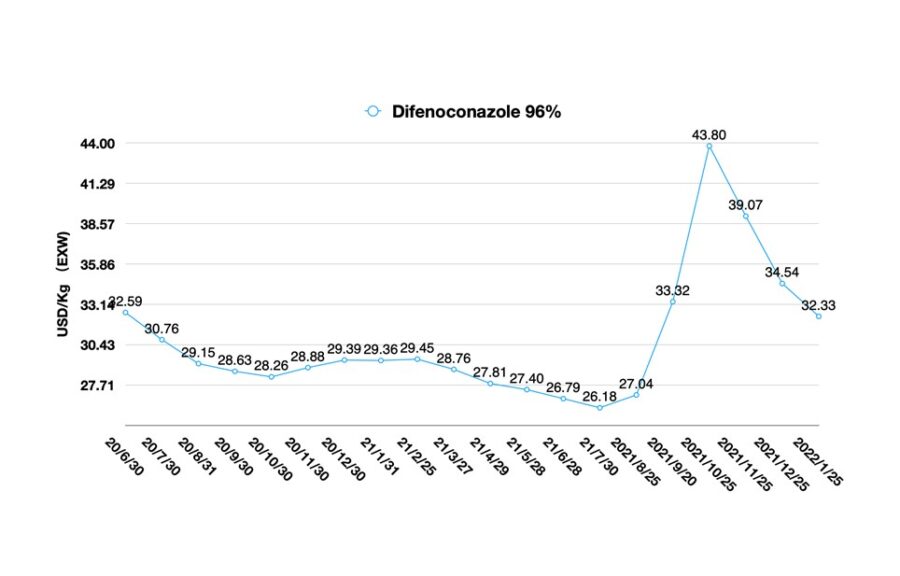

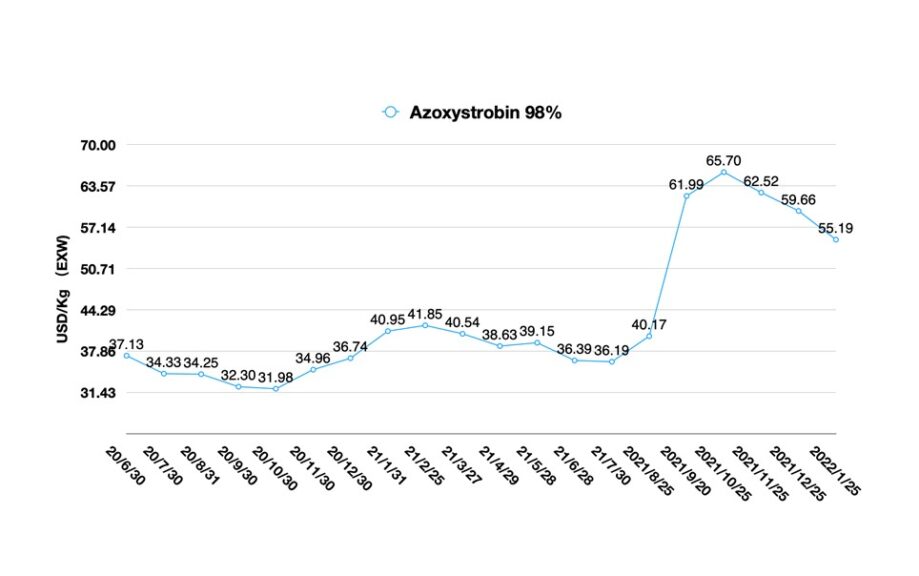

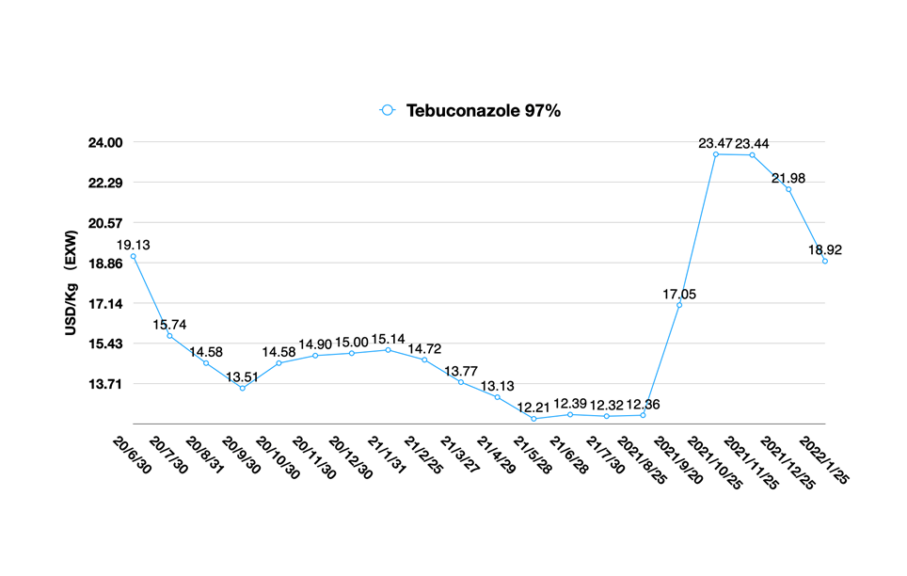

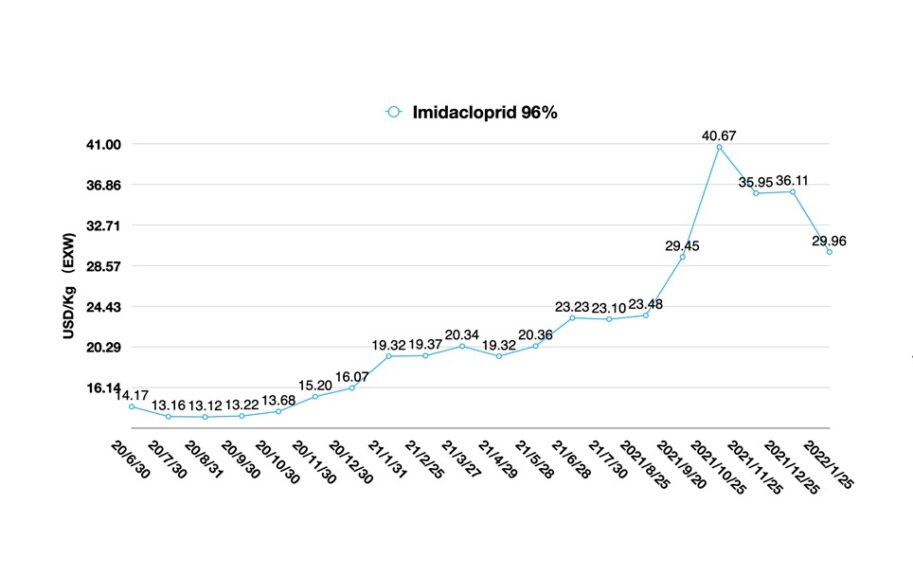

28 February 2022 Editor’s note: Contributing writer David Li offers a snapshot of current price trends for key herbicides, fungicides, and insecticides in the Chinese agrochemical market in his monthly China Price Index. He also provides insight into what the newly issued 14th Five-year National Development Plan will mean for the Chinese agrochemicals industry.

View all

In traditional Chinese culture, people believe that 60 years is a cycle, just like a year has four seasons, with spring, summer, autumn, and winter going round and round. The year 2022 is the beginning of a new 60 years, and the start of spring in the Year of the Tiger is also the beginning of the beginning. Coincidentally, the opening ceremony of the Beijing Winter Olympic Games was chosen on February 4, 2022, the same day of new beginning.

Photo credit: Xinhua

Accompanied by the Winter Olympics, China’s pesticide industry is also quietly beginning to change. On January 29, eight ministries jointly issued the 14th Five-year National Development Plan for the pesticide industry. The plan will influence China’s pesticide industry policies, laws and regulations, and industry development in the next five years.

In the 14th Five-year Plan of China Pesticide (2021-2025), three policy directions related to overseas distributors are emphasized. One is to promote industrial upgrading through green development. The other is to promote merger and reorganization driven by innovation. The third is to promote domestic and international double cycles mainly led by the demand of Chinese domestic market.

Industrial upgrading started from the 13th five-year plan of pesticides. Since the start of the “environmental protection storm” in 2017, Chinese policymakers have been determined to abandon the development model of “pollution first, clean up later”. In the face of the rapid destruction of the ecology, the local citizens and farmers do not want to trade economic growth for their environment. So China has guided enterprises through policy to carry out the first-stage upgrade of waste treatment systems, like solid waste treatment, waste water treatment, and VOC (volatile organic compounds) controlling.

The main measures are the combination of strict environmental supervision and centralized management of the industrial parks. Therefore, during the pesticide 14th Five-year Plan, the new production capacity of chemical pesticides and biological products in China will all enter the industrial park. The Jing-Jin-Ji (Beijing-Tianjin-Hebei) region, the Yangtze River Delta, the Pearl River Delta, and the Northwest new energy zone will be four production clusters combining fine chemicals, new materials, and advanced chemicals industry.

Different areas of production cluster will have different positioning. The Eastern coastal region will mainly focus on the development of innovative pesticide products. As for the new energy region in the Northwest, China will mainly focus on the biopesticide industry, the production of long-tail pesticide products with advanced processes and novel pesticide formulations.

Behind the region positioning, an important advantage is the human resources in different territories of China. The Southeast coast, for example, has a large number of institutions and universities. And there is also mature industrial workers with higher learning and strong innovation, and a relatively high degree of industrial concentration. So it is suitable for the development of innovative pesticides and patent pesticides. The Central and Western regions require industrial worker training, so scaling production is suitable for these territories. In the core competitiveness of Chinese pesticide enterprises, the region where they are located will be one of the important factors to be considered.

The Yangtze River Protection Law of the People’s Republic of China came into enforcement on March 1, 2021. On October 8, 2021, Premier Li Keqiang presided over an executive meeting of The State Council and adopted the Yellow River Protection Law (draft). In 2022, the Yellow River Protection Law is likely to be finally passed and implemented. The protection of the water source and the ecology of the upper reaches of the Yellow River will be the key goal of the implementation of the law. This will also put pressure on new capacities of pesticide in the upper reaches of the Yellow River, where compliance with emissions and production safety will be a top priority. Environmental issues have not been weakened in the 14th Five-year Plan pesticide policy, and supervision will still be enhanced.

The environmental protection regulation comes along with the “Double Control Policy” of energy consumption. China’s double control policy will avoid impact on normal production activities. And China’s various industries will try their best to upgrade their industries as the time node of “30/60 carbon peak and carbon neutral” is approaching. By 2025, China will reduce energy consumption per unit of GDP by 13.5% compared with 2020. Under such a clear goal, we will see the chemical industrial park energy consumption optimization, logistics energy consumption optimization, and other new measures for green economy growth.

For agrochemical enterprises, R&D and innovation are always the decisive factors to maintain enterprises’ long-term competitive advantage. Under the background of industrial upgrading, Chinese agrochemical enterprises are also actively responding to the new challenges. According to R&D General Manager Lei Wang, Nutrichem has principles to select the future molecules which shall have good eco-friendly property, low energy consumption, and high environmental compatibility. The confirmation of synthesis process will be the most important part in the R&D of molecules. From the original chemical process, Nutrichem prefers to select and develop the clean and green route. The continuous and intelligent research of future projects is developed at the same time. It can fundamentally solve the issues on environmental protection, low waste emissions, and energy saving.

Moreover, further combination by the research of environmental protection pre-treatment and recovery can support Nutrichem to achieve the recycling of key resources. For the production facilities, Nutrichem considers production efficiency and energy utilization as priority. The research and selection of engineering devices will be mainly for achieving the highest production efficiency under the premise of ensuring production safety and energy saving. The production process is managed in fine detail. The reasonable management of energy flow like water and steam can be utilized as recycling also.

A little innovation can lead us into a macro reality. From a pesticide enterprise’s choice of strategy and the specific implementation plans that match the strategy, we can see some practical actions of these Chinese agrochemical enterprises on the road to realizing China’s 14th Five-year Plan and achieving the goal of carbon neutrality in the future. The thinking behind the strategy will also give global partners some enlightenment on how to adapt and cooperate with each other, which contains great value.

Another important direction during the 14th Five-year Plan period of the Chinese pesticide industry is to continue to deepen industrial merger and reorganization, carry out structural adjustment, and encourage innovation drive. During the 13th Five-Year Plan period (2016-2020), environmental inspection forced the industry to eliminate outdated production capacity. Direct pollution of water and rivers is by no means what modern industrial civilization pursues. If the pollution produced by factories cannot be dealt with, then such factories and their production capacity are undoubtedly backward.

Only the agrochemical enterprises with high technology and high gross profit margin can lead the industry to a higher level of development. This is the key reason why China’s pesticide industry has been constantly merging and reorganizing in the past decade. Like the merger between Limin and Hebei Veyong, the acquisition of Yanhua Yoloo by UPL, the establishment of Syngenta Group, the continuous mergers and reorganizations in the agrochemical industry in the past few years have reshaped the entire value chain of China’s agrochemical industry.

Not only the mergers and acquisitions among Chinese agrochemical enterprises, but also foreign enterprises continue to invest in China’s manufacturing bases. During the re-shoring of the manufacturing sector back to the region, China’s production base, combined with the whole industrial chain, still brings continuous competitiveness to global multinational companies. The agrochemical industry is very special and unique. Its value chain is from chemical raw materials to dining table. We call it the “whole industry chain competition”. In the competition of upstream raw materials, China and the Asia-Pacific region have also become the raw material resource exporting countries that companies strive for. The location of manufacturing seems less important than the continued supply and business opportunities it brings.

By 2025, China’s pesticide industry will focus on fostering 10 enterprises with revenue of more than 5 billion yuan (around 794 million USD) and 10 enterprises with revenue of more than 1 billion yuan (around 159 million USD). It can be seen that the future supply of pesticides in China is just as we expected, 20% of Chinese pesticide enterprises will supply 80% of the world’s pesticide demand. Industry concentration will be further enhanced during the 14th Five-year Plan period of China Pesticide.

In the process of merger and reorganization, one of the most important basic principles is the compatibility of strategies. There are two main purposes of M&A: one is to expand the range of product categories, the other is to improve the production scale of product categories. The former is to increase gross margin growth potential, while the latter is to reduce costs so that key products continue to contribute higher ROI.

Although the merger between Fuhua and Jiangshan in 2021 was not successfully realized, the merger between the two parties in the future will still be highly possible. On October 8, 2021, Wynca completed the transfer registration of part of the shares of Nutrichem. The company holds 12.31% of the shares of Nutrichem and has successfully become its second largest shareholder. The capacity consolidation of long-tail products will continue in the 14th five-year pesticide period, and generics based on innovative processes and creative patent compounds will be the main growth drivers for the Chinese market. The combination of traditional long-tail producers like Wynca with innovation-driven companies, like Nutrichem, may open up new business models for sustainable growth of agrochemical companies.

The development of new compounds will be a bright spot in China’s pesticide industry in the next five years. In the past, the patent products mainly came from Japanese R&D companies. In terms of marketing, the timing and popularity of patented products are the key factors to extend the life cycle of products. Through the business model of license-out, agrochemical companies which focus on patented active ingredients could promote its products with overseas distributors and multinational companies. Due to the continuous accumulation of Chinese enterprises in the field of basic scientific research and the continuous investment in the field of life science, there will be more patented pesticide products from the China market during the 14th Five-year Plan period.

At the end of 2020, CAC Nantong signed a formal contract with Syngenta Group China to launch the “Strategic cooperation of Cyproflanilide in China”.

At the end of 2020, CAC Nantong signed a formal contract with Syngenta Group China to launch the “Strategic cooperation of Cyproflanilide in China“. Chinese companies are gradually developing patented compounds that are exploring the possibility of cooperation with multinational companies. Regional distribution agreement and overseas license-out will also be a good start for Chinese agrochemical enterprises to carry out the beachhead of global sales.

However, the huge cultural gap between China and other countries remains a challenge for these Chinese agrochemical companies. From laws and regulations to business models, from CDMO to portfolio package licensing, the capability of global commercialization could be a tough test for China’s young pesticide leaders. Therefore, in the next five years, China’s pesticide middle-class managers should not self seal in the domestic market, as the globalization of human resources could bring disruptive value to the industry. The best candidates could be those who understand Chinese culture, are familiar with international business principles, majored in chemistry, and have strong knowledge from chemicals to life science.

Different from its past over-dependence on foreign trade, China will gradually shift to an economic growth model driven by domestic demand and mutually promoted by the duo cycles of domestic demand and overseas demand. China’s pesticide demand will mainly come from the development of the domestic agricultural industry. In the next two to three years, China is expected to carry out GM crop adoption on its 1.8 billion mu (120 million Ha) of limited arable land, with corn being the preferred variety. China is under pressure to ensure food security for its 1.4 billion people. Demand for food, proteins and oils, is strongly supporting the growth of agricultural trade between China and around the world.

With such a large population base, China plays an important role in promoting the transformation of its agricultural and food systems. According to the latest food and Agriculture Organization of the United Nations (FAO) report “The State Of The World’s Land And Water Resources For Food And Agriculture: Systems at breaking point”, Dr. Qu Dongyu, Director-General of FAO, pointed out:

With such a large population base, China plays an important role in promoting the transformation of its agricultural and food systems. According to the latest food and Agriculture Organization of the United Nations (FAO) report “The State Of The World’s Land And Water Resources For Food And Agriculture: Systems at breaking point”, Dr. Qu Dongyu, Director-General of FAO, pointed out:

“Against this background, it is clear our future food security will depend on safeguarding our land, soil and water resources. The growing demand for agrifood products requires us to look for innovative ways to achieve the Sustainable Development Goals, under a changing climate and loss of biodiversity. We must not underestimate the scale and complexity of this challenge. The report argues that this will depend on how well we manage the risks to the quality of our land and water ecosystems, how we blend innovative technical and institutional solutions to meet local circumstances, and, above all, how we can focus on better systems of land and water governance.”

By 2050, FAO estimates agriculture will need to produce almost 50% more food, livestock fodder, and biofuel than in 2012 to satisfy global demand and keep on track to achieve “zero hunger” by 2030. But the problem is balancing the pursuit of agricultural productivity with limited arable land and climate change.

As noted in the report, “A central challenge for agriculture is to reduce land degradation and emissions and to prevent further pollution and loss of environmental services while sustaining production levels. Responses need to include climate-smart land management attuned to variations in soil and water processes. Management options are available to increase productivity and production levels if innovation in management and technology can be taken to scale to transition to sustainable agrifood systems. However, none of these can go far without planning and managing land, soil and water resources through effective land and water governance. Increasing land and water productivity is crucial for achieving food security, sustainable production and SDG targets.”

The FAO’s report is highly valuable. Combined with the carbon-neutral and sustainable development goals, the protection of water and arable land, it is urgent that governments make changes. It’s not just China’s pesticide industry that needs to be sustainable. Everyone involved in the crop protection industry needs to look a little bit beyond the pesticide prices to see the challenges which world agriculture will be facing now. We might better understand the far-reaching implications of industrial policymaking. At the end of this article, I would like to conclude with a quote from Dr. Dongyu in the forward of the FAO report:

“While the scale of the challenge is daunting, whether as cultivators of land or consumers of food, even small shifts in behaviors will see the much-needed transformation at the core of our global agrifood systems.”